FIN415 Class Web

Page, Spring '20

Jacksonville

University

Instructor:

Maggie Foley

Term Project Part I (due with

final)

Term project part II (excel

questions) (due with final)

Weekly SCHEDULE, LINKS, FILES and Questions

|

Week |

Coverage, HW, Supplements -

Required |

|

Videos (optional) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Week 1 |

Marketwatch Stock Trading Game (Pass code: havefun) 1. URL for your game: 2. Password for this private game: havefun. 3. Click on the 'Join Now' button to get

started. 4. If you are an existing MarketWatch member, login. If you are a new user,

follow the link for a Free account - it's easy! 5. Follow the instructions and start trading! 6. Game will be over

on 4/17/2019 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

2019

in Review: The Global Economy Explained in 5 Charts

Global growth this

year recorded its weakest pace since the global financial crisis a decade

ago, reflecting common influences across countries and country-specific

factors. Rising trade

barriers and associated uncertainty weighed on business sentiment and

activity globally. In some cases (advanced economies and China), these

developments magnified cyclical and structural slowdowns already under way. Further

pressures came from country-specific weakness in large emerging market

economies such as Brazil, India, Mexico, and Russia. Worsening macroeconomic

stress related to tighter financial conditions (Argentina), geopolitical

tensions (Iran), and social unrest (Venezuela, Libya, Yemen) rounded out the

difficult picture.

With the

economic environment becoming more uncertain, firms turned cautious on

long-range spending and global purchases of machinery and equipment

decelerated. Household demand for durable goods also weakened, although there

was a pick up in the second quarter of 2019. This was particularly evident

with automobiles, where regulatory changes, new emission standards, and

possibly the shift to ride-shares weighed on sales in several countries.

Faced with

sluggish demand for durable goods, firms scaled back industrial production.

Global trade—which is intensive in durable final goods and the components

used to produce them—slowed to a standstill.

Central banks

reacted aggressively to the weaker activity. Over the course of the year,

several—including the US Federal Reserve, the European Central Bank (ECB),

and large emerging market central banks—cut interest rates, while the ECB

also restarted asset purchases.

These policies

averted a deeper slowdown. Lower interest rates and supportive financial

conditions reinforced still-resilient purchases of nondurable goods and

services, encouraging job creation. Tight labor markets and gradually rising

wages, in turn, supported consumer confidence and household spending.

Will these

bright spots translate into stronger global growth next year? Find out more when

the IMF releases its World Economic Outlook Update on

January 20. We're not

predicting recession in 2020 but odds are growing, says Vanguard global chief

economist (Video)

For class discussion: What is

your opinion about the US economy in 2019? What is

your economic outlook of 2020? Recession? |

|

For class discussion: ·

Any

interesting facts? Any surprises? And why? ·

Find

the current exchange rates among the G7 countries and BRIC countries. ·

Convert

$100 to currencies of the G7 countries and BRIC countries. ·

Assuming

you are a consultant. What advice can you give to investors in Japan to make

money without risk? |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part II In class exercise –

convert currencies back and forth If

the dollar is pegged to gold at US $1200 = 1 ounce of gold and the British

pound is pegged to gold at £240 = 1 ounce of gold. What should be the

exchange rate between US$ and British £? How much can you make without any

risk if the exchange rate is 1£ = 6$? Assume that your initial investment is

$1200. Solution: Start with $1200à

option 1: get 1 ounce of gold à

trade for £240 in UK è

and then get £240 * 6$/£ = $1440, the money that you can put into your pocket

è $240 profits

($1440-$1200), this strategy works! Start with $1200à option 2: get £200 ($1200

and 1£ for 6$, so $1200/6=£200) è get gold (200/240 = 5/6 ounce of

gold) è get back

$, 1200*(5/6) = $1000è this

strategy will not work! You will lose $200 by doing so! Note

that with $1200, you can either buy gold first, or get £ first. |

|

Reference of useful websites for global economy International Trade

Statistics (PDF) Current Account (BOP) Data – World Bank http://data.worldbank.org/indicator/BN.CAB.XOKA.CD IMF, world bank and UN are only a few of the major organizations

that track, report and aid international economic and

financial development. Using these website, you can summarize the

economic outlook for each country. IMF: www.imf.org/external/index.htm UN: www.un.org/databases/index.htm World bank: www.worldbank.org Bank of international settlement: www.bis.org/index.htm St. Louis Federal Reserve provides a large amount of recent open

economy macroeconomic data online. You can track down BOP and GDP data for

the major industrial countries. Recent international economic data: research.stlouisfed.org/publicaitons/iet |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 2 Chapter 2 (PPT) Let’s watch this video together. Imports, Exports, and Exchange

Rates: Crash Course Economics #15 ·

What is BOP? The balance of payment of a country contains two accounts:

current and capital. The current account records

exports and imports of goods and services as well as unilateral transfers,

whereas the capital account records purchase

and sale transactions of foreign assets and liabilities during a particular

year. ·

What is the current account? Balance of

payments: Current account (video, Khan academy)

As the name implies, the current account considers goods and

services currently being produced. The current account deals with short-term transactions known

as actual transactions, as they have a real impact on income, output and

employment levels of a country through the movement of goods and services in the

economy. It consists of visible trade (export and import of goods), invisible trade (export

and import of services), unilateral transfers, and investment income (income from

factors such as land or foreign shares). The credit and debit of foreign exchangedue

to these transactions are also recorded in the balance of current account. The

resulting balance of the current account is approximated as the sum total of balance of trade.

