FIN415 Class Web

Page, Spring '22

Jacksonville

University

Instructor:

Maggie Foley

Term Project Part I (due with

final)

Term project part II (excel

questions) (due with final)

Weekly SCHEDULE,

LINKS, FILES and Questions

|

Week |

Coverage, HW, Supplements -

Required |

|

Videos (optional) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Week 1 |

Marketwatch Stock Trading Game (Pass

code: havefun) 1. URL for your game: 2. Password for this private

game: havefun. 3. Click on the 'Join Now'

button to get started. 4. If you are an

existing MarketWatch member, login. If you are a new user, follow

the link for a Free account - it's easy! 5. Follow the instructions and

start trading! 6. Game will be over

on 4/17/2019 How to Use

Finviz Stock Screener (youtube, FYI)

How To Win

The MarketWatch Stock Market Game (youtube, FYI)

How Short

Selling Works (Short Selling for Beginners) (youtube,

FYI)

|

|

1/11Class

video:

syllabus and market watch game 1/13 class

video: 2021 global review – world bank; Currency

conversion exercise 1/18 Class

video: Bi-lateral vs. Multi-lateral trading system;

RCEP 1/20 class

video: Balance of payment, current account 1/25 Class

video:

International monetary system, Bretton Woods aggrement, gold standard,

digital currency 1/27 class

video: Global financial market, Brexit, LIBOR and

SOFR 2/1 Class

video: Exchange rates determinants; Impossible

trinity; Dollar appreciation 2022 2/3 class

video: Currency conversion; Bid-Ask spread; 2/8 Class

video:

Eurocurrency, Naples waste

management & Italy’s first bank (PPT, by Theodore and Christian. Thank

you) 2/10 class

video: class

is cancelled --- instructor needs to attend AEF

conference 2/15 Class

video:

Exchange rates determinants revisited; Argentina’s hyperinflation 2/17 class

video:

will $ collapse? Yen carry trade; in class exercise 2/22 Class

video: First Mid Term Exam 2/24 class

video:

Futures contract 3/1

Class video: call & put option 3/3

Class video: currency carry trade examples 3/8

Class video: interest rate parity 3/10

Class video: Ukraine War (Thanks, Theodore and Christian), and IRP 3/15 Class video Spring Break 3/17 Class video Spring Break 3/22

Class video IRP 3/24

Class video PPP, Big Mac Index 3/29

Class video International Fisher Effect, exam review 3/31 Class video Second Midterm exam (on blackboard, under second

midterm exam folder) 4/5 Class video chapter 11: Transaction Exposure, part I 4/7

Class video class is cancelled --- instructor needs to attend EFA conference

4/12 Class video chapter 18: interest rate swap, exercise of

interest rate swap 4/14

Class video Happy Charter Day 4/19 Class video

chapter 18: currency swap, Goldman sacks and Greece Debt crisis 4/21 Class video

term project Excel Final

Exam on 4/28/2022 on blackboard |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part I: 2021 Review (from worldbank.com) https://www.worldbank.org/en/news/feature/2021/12/20/year-2021-in-review-the-inequality-pandemic 2021

has shown that the impact of the pandemic is far-reaching and has touched

every possible area of development. With the poor and the vulnerable bearing

the brunt of it, the pandemic is dealing a severe setback to ending poverty

and boosting shared prosperity. But it isn’t all doom and gloom. As the year went on, there were some

positive developments — global economy grew, goods trade rebounded, food

commodity prices have begun to stabilize, and remittances registered a robust

recovery. However, with newer

variants and unequal access to vaccines, there is still more to work to be

done. At

the same time, as some countries are beginning to chart their recovery, it is also an opportunity for them to

achieve lasting economic growth without degrading the environment or

aggravating inequality. The Bank Group is helping countries chart a

recovery that is green, resilient, and inclusive through achieving economic

stability and growth, leveraging the digital revolution, making development

greener and more sustainable, and investing in people. For discussion: ·

Do you think that

the Covid-19 crisis is a temporary shock, or a permanent one? ·

How soon can we

recover from this crisis? ·

Comparing with

financial crisis of 2008, which one is more severe? Uneven Global Recovery

As is the case

with access to vaccines, there is an emerging gap in the economic recovery

between high-income and low- and

middle-income economies. The June edition of the

Global Economic Prospects noted that while the global economy is set to

expand 5.6 percent in 2021—its strongest post-recession pace in 80 years, the

recovery will be uneven. Low-income economies are forecast to expand by only

2.9 percent in 2021, the slowest growth in the past 20 years, other than

2020, partly due to the slow pace of vaccination. An update to the Global

Economic Prospects is expected in January.

High Energy Prices Fueling Rise in

Other Commodity Costs

The picture of

commodity prices isn’t rosy either. According to the latest Commodity Markets

Outlook, energy prices are expected to average more than 80 percent higher in

2021 compared to the previous year.

Since energy

is a critical commodity for food production and heating, these soaring prices

can have downstream implications. Higher energy prices have already affected

fertilizer prices, in turn increasing the cost of food production. However, in

the latter half of 2021, food commodity prices have begun to stabilize in

response to favorable global supply outlook, but they are still above

pre-pandemic levels. Moreover, domestic food price inflation is rising in

most countries, reducing poor people’s ability to afford healthy food. This

can exacerbate food insecurity in developing countries. Unequal Vaccines Access

The quickest

way to end the pandemic is by vaccinating the world. However, with just over 7 percent of people in low-income

countries receiving a dose of the vaccines compared to over 75 percent in

high-income countries, we need fair and broad access to effective and safe

COVID-19 vaccines to save lives and strengthen global economic recovery. World Bank slashes global growth forecast and warns about

growing inequality PUBLISHED TUE, JAN 11

202211:42 PM EST, Saheli Roy Choudhury https://www.cnbc.com/2022/01/12/world-bank-slashes-2022-global-growth-forecast.html

(video as well) KEY POINTS ·

The World Bank

slashed its global growth forecast on Tuesday and cautioned that a rise in inflation, debt and income

inequality could jeopardize the recovery in emerging and developing

economies. ·

Global growth is

expected to slow to 4.1% in 2022 and

3.2% in 2023 as more nations start unwinding unprecedented levels of

fiscal and monetary policy support, the bank said in its latest “Global

Economic Prospects” report. ·

Growth in China is

set to ease to 5.1% this year, partly due to the lingering effects of the

pandemic as well as additional regulatory tightening from Beijing, according

to the report. The World Bank slashed its

global growth forecast for 2022 and 2023, and cautioned that a rise in

inflation, debt and income inequality could jeopardize the recovery in

emerging and developing economies. Global growth is expected to slow to 4.1% in 2022 and 3.2% in

2023 as more nations start unwinding unprecedented levels of fiscal and

monetary policy support to tackle the fallout from the coronavirus pandemic,

the bank said in its “Global Economic Prospects” report on Tuesday. The projections follow a

strong rebound in global growth as demand soared after Covid-related

lockdowns lifted. The World Bank estimated that the world economy grew 5.5%

in 2021. Major economies including the United States, China and countries

in the euro zone are expected to slow down this year,

the bank said. It added that a resurgence in Covid infections, due to the

highly contagious omicron variant, will likely disrupt economic activity in

the near term and could worsen growth projections if it persists. Ongoing supply-chain

bottlenecks, rising inflationary pressures and elevated levels of financial

vulnerability in large parts of the world could increase the risks of a “hard

landing,” the World Bank warned. A hard landing refers to a sharp economic

slowdown following a period of rapid growth. There’s a growing canyon

between [emerging economies’] growth rates and those in advanced economies. The World Bank is the

first major global institution this year to come out with growth projections.

The International Monetary Fund is expected to release its World Economic

Outlook update on Jan. 25, Reuters reported. Growth projections Growth in China is set to ease from an estimated 8% in 2021 to

5.1% this year, partly due to the lingering effects of the pandemic as well as

additional regulatory tightening from Beijing, according to the World Bank. Advanced economies are predicted to slow from 5% in 2021 to 3.8%

in 2022, which the World Bank said will be “sufficient to return

aggregate advanced-economy output to its prepandemic trend in 2023 and thus

complete its cyclical recovery.” On the other hand,

emerging markets and developing economies (EMDEs) are expected to “suffer

substantial scarring to output from the pandemic.” Their growth trajectories

would not be strong enough to return investment or output to pre-pandemic

levels by 2023, according to the report. Developing countries are

struggling with inflation and rising rates, says World Bank President Broadly, EMDEs are predicted to slow from an