https://www.bea.gov/data/intl-trade-investment/international-transactions

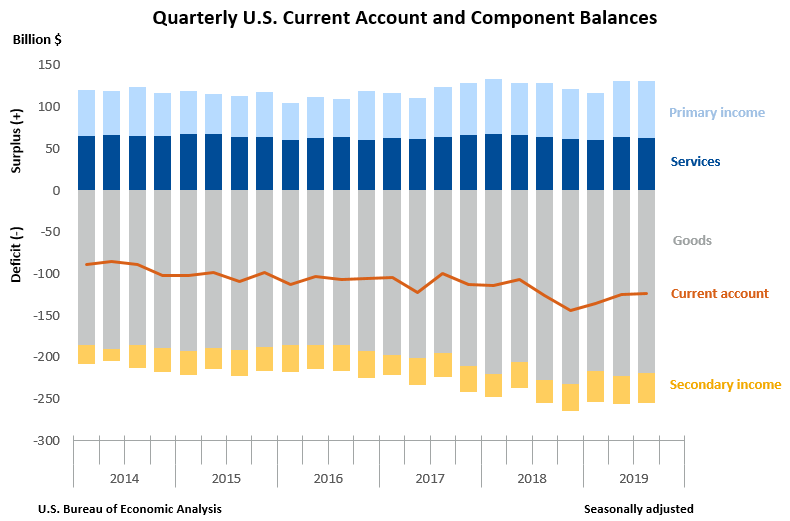

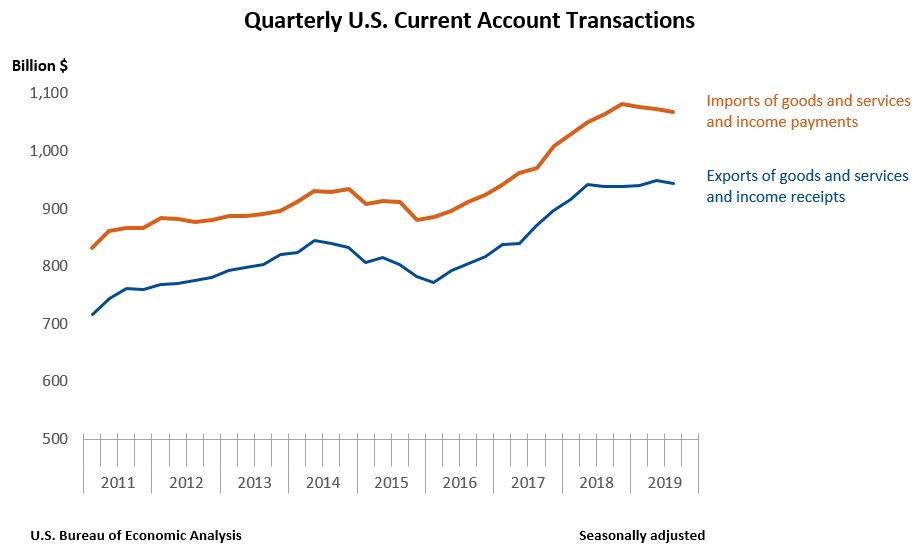

The U.S. current account deficit narrowed by $1.1 billion, or 0.9 percent, to $124.1 billion in the third quarter of 2019, according to statistics from the U.S. Bureau of Economic Analysis. The revised second quarter deficit was $125.2 billion. The third quarter deficit was 2.3 percent of current dollar gross domestic product, down less than 0.1 percent from the second quarter. For Details, please read the following article. U.S.

International Transactions, Third Quarter 2019

Current

Account Deficit Narrows by 0.9 Percent in Third Quarter The U.S.

current account deficit, which reflects the combined

balances on trade in goods and services and income flows between U.S.

residents and residents of other countries, narrowed by $1.1 billion, or 0.9

percent, to $124.1 billion in the third quarter of 2019, according to

statistics from the U.S. Bureau of Economic Analysis (BEA). The revised

second quarter deficit was $125.2 billion. The third

quarter deficit was 2.3 percent of current dollar gross domestic product,

down less than 0.1 percent from the second quarter. The $1.1

billion narrowing of the current account deficit in the third quarter mainly

reflected a reduced deficit on goods and an expanded surplus on primary

income.

Current Account

Transactions Exports of

goods and services to, and income received from, foreign residents decreased

$4.3 billion, to $944.4 billion, in the third quarter. Imports of goods and

services from, and income paid to, foreign/n residents decreased $5.4

billion, to $1.07 trillion.

Trade in Goods Exports of

goods decreased $0.9 billion, to $413.8 billion, and imports

of goods decreased $4.5 billion, to $633.4 billion. The

decreases in both exports and imports mainly reflected decreases in

industrial supplies and materials, primarily petroleum and products. Trade in Services Exports of services decreased

$0.3 billion, to $212.0 billion, reflecting partly offsetting changes across

major categories. Decreases were led by travel, mainly other personal travel,

and increases were led by other business services, mainly professional and

management consulting services. Imports of services increased

$1.6 billion, to $149.8 billion, reflecting increases in nearly all major

categories. Increases were led by insurance services, mainly reinsurance. Primary Income Receipts of primary income decreased $4.1 billion, to $282.0 billion, and payments

of primary income decreased $6.2 billion, to $213.3

billion. The decreases in both receipts and payments mainly reflected

decreases in direct investment income and in other investment income. Within

direct investment income receipts, dividends increased $24.9 billion, to

$95.3 billion, in the third quarter and remain elevated since the passage of

the 2017 Tax Cuts and Jobs Act, which generally eliminated taxes on

repatriated earnings beginning in 2018. For more information, see “How do the effects of the 2017 Tax Cuts and Jobs Act

appear in BEA’s direct investment statistics?” The decreases in other investment income receipts and

payments mainly reflected decreases in interest on loans and deposits. Secondary Income Receipts of secondary income increased $1.0 billion, to $36.6 billion, mainly

reflecting an increase in private sector fines and penalties, a component of

private transfer receipts. Payments of secondary income increased

$3.7 billion, to $72.0 billion, mainly reflecting increases in U.S.

government grants and in insurance-related transfers, a component of private

transfer payments. ·

What is the Capital Account

Balance of payments: Capital account (video,

Khan Academy) The capital account is a

record of the inflows and outflows of capital that directly affect a nation’s foreign assets and liabilities. It is concerned with all international trade

transactions between citizens of a given country and

citizens in other countries. The components of the capital account include foreign investment and loans,

banking capital and other forms of capital, as well as monetary movements or

changes in the foreign exchange

reserve. The capital account flow reflects factors such as

commercial borrowings, banking, investments, loans, and capital. In other words, the capital account is concerned with payments

of debts and claims, regardless of the time period. The balance of capital

account also includes all items reflecting changes in stocks.

https://fred.stlouisfed.org/tags/series?t=capital+account · The Bottom LineIn economic terms, the current account deals with receipt and

payment in cash as well as non-capital items, and the capital account

reflects sources and utilization of capital. The sum of the current

account and capital account as reflected in the balance of payments will

always be zero; any surplus or deficit in

the current account is matched and canceled out by an equal surplus or

deficit in the capital account. (https://www.investopedia.com/ask/answers/031615/whats-difference-between-current-account-and-capital-account.asp) The

20 largest trade partners of the United States represent 76.6% of

U.S. exports, and 81.0% of U.S. imports as of December 2014. These

figures do not include services or foreign direct investment. The

largest US partners with their total trade (sum of imports and exports)

in millions of $ for calendar year 2016 are as follows

Source:

indexmundi.com and world bank (2015) For

Class Discussion: 1. Can US win the trade war

against China? Can trade war help reduce US current deficit? 2. Can

US devaluate currency to eliminate current account deficit? Why does US reduce interest rate? Can cutting

interest rate help boosting US economy? · $

devalued, then export become cheaper and increased; imports more expensive

and decreased; seems like current account deficit could disappear. · However,

in short run, demand is not so flexible and thereby current account might get

worsen. · Demand

will improve with time, so current account improves with time, but not

immediately. · $

depreciated, it becomes less attractive to foreign government and investors.

The borrowing cost to cover the deficit will increase. · $

depreciated, living standard might drop. · Competitor

can drop price; Countries can devalue their currencies. · Your

idea? Topic:

Trade war with China to reduce trade deficit (current account deficit) Despite Trump's tariffs,

the U.S. trade deficit keeps growing (video)

U.S. China

Trade War Explained: How Tariffs Work & Impact the Economy (video)

Analysts say

US-China trade imbalance may not be what really matters (vido)

A Wall Street

Strategist Explains His Trade Deficit With Costco (Video)

Timeline of the

China-U.S. trade war (video)

HW I- Chapter 2

(Due with first mid term exam) 1.

About the trade war between US and China and the upcoming one between

US and Germany, what is your opinion? Can the trade wars help reduce the US

current account deficits? 2.

Based on the classroom discussion, and documents posted and available

online, do you think that the trade war against China could help US to reduce

its trade deficit (or current account deficit)? Please be specific. 3. Internet exercises (not

required, information for intereted students only) a. IMF,

world bank and UN are only a few of the major organizations that track, report and aid international economic and financial

development. Based on information provided in those websites, you could learn

about a country’s economic outlook. IMF: www.imf.org/external/index.htm UN: www.un.org/databases/index.htm World

bank: www.worldbank.org’ Bank

of international settlement: www.bis.org/index.htm b. St.

Louis Federal Reserve provides a large amount of recent open economy

macroeconomic data online. You can track down BOP and GDP data for the major

industrial countries. Recent

international economic data: research.stlouisfed.org/publications Balance

of Payments statistics: research.stlouisfed.org/fred2/categories/125 |

|

Balance of

payments: Current account (video, Khan academy) (FYI)

Balance of payments:

Capital account (video, Khan Academy) (FYI) US Trade Deficit With China and Why

It's So High

The Real Reason American Jobs Are

Going to China (For class discussion)

Updated November 21, 2018 The U.S. trade deficit with China was $375 billion in

2017. The trade deficit exists because U.S. exports to China were

only $130 billion while imports from China were $506 billion. The United States imported from China $77 billion in computers

and accessories, $70 billion in cell phones, and $54 billion in apparel and

footwear. A lot of these imports are from U.S. manufacturers that send raw

materials to China for low-cost assembly. Once shipped back to the United

States, they are considered imports. In 2017, China imported from America $16 billion in commercial aircraft, $12

billion in soybeans, and $10 billion in autos. In 2018, China canceled its

soybean imports after President Trump started a trade war. He imposed tariffs on Chinese steel exports and other

goods. Current Trade Deficit As of July 2018, the United States exported a total of $74.3

billion in goods to China. It imported $296.8 billion, according to the U.S. Census Bureau. As a result, the total trade deficit

with China is $222.6 billion. A monthly breakdown is in the chart. Causes China can produce many consumer goods at lower costs than

other countries can. Americans, of course, want these goods for the lowest

prices. How does China keep prices so low? Most economists agree that China's

competitive pricing is a result of two factors:

If the United States implemented trade protectionism, U.S.

consumers would have to pay high prices for their "Made in America"

goods. It’s unlikely that the trade deficit will change. Most people would

rather pay as little as possible for computers, electronics, and

clothing, even if it means other Americans lose their jobs. China is the world's largest economy. It also has the world's biggest

population. It must divide its production between almost 1.4 billion

residents. A common way to measure standard of living is gross domestic product per

capita. In 2017,

China’s GDP per capita was $16,600. China's leaders are desperately trying to

get the economy to grow faster to raise the country’s living standards.

They remember Mao's Cultural Revolution all too well. They know that the

Chinese people won't accept a lower standard of living forever. China sets the value of its currency, the yuan, to equal the value of a basket of

currencies that includes the dollar. In other words, China pegs its currency to the dollar using a

modified fixed exchange rate.

When the dollar loses value, China buys dollars through U.S. Treasurys to support it. In 2016, China

began relaxing its peg. It wants market forces to have a greater impact on

the yuan's value. As a result, the dollar to yuan conversion has been more volatile since

then. China's influence on the dollar remains substantial. Effect China must buy so many U.S. Treasury notes that it is the

largest lender to the U.S. government. Japan is the second largest. As

of September 2018, the U.S. debt to China was $1.15 trillion. That's

18 percent of the total public debt owned by foreign countries. Many are concerned that this gives China

political leverage over U.S. fiscal policy. They worry about

what would happen if China started selling its Treasury holdings. It

would also be disastrous if China merely cut back on its Treasury purchases. Why are they so worried? By buying Treasurys, China helped

keep U.S. interest rates low. If China were to stop buying

Treasurys, interest rates would rise. That could throw the United States into a recession. But

this wouldn’t be in China's best interests, as U.S. shoppers would buy fewer

Chinese exports. In fact, China is buying almost as many Treasurys

as ever. U.S. companies that can't compete with cheap Chinese goods

must either lower their costs or go out of business. Many businesses reduce

their costs by outsourcing jobs to China or India. Outsourcing adds to

U.S. unemployment. Other industries have just dried up. U.S.

manufacturing, as measured by the number of jobs, declined 34

percent between 1998 and 2010. As these industries declined, so has

U.S. competitiveness in the global marketplace. What's Being Done President Trump promised to lower the trade deficit with

China. On March 1, 2018, he announced he would impose a 25

percent tariff on steel imports and a 10 percent tariff on

aluminum. On July 6, Trump's tariffs went into effect for $34 billion of

Chinese imports. China canceled all import contracts for soybeans. Trump's tariffs have raised the costs of imported steel, most

of which is from China. Trump's move comes a month after he imposed

tariffs and quotas on imported solar panels and washing

machines. China has become a global leader in solar panel

production. The tariffs depressed the stock market when they were

announced. The Trump administration is developing further

anti-China protectionist measures, including more tariffs. It wants China to remove

requirements that U.S. companies transfer technology to Chinese firms. China

requires companies to do this to gain access to its market. Trump also asked China to do more to raise its currency. He

claims that China artificially undervalues the yuan by 15 percent to 40

percent. That was true in 2000. But former Treasury Secretary Hank Paulson initiated the U.S.-China Strategic

Economic Dialogue in 2006. He convinced the People's Bank of China to

strengthen the yuan's value against the dollar. It increased 2 to 3 percent annually

between 2000 and 2013. U.S. Treasury Secretary Jack Lew continued the

dialogue during the Obama administration. The Trump administration continued the talks until they

stalled in July 2017. The dollar strengthened 25 percent between 2013 and 2015.

It took the Chinese yuan up with it. China had to lower costs even more

to compete with Southeast Asian companies. The PBOC tried unpegging the yuan

from the dollar in 2015. The yuan immediately plummeted. That indicated that

the yuan was overvalued. If the yuan were undervalued, as Trump claims, it

would have risen instead. Potential questions for discussion: 1. How does China manipulate its currency according to this paper? 2. What would happen to interest rate if China stops purchasing Treasury securities? 3. Do you think the tariff worked as it was supposed to? 4. … A quick guide to the US-China trade

war (https://www.bbc.com/news/business-45899310)

·

16 December

2019 ·

·

The world's

two largest economies are locked in a bitter trade battle. The

dispute, which has simmered for nearly 18 months, has seen the US and China

impose tariffs on hundreds of billions of dollars worth of one another's

goods. US

President Donald Trump has long accused China of unfair trading practices and

intellectual property theft. In China,

there is a perception that the US is trying to curb its rise as a global

economic power. § The US-China trade war

in charts § US-China trade war:

'We're all paying for this' Negotiations

are ongoing but have proven difficult. In December, the two sides announced

a preliminary deal but some of the thorniest issues

remain unresolved. Uncertainty

surrounding the trade war has hurt businesses and weighed on the global

economy. What tariffs have been imposed?

Mr Trump's

tariffs policy aims to encourage consumers to buy American by making imported

goods more expensive. So far, the

US has imposed tariffs on more than $360bn (£268bn) of Chinese goods, and

China has retaliated with tariffs on more than $110bn of US products. Washington

delivered three rounds of tariffs last year, and a fourth one in September. The most recent round

targeted Chinese imports, from meat to musical instruments, with a 15% duty. Beijing

has hit back with tariffs ranging from 5% to 25% on US goods. Its latest

tariff strike included a 5% levy on US crude oil, the first time fuel has

been hit in the trade battle.

What's next?