estimated 6.3% last year to 4.6% in 2022. For some smaller nations or

even countries that rely heavily on tourism, the economic output is expected

to stay below pre-pandemic levels, the bank said. Worsening inequality The coronavirus pandemic has worsened income inequality,

particularly between countries, the World Bank said. It referred to data that

showed 60% of households surveyed in

EMDEs experienced a loss of income in 2020, while those in low-income

countries and in sub-Saharan Africa were hit the hardest. Inflation, which tends to

hit low-income workers the hardest, is running at levels not seen since 2008,

the bank said. Rising prices will constrain monetary policy where many

emerging and developing economies are withdrawing support to contain

inflation before the growth recovery is complete, it added. The pandemic also pushed

total global debt to the highest level in half a century and it could

complicate future coordinated debt relief efforts, the report said. The World

Bank called for “global cooperation” to help developing economies expand

their financial resources needed for sustainable development. Covid risks Covid-19 continues to cast

a shadow over growth prospects. If variants like omicron persist, it could

further reduce the bank’s global growth projections, according to World Bank

President David Malpass. “Developing countries are

facing severe long-term problems related to lower vaccination rates, global

macro policies and the debt burden,” he said in opening remarks during the

report’s launch. “There’s a growing canyon

between their growth rates and those in advanced economies. This inequality

is even more dramatic in per capita and median income terms, with people in

the developing world left behind and poverty rates rising,” he added. Moderna CEO: We can supply

up to 3 billion Covid vaccine booster doses this year “We’re seeing troubling

reversals in poverty, nutrition, and health.” Malpass also pointed out

that a reversal in education from school closures will have a permanent,

outsized impact on low and middle-income countries. Since early 2020, there

have been more than 300 million reported cases of Covid infections and over

5.5 million people have died. Vaccine rollout has been less than equitable,

with poorer countries struggling to get an adequate supply of doses. Information published by

Our World In Data showed that while 9.49 billion vaccine doses have so far

been administered worldwide, only 8.9% of people in low-income countries have

received at least one dose. Many international

institutions, including the World Bank as well as the World Health

Organization, have called for wider and more equitable distribution of

vaccines in order to bring the pandemic under control. Watch this video on

Netflix Death to 2020 https://www.youtube.com/watch?v=PZjLujzc858 |

|

IMF / World Economic Outlook October

2021 Forecast

https://mediacenter.imf.org/NEWS/imf---world-economic-outlook-october-2021-forecast/s/b81600f3-cb01-47c0-8751-7a10690341af

World

Economic Outlook, October 2021 (video)

The IMF is lowering its global growth

projection for 2021 slightly to 5.9 percent while keeping it unchanged for

2022 at 4.9 percent. However, this modest headline revision masks large

downgrades for some countries the Fund reports in its World Economic Outlook

released Tuesday (October 12) in Washington, DC. “The global recovery continues, but momentum

has weakened, hobbled by the pandemic. We have a slight downward revision for

global growth for this year to 5.9 percent for next year, our projection

remains unchanged at 4.9 percent. The divergences in growth prospects across

countries, however, persist and remains a major concern,” said Gita Gopinath,

Economic Counsellor and Director of the Research Department at the

International Monetary Fund Gopinath added that risks to economic

prospects have increased and policy trade-offs have become more complex in

the ongoing Covid-19 pandemic. Monetary policy will need to walk a fine line

between tackling inflation and financial risks and supporting the economic

recovery. “One of the major risks remains that there

could be new variants of the virus that could further slow back the recovery.

We're seeing major supply disruptions around the world that are also feeding

inflationary pressures, which are quite high and financial risk taking also is

increasing, which poses an additional risk to the outlook,” explained

Gopinath. The dangerous divergence in economic prospects

across countries remains a major concern. These divergences are a consequence

of the ‘great vaccine divide’ and large disparities in policy support. “The foremost priority is to vaccinate the

world. Much greater multilateral action is needed to vaccinate at least 40

percent of the population in every country by the end of this year and 70

percent by the middle of next year. We also need much greater action to

address climate change. Individual countries will need to tailor their fiscal

and monetary policy to the country's specific conditions, to the health

conditions in their country, to their economic conditions, while also maintaining

the credibility of their fiscal and monetary frameworks,” said Gopinath. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part II In class exercise – convert currencies