The so-called "phase one" deal agreed in December

reduces some US tariffs in exchange for more Chinese purchases of American

products, and better protection for US intellectual property. § Trump

escalates trade war with fresh tariff hikes § US delays some

tariffs on Chinese imports The deal is yet to be signed and tariffs of 25% on $250bn

worth of Chinese goods remain in place. However, the US will drop tariffs on $120bn worth of

Chinese goods to 7.5%. Washington also shelved a planned round of tariffs, which

would have hit Chinese smart phones, clothing and toys. For class

discussion: What is the

purpose of the trade war against China? Has the

trade war achieved its goal yet? |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part II of Chapter 2 --- Evolution of international monetary system Finance: The History of Money (combined) (video, fan to

watch)

Review of history of money: A brief history of money - From gold to

bitcoin and cryptocurrencies (video)

· Bimetallism:

Before 1875 · Classical

Gold Standard: 1875-1914 The Gold Standard Explained in One Minute (video)

§ International

value of currency was determined by its fixed relationship to gold. § Gold was used to

settle international accounts, so the risk of trading with other countries

could be reduced. · Interwar

Period: 1915-1944 § Countries

suspended gold standard during the WWI, to increase money supply and pay for

the war. § Countries relied

on a partial gold standard and partly other countries’ currencies

during the WWII · Bretton Woods System: 1945-1972 The Bretton Woods Monetary System (1944 - 1971) Explained in

One Minute (video)

§ All currencies

were pegged to US$. § US$ was the only

currency that was backed by gold. § US$ was world

currency at that time. · The

Flexible Exchange Rate Regime: 1973-Present FLOATING AND FIXED EXCHANGE RATE (video)

For class discussion: Read the following. Is there any knowledge that is new to you? The Evolution

of US Currency

At times, America may not be

the most popular nation in the world, but one thing is for sure: it is famous

for its green. The greenback has been iconic since its inception. This infographic above misses a few key instances

in US currency history – namely the birth of the

Federal Reserve in 1913 and Nixon ending convertibility to gold in

1971. Both events were catalysts to massive money printing which leaves

the USD with only a fraction of the purchasing power that it once had.

|

|

Brexit: What happens now? By Peter BarnesSenior elections and political analyst, BBC

News ·

16 January 2020

The government's large majority meant that

the EU Withdrawal Bill sailed through the House of Commons. There will be attempts to amend the bill in

the Lords but any significant changes would almost certainly be overturned by

MPs. It is expected to become law within days. What happens after Brexit? Assuming the European Parliament also gives

the green light, the UK will formally leave the EU on 31 January with a

withdrawal deal - and it will then go into a transition period that is

scheduled to end on 31 December 2020. During this period the UK will effectively

remain in the EU's customs union and single market - but will be outside the

political institutions and there will be no British members of the European

Parliament. Future trade deal The first priority will be to negotiate a

trade deal with the EU. The UK wants as much access as possible for its goods

and services to the EU. But the government has made clear that the

UK must leave the customs union and single market and end the overall

jurisdiction of the European Court of Justice. Time is short. The EU could take weeks to

agree a formal negotiating mandate - all the remaining 27 member states and

the European Parliament have to be in agreement. That means formal talks

might only begin in March. The government has ruled out any form of

extension to the transition period. If no trade deal has been agreed and

ratified by the end of the year, then the UK faces the prospect of tariffs on

exports to the EU. The prime minister has argued that as the UK

is completely aligned to EU rules, the negotiation should be straightforward.

But critics have pointed out that the UK wishes to have the freedom to

diverge from EU rules so it can do deals with other countries - and that will

make negotiations more difficult. It's not just a trade deal that needs to be sorted out. The UK must agree how it is going to co-operate with the EU on security and law enforcement. The UK is set to leave the European Arrest Warrant scheme and will have to agree a replacement. It must also agree deals in a number of other areas where co-operation is needed. (https://www.bbc.com/news/uk-politics-46393399) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Second

Quiz Solution (FYI) 1. If U.S. imports > exports, then the supply of dollars > the demand of the dollars in the foreign exchange market, ceteris paribus. True / false Solution: Import means using $ (spending $, or out flow of $) to buy foreign goods è In the FX market, supply of $ increases è So when supply increases and assume that demand is unchanged, the value of $ will drop 2. If Japan exports > imports, then yen would appreciate against other currencies. True / false Solution: Export means selling domestic products for yen ( in flow of yen from importers who will pay yen for the goods made in Japan; there is an increased demand for yen) è In the FX market, demand of yen increases è So when demand increases and assume that supply is unchanged, the value of yen will rise. 3. If the interest rate rises in the U.S., ceteris paribus, then capital will flow out of the U.S. True / false Solution: Interest rate rises è financial market will become more attractive to foreign investors è capital will flow in, not flow out. Chapter 3 International Financial Market/ References: Go to www.forex.com and

set up a practice account and you can trade with $50,000 virtue money. Visit http://www.dailyfx.com/to

get daily foreign exchange market news. Part I: international financial centers As of today, the top ten global financial

centers were:

·

London. London has been a leading international

financial centre since

the 19th century, acting as a centre of lending and

investment around the world. English contract law was

adopted widely for international

finance, with legal services provided in

London. Financial institutions located there provided services

internationally such as Lloyd's of London (founded

1686) for insurance and the Baltic Exchange (founded 1744)

for shipping. During the 20th century London played an important role in

the development of new financial products such as the Eurodollar and Eurobonds in the 1960s,

international asset management and international equities trading in the

1980s, and derivatives in the 1990s. London continues to maintain a leading

position as a financial centre in the 21st century, and maintains the largest

trade surplus in financial services around the world. However, like New York,

it faces new competitors including fast-rising eastern financial centres such

as Hong Kong and Shanghai. London is the largest centre for derivatives markets, foreign

exchange markets, money markets, issuance of

international debt securities, international insurance, trading in gold, silver and base metals through

the London

bullion market and London

Metal Exchange, and

international bank lending. London

benefits from its position between the Asia and U.S. time zones, and has benefited from its location within the European Union, though this may end following the outcome of the Brexit referendum of 2016 and the

decision of the United Kingdom to leave the European Union. As well as

the London

Stock Exchange, the Bank of England, the second oldest

central bank, and the European

Banking Authority are in London, although the EBA is

moving to Paris in March 2019 after Brexit. ·

Tokyo. One report

suggests that Japanese authorities are working on plans to transform Tokyo

but have met with mixed success, noting that "initial drafts suggest

that Japan's economic specialists are having trouble figuring out the secret

of the Western financial centres' success." Efforts include

more English-speaking restaurants and services a/nd the building of many new

office buildings in Tokyo, but more powerful stimuli such as lower taxes have

been neglected and a relative aversion to finance remains prevalent in Japan. Tokyo

emerged as a major financial centre in the 1980s as the Japanese economy

became one of the largest in the world. As a financial centre, Tokyo has good links with New

York City and London. ·

Hong

Kong. As a financial centre,

Hong Kong has strong links with London and New York City. It developed its financial services industry while a

British territory and its present legal system, defined in Hong Kong Basic Law,

is based on English law.

In 1997, Hong Kong became a Special Administrative Region of the People's Republic

of China, retaining its laws and a high degree of autonomy

for at least 50 years after the transfer. Most of the world's 100 largest

banks have a presence in the city. Hong Kong is a

leading location for initial

public offerings, competing with New York City, and also for merger and acquisition activity ·

Singapore. With its strong links with London, Singapore has developed into the Asia region's largest

centre for foreign exchange and commodity trading, as well as a growing

wealth management hub.

Other than Tokyo, it

is one of the main centres for fixed income trading in Asia. However, the

market capitalisation of its stock exchange has been falling since 2014 and

several major companies plan to delist. (https://en.wikipedia.org/wiki/Financial_centre) For Discussion: What

makes an international financial centre? (video)

Is

China threatening Asia's financial center? | CNBC Explains

(video)

Do

we need so many financial centers in Asia? Part II: Floating exchange rate system vs. fixed

exchange rate system For Discussion: · US is using floating exchange rate system. What is the

advantage and disadvantage of this system? DO we need Cheap $ or strong $? · Chinese

currency is pegged to US$. What is the advantage and disadvantage of this

system? What about let it float, instead of holding its value at a fixed

rate? Can Chinese government control its currency? How? Is cheap RMB always

better than Strong RMB, to Chinese government? · Germany

is part of the Euro Zone. Can Germany manipulate Euro? · Who

are the major players in the FX market? · As

compared with stock market, FX market is more volatile or less? Why? A - set a fixed exchange rate between its currency and

another while allowing capital to flow freely across its borders, B - allow capital to flow freely and set

its own monetary policy, or C - set its own monetary policy and

maintain a fixed exchange rate. The Impossible Trinity or "The

Trilemma", in which two policy positions are possible. If a nation were

to adopt position a, for example,

then it would maintain a fixed exchange rate and allow free capital flows,

the consequence of which would be loss of monetary sovereignty.

The Impossible Trinity - 60 Second Adventures in Economics (5/6)

(video)

The impossible trinity (also

known as the trilemma) is a concept

in international

economics which states that it is impossible to have all

three of the following at the same time: ·

a fixed foreign exchange

rate ·

free capital movement (absence of capital controls) ·

an independent monetary policy It is both a hypothesis based on the uncovered interest

rate parity condition, and

a finding from empirical studies where governments that have tried to

simultaneously pursue all three goals have failed. The concept was developed

independently by both John Marcus Fleming in 1962 and Robert Alexander

Mundell in different articles between 1960 and 1963. Policy

choices

According to the impossible

trinity, a central bank can only pursue two of the above-mentioned three

policies simultaneously. To see why, consider this example: Assume that world interest

rate is at 5%. If the home central bank tries to set domestic interest rate

at a rate lower than 5%, for example at 2%, there will be a depreciation

pressure on the home currency, because investors would want to sell their low

yielding domestic currency and buy higher yielding foreign currency. If the

central bank also wants to have free capital flows, the only way the central

bank could prevent depreciation of the home currency is to sell its foreign

currency reserves. Since foreign currency reserves of a central bank are

limited, once the reserves are depleted, the domestic currency will

depreciate. Hence, all three of the

policy objectives mentioned above cannot be pursued simultaneously. A central

bank has to forgo one of the three objectives. Therefore, a central bank has

three policy combination options. Options

In terms of the diagram above

(Oxelheim, 1990), the options are: ·

Option (a): A stable exchange rate and free capital flows (but

not an independent monetary policy because setting a domestic interest rate

that is different from the world interest rate would undermine a stable

exchange rate due to appreciation or depreciation pressure on the domestic

currency). ·

Option (b): An independent monetary policy and free capital

flows (but not a stable exchange rate). ·

Option (c): A stable exchange rate and independent monetary policy

(but no free capital flows, which would require the use of capital

controls. Currently, Eurozone members

have chosen the first option (a) while most other countries have opted for

the second one (b). By contrast, Harvard economist Dani Rodrik advocates the use of the

third option (c) in his book The Globalization Paradox, emphasising

that world GDP grew fastest during the Bretton Woods era when capital

controls were accepted in mainstream economics. Rodrik also argues that the

expansion of financial globalization and the free movement of

capital flows are the reason why economic crises have become more frequent in

both developing and advanced economies alike. Rodrik has also developed the

"political trilemma of the world economy", where

"democracy, national sovereignty and global economic

integration are mutually incompatible: we can combine any two of the

three, but never have all three simultaneously and in full." (from Wikipedia)

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

USD/JPY = 119.50 è USD is the

Base currency / JPY is the Quote currency è 1 UDS =

119.5 JPY ·

This is an indirect quote |

This is

referred to as a currency pair.

The currency to the left of the slash is the base currency, while the currency

on the right is called the quote or counter currency. The

base currency (in this case, the U.S. dollar) is always equal to one unit (in

this case, US$1), and the quoted currency (in this case, the Japanese yen) is

what that one base unit is equivalent to in the other currency. The quote

means that US$1 = 119.50 Japanese yen. In other words, US$1 can buy 119.50

Japanese yen. The forex quote includes the currency abbreviations for the

currencies in question.

Direct

Currency Quote vs. Indirect Currency Quote

There are two

ways to quote a currency pair, either directly or indirectly. A direct currency quote is simply a currency pair in which

the domestic currency is the

quoted currency; while an

indirect quote, is a currency pair where the domestic currency is the base currency. So if you were looking at

the Canadian dollar as the domestic currency and U.S. dollar as the foreign

currency, a direct quote would be USD/CAD, while an indirect quote would be

CAD/USD. The direct quote varies the domestic currency, and the base, or

foreign currency, remains fixed at one unit. In the indirect quote, on the

other hand, the foreign currency is variable and the

domestic currency is fixed at one unit.

·

Direct currency quote:

foreign currency / domestic currency, such as JPY / USD (one JPY for

how many USD)

·

Indirect currency quote: domestic currency / foreign currency,

such as USD/JPY (one USD for how many JPY)

For example,

if Canada is the domestic currency, a direct quote would be 1.18

USD/CAD and means that USD$1 will purchase C$1.18 . The indirect quote

for this would be the inverse (1/1.18), 0.85 CAD/USD, which means with C$1,

you can purchase US$0.85.

In

the forex spot market, most currencies are traded against the U.S.

dollar, and the U.S. dollar is frequently the base currency in the currency

pair. In these cases, it is called a direct quote. This would apply to the

above USD/JPY currency pair, which indicates that US$1 is equal to 119.50

Japanese yen.

However, not

all currencies have the U.S. dollar as the base. The Queen's currencies -

those currencies that historically have had a tie with Britain, such as

the British pound, Australian Dollar and New Zealand dollar - are

all quoted as the base currency against the U.S. dollar. The euro is quoted

the same way as well. In these cases, the U.S. dollar is the counter

currency, and the exchange rate is referred to as an indirect quote. This is

why the EUR/USD quote is given as 1.25, for example, because it means that

one euro is the equivalent of 1.25 U.S. dollars.

Most currency

exchange rates are quoted out to four digits after the decimal place,

with the exception of the Japanese yen (JPY), which is quoted out to two

decimal places.

Cross Currency

( You can find the cross

exchange rates at www.forex.com

When a currency quote is given without the U.S. dollar as one of its components,

this is called a cross currency. The most common cross

currency pairs are the EUR/GBP, EUR/CHF and EUR/JPY. These currency pairs

expand the trading possibilities in the forex market, but it is important to

note that they do not have as much of a following (for example, not as

actively traded) as pairs that include the U.S. dollar, which also are called

the majors. (For more on cross currency, see Make The Currency Cross Your Boss.)

(https://www.investopedia.com/university/forexmarket/forex2.asp)

Summary:

USD / JPY

= 119.50 è 1 US$ = 119.5 YEN, to US residents this is an indirect quote; to a Japanese, it is a direct quote.

Base / quote

JPY / USD

= 1/119.50 è 1 YEN = (1/119.5)$, to US residents this is a direct quote; to a Japanese, it is a indirect quote.

Base / quote

Direct quote

= 1/(indirect quote) or indirect quote = 1/ (direct quote) *** Inverse relationship

Part IV: what is BID and ASK price on

Forex

Forex: Bid and Ask (video)

Bid and Ask

As with most trading in the financial markets, when you are trading a

currency pair there is a bid price (buy) and an ask price (sell).