back and forth If the dollar is pegged to gold at US $1800 = 1

ounce of gold and the British pound is pegged to gold at £1200 = 1 ounce of

gold. What should be the exchange rate between US$ and British £? How much

can you make without any risk if the exchange rate is 1£ = 2$? Assume that

your initial investment is $1800. What about the exchange rate set

at 1£ = 1.2$? What about your initial investment is £1200? Solution: 1£ = 2$ (note

that the exchange rate is set at 1£ = 1.5$ since $1800 = £1500=1 ounce of

gold $1.5=1£). With $1800, you can buy 1 ounce of gold at US $1800

= 1 ounce of gold. With one ounce of gold, you can sell

it in UK at £1200 = 1 ounce of gold, so you can get back £1200 convert

£ to $ at $2=1£ as given get back £1200 * 2$/£ = $2400

> $1800, initial investment you

could make a profit of $600 ($2400 - $1800=$600) Yes. 1£ = 1.2$ (note

that the exchange rate is set at 1£ = 1.5$ since $1800 = £1500=1 ounce of

gold $1.5=1£). With

$1800, you can buy either 1 ounce of gold at US $1800 = 1 ounce of

gold. With

one ounce of gold, you can sell it in UK at £1200 = 1 ounce of gold, so you

can get back £1200 convert £ to $ at $1.2=1£ as

given get

back £1200 * 1.2$/£ = $1440 < $1800 you

will lose $360 ($1440 - $1800=$-360) No. So

should convert to £ first and then buy gold in UK With

$1800, you can convert to £1500 ($1800 / (1.2$/£ = £1500 ). buy

gold in UK at £1200 = 1 ounce of gold, so you can get back £1500/£1200 = 1.25

ounce of gold Sell gold in US

at US $1800 = 1 ounce of gold So

get back 1.25 ounce of gold * $1800 = $2250 > $1800 you

will make a profit of $450 ($2250 - $1800=$450) Yes. Homework chapter1-1 (due with first

midterm exam) 1. If

the dollar is pegged to gold at US $1800 = 1 ounce of gold and the British

pound is pegged to gold at €1500 = 1 ounce of gold. What should be the

exchange rate between US$ and Euro €? How much can you make without any risk

if the exchange rate is 1€ = 1.5$? (hint: $1800 è get gold è sell gold for euro è convert euro back to

$) How much can you make without any

risk if the exchange rate is 1€ = 0.8$? (hint: $1800 è get euro è buy gold using euro è sell gold for $) Assume

that your initial investment is $1800. (answer: $1.2/euro,

$450, $900) |

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part

III: Multilateral Trade vs. Bilateral Trade What is

MULTILATERALISM? What does MULTILATERALISM mean? MULTILATERALISM meaning

& explanation (youtube)

What is

BILATERAL TRADE? What does BILATERAL TRADE mean? BILATERAL TRADE meaning

& explanation (youtube)

Take

away: Multilateral

trade agreements strengthen the global economy by making developing countries

competitive. They

standardize import and export procedures giving economic benefits to all

member nations. Their

complexity helps those that can take advantage of globalization, while those

who cannot often face hardships. For

class discussion: Do you agree with the above points?

Why or why not? Multilateral Trade Agreements With Their Pros, Cons and

Examples

5 Pros and 4 Cons to the World's

Largest Trade Agreements https://www.thebalance.com/multilateral-trade-agreements-pros-cons-and-examples-3305949 BY REVIEWED BY Updated October 28, 2020 Multilateral trade

agreements are commerce treaties among three or more nations. The

agreements reduce tariffs and make

it easier for businesses to import and export. Since they are

among many countries, they are difficult to negotiate. That same broad scope makes them more