Again, these are in relation to the base currency. When buying a currency pair (going long), the

ask price refers to the amount of quoted currency that has to be paid

in order to buy one unit of the base

currency, or how much the market will sell one unit of the base

currency for in relation to the quoted currency.

The bid price is used when

selling a currency pair (going short) and reflects how much of the

quoted currency will be obtained when selling one unit of the base currency,

or how much the market will pay for the quoted currency in relation to the

base currency.

The quote before the slash is the bid price, and the two

digits after the slash represent the ask price (only the last two digits of

the full price are typically quoted). Note that the bid price is always

smaller than the ask price. Let's look at an example:

|

USD/CAD = 1.2000/05 |

If you want to

buy this currency pair, this means that you intend to buy the base currency

and are therefore looking at the ask price to see how much (in Canadian

dollars) the market will charge for U.S. dollars. According to the ask price,

you can buy one U.S. dollar with 1.2005 Canadian dollars.

However, in

order to sell this currency pair, or sell the base currency in exchange for

the quoted currency, you would look at the bid price. It tells you that the

market will buy US$1 base currency (you will be selling the market the base

currency) for a price equivalent to 1.2000 Canadian dollars, which is the

quoted currency.

Whichever

currency is quoted first (the base currency) is always the one in which the

transaction is being conducted. You either buy or sell the base currency.

Depending on what currency you want to use to buy or sell the base with, you

refer to the corresponding currency pair spot exchange rate to determine the

price.

(https://www.investopedia.com/university/forexmarket/forex2.asp)

Exercise I:

Assume you have

$1000 and bid rate is $1.52/£ and ask rate is $1.60 /£.

GBP/USD = 1.5200/1.6000

Meanwhile, the bid rate is quoted as 0.625 £/$ and the ask rate

is quoted as 0.6579 £/$.

USD/GBP = 0.6250 /0.6579

If you convert it to £ and then convert it back to $, what will

happen?

Answer:

Sell at bid and buy at ask price (ask is always higher than

bid so you buy high and sell low, since you are dealing with the bank).

You

can either buy and sell dollar:

with

$1000, you sell at bid 0.625 £/$ so you get 625£

($1000* 0.625 £/$ =

625£). With 625£, you sell at bid $1.52/£, so you get $950 (625£ * $1.52/£ =

$950)

Exercise II: you

Suppose the spot ask exchange rate is $1.90 = £1.00

and the spot bid exchange rate is $1.89 = £1.00. If you were to buy

$1,000,000 worth of £ and then sell them 10 minutes later, how much of your

$1,000,000 would be lost by the bid-ask spread? (Hint: You buy at ask and

sell at bid)

Answer:

GBP

at $1.60 /£ and buy $ at 0.6579 £/$. So $1000 / 1.6

$/£ * 0.6579 £/$ = $950

GBP

at $1.60 /£ and buy $ at 0.6579 £/$. So $1000 / 1.6

$/£ * 0.6579 £/$ = $950

Exercise III: The dollar-euro exchange rate is $1.25 =

€1.00 and the dollar-yen exchange rate is ¥100 =

$1.00. What is the euro-yen cross rate? (answer: ¥125 = €1.00)

Exercise IV: The AUD/$ spot exchange rate is AUD1.60/$

and the SF/$ is SF1.25/$. The AUD/SF

cross exchange rate is: (answer: 1.2800)

Part V: LIBOR, Eurodollar, Eurobond

What is US dollar LIBOR? (What is LIBOR? Video, and other video (Libor, khan academy)

The London Interbank Offered Rate (LIBOR) is an

interest rate based on the average interest rates at which a large number of international

banks in London lend money to one another. The official LIBOR rates are

calculated on a daily basis and made public at 11:00 (London Time) by the ICE

Benchmark Administration (IBA). We publish the LIBOR rates on this website

with a delay (we are not allowed to publish realtime LIBOR rates).

The daily reported interest rates are the mean

of the middle values. The rates are a benchmark rather than a tradable rate,

the actual rate at which banks will lend to one another continues to vary

throughout the day. The LIBOR rates come in different maturities (overnight,

1 week and 1, 2, 3, 6, and 12 months) and different currencies (the euro, US

dollar, British pound sterling, Japanese yen and Swiss franc).

In the past, the BBA published LIBOR rates for

5 more currencies (Swedish krona, Danish krone, Canadian dollar, Australian

dollar and New Zealand dollar) and 8 more maturities (2 weeks, 4, 5, 7, 8, 9,

10 and 11 months).

On this page we show the US dollar LIBOR rates. The US dollar LIBOR rates

can be considered as the interbank cost of borrowing funds in US dollars.

The LIBOR interest rates are being used as a

reference rate for a lot of financial products, for example derivatives like

swaps. A lot of banks use the LIBOR interest rates also to determine their

rates on products like mortgages, savings accounts and loans.

![]() Current US dollar LIBOR

interest rates:

Current US dollar LIBOR

interest rates:

In the following table we show the current US dollar

LIBOR interest rates (not realtime, daily updated).

|

US dollar LIBOR |

01-24-2020 |

01-23-2020 |

01-22-2020 |

01-21-2020 |

01-20-2020 |

|

1.53188 % |

1.53163 % |

1.53263 % |

1.53925 % |

- |

|

|

1.56175 % |

1.56088 % |

1.55325 % |

1.55238 % |

1.56225 % |

|

|

- |

- |

- |

- |

- |

|

|

1.65950 % |

1.66088 % |

1.65938 % |

1.65950 % |

1.65338 % |

|

|

1.78038 % |

1.76575 % |

1.76988 % |

1.78250 % |

1.78638 % |

|

|

1.79538 % |

1.79413 % |

1.80088 % |

1.80625 % |

1.80213 % |

|

|

- |

- |

- |

- |

- |

|

|

- |

- |

- |

- |

- |

|

|

1.80525 % |

1.82175 % |

1.82463 % |

1.83438 % |

1.82950 % |

|

|

- |

- |

- |

- |

- |

|

|

- |

- |

- |

- |

- |

|

|

- |

- |

- |

- |

- |

|

|

- |

- |

- |

- |

- |

|

|

- |

- |

- |

- |

- |

|

|

1.87988 % |

1.89450 % |

1.91900 % |

1.91838 % |

1.92463 % |

The London Interbank Offered Rate is the average interest rate at which leading banks borrow funds from other banks in the London market. LIBOR is the most widely used global "benchmark" or reference rate for short term interest rates.

Eurodollar

-- Eurodollar explained (video)

The term

eurodollar refers to U.S. dollar-denominated deposits at foreign banks or at

the overseas branches of American banks. By being located outside the United States,

eurodollars escape regulation by the Federal Reserve Board, including

reserve requirements. Dollar-denominated deposits not subject to U.S. banking

regulations were originally held almost exclusively in Europe, hence the name

eurodollar. They are also widely held in branches located in the Bahamas and

the Cayman Islands.

(https://www.investopedia.com/terms/e/eurodollar.asp)

For discussion:

· Between LIBOR USD rate and US interest rate for similar terms, there should not be any discrepancies. Right?

What is a Eurobond What is EUROBOND? What does EUOBOND mean? (video)

A eurobond is denominated in a currency other than the home

currency of the country or market in which it is issued. These bonds are

frequently grouped together by the currency in which they are denominated,

such as eurodollar or euroyen bonds. Issuance is usually handled by an

international syndicate of

financial institutions on behalf of the borrower, one of which may underwrite

the bond, thus guaranteeing purchase of the entire issue. https://www.investopedia.com/terms/e/eurobond.asp

HOMEWORK II (CHAPTER 3) (Due with first

mid term exam)

1. Bid/Ask Spread

Compute the bid/ask percentage spread for

Mexican peso retail transactions in which the ask rate is $.11 and the bid

rate is $.10. HINT: BID ASK SPREAD = (ASK-BID)/ASK (Answer:

9.09%)

2. Indirect Exchange Rate

If the direct exchange rate of the euro is

worth $1.25, what is the indirect rate of the euro? That is, what is the

value of a dollar in euros? (Answer:

0.8€)

3. Cross Exchange Rate

Assume Poland currency (the zloty) is worth

$.17 and the Japanese yen is worth $.008. What is the cross rate of the zloty

with respect to yen? That is, how many yen equal a zloty? (Answer:

21.25¥)

4. Foreign Exchange

You just came back from Canada, where the

Canadian dollar was worth $.70.

You still have C$200 from your trip and could

exchange them for dollars at the airport, but the airport foreign exchange

desk will only buy them for $.60. Next week, you will be going to Mexico and

will need pesos. The airport foreign exchange desk will sell you pesos for

$.10 per peso. You met a tourist at the airport who is from Mexico and is on

his way to Canada. He is willing to buy your C$200 for 1,300 pesos. Should

you accept the offer or cash the Canadian dollars in at the airport?

Explain. (Answer: You can only get $1,200 peso if you accept the

offer in the airport)

New

York stretches lead over London as the world’s top financial center, survey

shows

PUBLISHED

THU, SEP 19 20199:11 AM EDTUPDATED THU, SEP 19 201910:25 AM EDT

David

Reid@DAVYREID73

New

York has stretched its lead over London in the race to be the world’s top financial

center, according to a poll conducted by Z/Yen group and the China

Development Institute (CDI).

The Big

Apple scored 790 points to top the 26th edition of the Global Financial

Centres Index. The index studied 104 different cities.

New

York increased its lead over London to 17 points, with the home of Wall

Street considered top in all 5 factors measured: Business Environment, Human

Capital, Infrastructure, Financial Sector, Development, and Reputation.

The

U.K. capital only just retained second in the ranking as Brexit continued to

diminish its standing. London with a score of 773 only just edged out Hong

Kong in third place with a score of 771.

Professor

Michael Mainelli, executive chairman of Z/Yen, said competition at the top of

the index is intensifying and London could soon be surpassed by more than one

city.

“London

is in a ‘slipping second’ position globally and a ‘slipping first’ in Europe

amidst high volatility emanating from policy uncertainties, Brexit, trade

wars, and geopolitical unrest. Asian centres and a resurging Paris are

fighting for that second-place spot,” he said in a press release Thursday.

Singapore

and Shanghai remain in fourth and fifth position respectively and seven of

the top ten places in the index are now taken by Asia/Pacific locations.

A new

separate index was included for the first time, measuring the top locations

for FinTech firms. Chinese centers occupy five of the top seven places in

that index, led by Beijing and Shanghai. New York, London, Singapore, San

Francisco, and Chicago also feature in the top ten for FinTech.

Results

to both surveys were collated via an online questionnaire during the 24

months to June 2019. The survey collectors said 3,360 respondents gave valid

answers during this time.

London

retains global finance throne amid Brexit chaos

Andrew

MacAskill, Sinead Cruise, Huw Jones, Oct, 2019

LONDON (Reuters) - From the pinnacle of the

City of London’s largest skyscraper, Stuart Lipton is wagering a $1.2 billion

bet that the British capital remains a master of the international financial

universe no matter what happens with Brexit.

The

76-year-old property developer is not alone. Bankrolled by a host of global

investors, including France’s Axa (AXAF.PA), his big-ticket gamble in London’s

financial district is - so far - on the money.

The

cataclysmic warnings during the 2016 referendum that London would lose its

financial throne if it voted to leave the European Union (EU) have, so far,

been proven wrong. London is still the world’s banker, only bigger by some

measures.

“London

is extraordinarily resilient and its future as a finance centre is secure

because what we have here is unique,” Lipton told Reuters on the 61st floor

of 22 Bishopsgate, set to become western Europe’s second tallest skyscraper

when it opens next year.

In the

year to June, London has attracted more cross border commercial real estate

investment than any other city. It has overtaken New York as destination for

fintech investment and it has increased its dominance of the world’s $6.6

trillion daily foreign exchange market.

Since

the vote to leave the EU, Britain has leapfrogged the United States to become

the largest centre for trading interest rate swaps, despite calls by

ex-French President Francois Hollande to end London’s dominance in clearing

euro-denominated derivatives.

That

London has expanded its influence as an international finance centre is one

of the biggest riddles of the United Kingdom’s tortuous three year Brexit

crisis.

The

city’s standing ensures the United Kingdom keeps one of its last big chips at

the top table of world politics just as it splits from the EU.

It also

means EU companies will still come to London to raise finance outside the

bloc after Brexit, a fact not lost on Wall Street heavyweights such as

Goldman Sachs (GS.N) and JP Morgan (JPM.N).

Just a

mile away from 22 Bishopsgate, Goldman opened its new 1 million square foot

European headquarters - complete with mothers’ rooms and wildflowers on the

roof - in July, three years on from the 2016 referendum.

Largely

abandoned by the British government during Brexit talks, ten senior industry

officials told Reuters London’s financial services sector has grown since

2016 because there is no realistic competitor in its time zone.

And

high-rolling bankers are too attached to its Anglo-Saxon, work-hard,

play-hard culture.

The

chief executive of the British division of one of Europe’s largest banks said

although some business will move to the EU, most senior bankers will be

reluctant to leave London. He would consider taking a 20% pay cut to remain

in the city.

“If you

are an Italian banker, who moved out to London 20 years ago, and your kids go

to a private school around the corner then you are not going to move to

Frankfurt.” He said.

The

2016 referendum shocked many of the masters of London’s financial universe,

triggering the biggest one-day fall of the pound since the era of

free-floating exchange rates was introduced in the early 1970s.

But so

far, most major financial institutions have opted against moving large

numbers of people and activities until the loss of access to the EU’s

lucrative single market is confirmed.

Banks,

insurers and asset managers have shifted over a trillion euros of assets such

as derivatives and bonds from London to the continent and opened new EU hubs

as a hedge against London suddenly being cut off from the bloc if Britain

exits the EU without a formal agreement.

The

Bank of England estimates around 4,000 people may have moved by the time

Britain has exited the EU. But the key decisions are still taken in London.

Reuters

contacted JP Morgan and Goldman, and rivals Citi (C.N), Bank of America

(BAC.N), UBS (UBSG.S), Morgan Stanley (MS.N), Credit Suisse (CSGN.S) and

Deutsche Bank (DBKGn.DE), to seek details on how a ‘no deal Brexit’ might

accelerate the transfer of resources and activities from London.

All

banks said they were prepared for a no-deal Brexit, and had been since the

first quarter.

BUSINESS NEWSOCTOBER 8, 2019 / 2:04 AM / 4 MONTHS AGO

The end of Libor:

the biggest banking challenge you've never heard of

Sinead Cruise, Lawrence White

LONDON (Reuters) - On June 30, British bank NatWest (RBS.L) sent

out an arcane-sounding press release - bus operator National Express (NEX.L)

had become the first company to take out a loan based on Sonia, a replacement

for scandal-hit interest rate benchmark Libor.

FILE PHOTO: British five pound banknotes are seen in this

picture illustration taken November 14, 2017. REUTERS/Benoit

Tessier/Illustration/File Photo

It was billed as the first switch of thousands that British

firms would make by end-2021, when the benchmark is set to be decommissioned.