robust than other types of trade agreements once all

parties sign. Bilateral agreements are

easier to negotiate but these are only between two countries. They don't

have as big an impact on economic growth as does a multilateral

agreement. 5 Advantages of multilateral

agreements · Multilateral

agreements make all signatories treat each other equally. No country can

give better trade deals to one country than it does to another. That

levels the playing field. It's especially critical for emerging

market countries. Many of them are smaller in

size, making them less competitive. The Most

Favored Nation Status confers the

best trading terms a nation can get from a trading partner. Developing

countries benefit the most from this trading status. · The

second benefit is that it increases trade for every participant. Their

companies enjoy low tariffs. That makes their exports

cheaper. · The

third benefit is it standardizes commerce regulations for

all the trade partners. Companies save legal costs since they follow the same

rules for each country. · The

fourth benefit is that countries can negotiate trade deals with

more than one country at a time. Trade agreements undergo

a detailed approval process. Most countries would prefer to get one

agreement ratified covering many countries at once. · The

fifth benefit applies to emerging markets. Bilateral trade agreements

tend to favor the country with the best economy. That puts the weaker nation

at a disadvantage. But making emerging markets stronger helps the developed

economy over time. As those emerging markets become

developed, their middle class population increases. That creates

new affluent customers for everyone. 4 Disadvantages of multilateral

trading · The

biggest disadvantage of multilateral agreements is that they are

complex. That makes them difficult and time consuming to

negotiate. Sometimes the length of negotiation means it won't take place

at all. · Second,

the details of the negotiations are particular to trade and business practices.

The public often misunderstands them. As a result, they receive lots of

press, controversy, and protests. · The

third disadvantage is common to any trade agreement. Some companies and

regions of the country suffer when trade borders disappear. · The

fourth disadvantage falls on a country's small businesses. A

multilateral agreement gives a competitive advantage to giant

multi-nationals. They are already familiar with operating in a

global environment. As a result, the small firms can't compete. They lay off

workers to cut costs. Others move their factories to countries with a

lower standard of living. If a region depended on that industry, it

would experience high unemployment rates. That makes multilateral

agreements unpopular. Pros

Cons

Examples Some regional trade

agreements are multilateral. The largest had been the North American

Free Trade Agreement (NAFTA), which was ratified on

January 1, 1994. NAFTA quadrupled trade between the United

States, Canada, and Mexico from its 1993 level to

2018. On July 1, 2020, the U.S.-Mexico-Canada Agreement (USMCA) went

into effect. The USMCA was a new trade agreement between the three countries

that was negotiated under President Donald Trump. The Central American-Dominican

Republic Free Trade Agreement was signed on August 5, 2004. CAFTA-DR

eliminated tariffs on more than 80% of U.S. exports to six countries: Costa

Rica, the Dominican Republic, Guatemala, Honduras, Nicaragua, and El

Salvador. As of November 2019, it had increased trade by 104%, from

$2.44 billion in January 2005 to $4.97 billion. The Trans-Pacific

Partnership would have been bigger than NAFTA.

Negotiations concluded on October 4, 2015. After becoming

president, Donald Trump withdrew from the agreement. He promised to

replace it with bilateral agreements. The TPP was between

the United States and 11 other countries bordering the Pacific

Ocean. It would have removed tariffs and standardized business

practices. All global trade agreements

are multilateral. The most successful one is the General

Agreement on Trade and Tariffs. Twenty-three countries signed GATT in

1947. Its goal was to reduce tariffs and other trade barriers. In September 1986, the Uruguay

Round began in Punta del Este, Uruguay. It centered on extending

trade agreements to several new areas. These included services and

intellectual property. It also improved trade in agriculture and

textiles. The Uruguay Round led to the creation of the World Trade

Organization. On April 15, 1994, the 123 participating governments

signed the agreement creating the WTO in Marrakesh, Morocco. The

WTO assumed management of future global multilateral negotiations. The WTO's first project

was the Doha round of

trade agreements in 2001. That was a

multilateral trade agreement among all WTO members. Developing countries

would allow imports of financial services, particularly banking. In so

doing, they would have to modernize their markets. In return, the developed

countries would reduce farm subsidies. That would boost the growth

of developing countries that were good at producing food. Farm lobbies in the United States and

the European Union doomed

Doha negotiations. They refused to agree to lower subsidies or accept

increased foreign competition. The WTO abandoned the Doha round in July 2008. On December 7, 2013, WTO

representatives agreed to the so-called Bali package. All countries

agreed to streamline customs standards and reduce red tape to expedite

trade flows. Food security is an issue. India wants to subsidize food so

it could stockpile it to distribute in case of famine. Other countries worry

that India may dump the cheap food in the global market to gain market

share. Bilateral

Trade By JULIA KAGAN Updated December 21,

2020, Reviewed by TOBY WALTERS, Fact checked by ARIEL COURAGE https://www.investopedia.com/terms/b/bilateral-trade.asp What Is Bilateral Trade? Bilateral

trade is the exchange of goods between two nations promoting trade and

investment. The two countries will

reduce or eliminate tariffs, import quotas, export restraints, and other

trade barriers to encourage trade and investment. In the United States, the Office of