Four months on, NatWest’s trailblazing

Sonia switch has been followed by only one other loan, when the bank struck a

deal with utility South West Water on Oct. 2.

The slow progress highlights the challenge banks and borrowers

face as regulators attempt to end the use of Libor, a benchmark embedded in

as much as $340 trillion financial contracts worldwide from home loans to complicated

derivatives.

Libor, once dubbed the world’s most

important number, was discredited after the 2008 financial crisis when

authorities in the United States and Britain found traders had manipulated it

to make a profit.

But replacing Libor is proving expensive and tricky with

concerns that, if mishandled, it could trigger credit market confusion and

waves of lawsuits, finance industry sources said.

RELATED COVERAGE

Factbox: The global benchmarks replacing Libor

With no obvious alternative, some countries are adopting their

own benchmarks. The United States is leading the way with a booming trade in

derivatives linked to its new Sofr rate, while the European Central Bank

started publishing Estr, its new interest rate benchmark, earlier this month.

In Britain, professional investors such as hedge funds and

pension insurance clients are also already writing and trading derivatives

contracts linked to Sonia. But companies which make up the so-called Libor “cash” market of

sterling-denominated loans are dragging their feet or are even not aware of

the shift.

At least two banks in Britain have shifted staff from teams

preparing for Brexit to specialist Libor taskforces in the past quarter as

the issue becomes more pressing, industry sources said.

“Part of the market is very

educated and smart on this and part of the market is not even aware that

Libor is going,” said Phil Lloyd, head of market

structure & regulatory customer engagement at NatWest Markets.

Lloyd said banks like NatWest are battling to allay concerns

among corporate borrowers that the Sonia benchmark will make it harder for

them to know how much interest they owe because the rate is backward looking.

Sonia, the sterling overnight index average, is based on the

average of interest rates banks pay to borrow sterling from one another

outside market hours, and is published at 9:00 a.m. local time (0800 GMT)

daily, after the transactions have been vetted by the Bank of England.

Borrowers taking out Sonia loans will in effect not know exactly

how much interest they owe until they are required to pay.

In contrast, loans linked to Libor can have forward-looking term

rates, meaning borrowers have greater certainty over their future liabilities

and can manage cash flows more easily.

Bankers and consultants said the market was exploring a

forward-looking Sonia term rate by mid-2020 to appease borrowers but not

everyone is in favor.

The overnight Sonia rate, based on actual transactions, is seen

as more robust and less vulnerable to the kind of manipulation that affected

Libor, which was based on rates submitted by banks.

The Libor rigging scandal saw billions of dollars in fines

levied on major banks and jail sentences for traders convicted of

manipulating the benchmark for profit.

Some banks and lawyers fear the creation of a Sonia term rate,

which would likely be based on forward-looking estimates from banks as

opposed to past transactions, could undermine the security of the benchmark

and even spawn legal dangers for banks.

Murray Longton, a consultant at Capco who advises financial

firms on Libor transition, said banks were fearful of lawsuits, as the

proliferation of alternative Sonia term rates offered by different lenders

could spark allegations of mis-selling.

“If

you get this wrong, this is PPI for investment banking- if you haven’t communicated properly and you move a customer (on to

Sonia) and benefit, there could be a case where this gets reviewed and you

owe your client a lot,” he said.

The Payment Protection Insurance (PPI) mis-selling scandal in

Britain has cost banks more than 43 billion pounds in compensation after the

contracts were retrospectively deemed to have been mis-sold.

“A lot of the corporate market

are waiting for a few things of which one is a term rate. And if they never

get a term rate, then waiting will lead to them still executing Libor, and

not being ready for Sonia. The clock is ticking,”

Lloyd said.

“And the other point about

having a term rate is you’re starting to get back

into a world where you are really recreating a new version of Libor.”

COSTS AND CONSEQUENCES

But the reluctance of corporate borrowers to buy into Sonia is

not the only reason for the slow progress.

Banks face large costs for adapting systems and educating

thousands of relationship managers on the merits of Sonia over Libor.

Fourteen of the world’s top banks expect

to spend more than $1.2 billion on the Libor transition, data from Oliver

Wyman show, with the costs for the finance industry as a whole set to be

several multiples of that sum.

Much of this cost is linked to the arduous task of changing the

terms of contracts tied to Libor whose duration extend beyond the 2021

deadline. Progress has been held up not only by nervous borrowers but also by

banks in loan syndicates which may not always agree on the new wording

required to adapt existing loan agreements to the new benchmark.

“You need unanimous agreement

to change the baseline product, so what are the chances if you’ve got 10-15 participants (in a syndicate) that they will

all agree on the same thing?,” Capco’s

Longton said.

Some corporate borrowers are also playing a wait-and-see game to

see whether they can benefit financially from Libor’s

slow death spiral. But this could have costly consequences, depending on the

so-called “fallback” language

in contracts for their existing loans.

These fallbacks - originally designed to kick in if Libor was

temporarily unavailable - usually stipulate alternative rates, such as

calling other banks for a quote or using the last published Libor rate. But

the fallback clauses were not designed to cope with Libor ceasing to exist

indefinitely.

That could create big risks for borrowers, for example, by

potentially converting a “floating rate” loan, tied to the fluctuations of Libor into a fixed-rate

one.

Serge Gwynne, a partner at consultant Oliver Wyman, said

regulators could do more to help banks manage the transition away from Libor,

starting with much harder deadlines on when it would formally cease to exist.

“Libor

is embedded everywhere in the plumbing of the financial world, that’s why this is such a big challenge,”

said Longton.

“You are changing a product

that has been used to create markets for a long time. You are not just taking

one thing out and putting one thing in but changing the whole dynamic of how this

works.”

Chapter 4 Exchange Rate Determination

Part I:

What determines the strength of a currency?

Currency value is determined by demand and supply, if not

under control by the government.

What Determines The Strength Of A

Currency?

Q: What factors

determine the strength of a currency?

A: Currency

trading is complicated by the fact that there are so many factors involved.

Not only are there a number of country-specific variables that go into

determining a currency's strength, but there are also other benchmarks--other

currencies, for example, as well as commodities--against which a currency's

strength can be measured.

However, three

crucial factors are as follows:

1.

Interest rates. High

interest rates help promote a strong currency, because foreign investors can

get a higher return by investing in that country. However, the level of

interest rates is relative. You've probably noticed that interest rates on

CDs, savings accounts and money market accounts are

very low right now. So are U.S. Treasury bond rates and the U.S. federal funds rate. Ordinarily,

this would weaken the U.S. dollar, except for the fact that interest rates

behind other major world currencies are also low.

3.

Stability. A

strong government with a well-established rule of law and a history of

constructive economic policies are the type of things that attract investment

and thus promote a strong currency. In the case of the U.S. dollar, its

strength is further augmented by the fact that commodities are generally

traded in dollars, and many countries use the dollar as a reserve currency.

Speaking

of stability, that is probably what governments seek for their currencies,

more so than strength. A strong currency makes a country's exports more

expensive, hurting that nation's trade competitiveness. On the other hand, a

weak currency makes imports more expensive, boosting domestic inflation. So

the ideal course is to aim down the middle and avoid destabilizing

fluctuations.

Think about the changes in demand and supply

when the following changes occur.

· Inflation goes up (or

down)

· Real interest rate

goes up (or down)

· Domestic residents’

income goes up (or down)

· Current account goes

up (or down)

· Public debt goes up