Bilateral Trade Affairs minimizes trade deficits through negotiating free

trade agreements with new countries, supporting and improving existing trade

agreements, promoting economic development abroad, and other actions. KEY TAKEAWAYS ·

Bilateral trade

agreements are agreements between countries to promote trade and commerce. ·

They eliminate trade

barriers such as tariffs, import quotas, and export restraints in order to

encourage trade and investment. ·

The main advantage

of bilateral trade agreements is an expansion of the market for a country's

goods through concerted negotiation between two countries. ·

Bilateral trade agreements can also result in the closing

down of smaller companies unable to compete with large multinational

corporations. Understanding Bilateral Trade The goals of bilateral trade

agreements are to expand access between two countries’ markets and increase

their economic growth. Standardized business operations in five general areas

prevent one country from stealing another’s innovative products, dumping

goods at a small cost, or using unfair subsidies. Bilateral

trade agreements standardize regulations, labor standards, and environmental

protections. The

United States has signed bilateral trade agreements with 20 countries,

some of which include Israel, Jordan, Australia, Chile, Singapore, Bahrain,

Morocco, Oman, Peru, Panama, and Colombia. The Dominican Republic-Central America

FTR (CAFTA-DR) is a free trade agreement signed between the United States and

smaller economies of Central America, as well as the Dominican Republic.

The Central American countries are El Salvador, Guatemala, Costa Rica,

Nicaragua, and Honduras. NAFTA replaced the bilateral agreements with Canada

and Mexico in 1994. The U.S. renegotiated NAFTA under the United

States-Mexico-Canada Agreement, which went into effect in 2020.2 Advantages and Disadvantages of

Bilateral Trade Compared to multilateral trade

agreements, bilateral trade agreements

are negotiated more easily, because only two nations are party to the

agreement. Bilateral trade agreements initiate and reap trade benefits faster

than multilateral agreements. When negotiations for a multilateral

trade agreement are unsuccessful, many nations will negotiate bilateral

treaties instead. However, new agreements often result in competing

agreements between other countries, eliminating the advantages the Free Trade

Agreement (FTA) confers between the original two nations. Bilateral trade agreements also expand

the market for a country's goods. The United States vigorously pursued free

trade agreements with a number of countries under the Bush administration

during the early 2000s. In addition to creating a market for

U.S. goods, the expansion helped spread the mantra of trade liberalization

and encouraged open borders for trade. However, bilateral trade agreements can skew a country's markets when large

multinational corporations, which have significant capital and resources to

operate at scale, enter a market dominated by smaller players. As a

result, the latter might need to close shop when they are competed out of

existence. Examples of Bilateral Trade In October 2014, the United States and

Brazil settled a longstanding cotton dispute in the World Trade Organization

(WTO). Brazil terminated the

case, relinquishing its rights to countermeasures against U.S. trade or

further proceedings in the dispute. Brazil also agreed to not bring new

WTO actions against U.S. cotton support programs while the current U.S. Farm

Bill was in force, or against agricultural export credit guarantees under the

GSM-102 program. Because of the agreement, American businesses were no longer

subject to countermeasures such as increased tariffs totaling hundreds of

millions of dollars annually. In March 2016, the U.S. government and

the government of Peru reached an agreement removing barriers for U.S. beef

exports to Peru that had been in effect since 2003. The agreement opened one of the

fastest-growing markets in Latin America. In 2015, the United States exported

$25.4 million in beef and beef products to Peru. Removal of Peru’s

certification requirements, known as the export verification program, assured

American ranchers expanded market access. The agreement reflected the U.S.

negligible risk classification for bovine spongiform encephalopathy (BSE) by

the World Organization for Animal Health (OIE). The United States and Peru agreed to

amendments in certification statements making beef and beef products from

federally inspected U.S. establishments eligible for export to Peru, rather

than just beef and beef products from establishments participating in the

USDA Agricultural Marketing Service (AMS) Export Verification (EV) programs

under previous certification requirements. Homework chapter1-2 (due with first

midterm exam) 1)

Do you support

bilateral trading or multi-lateral trading? Why? 2)

What is your opinion

about RCEP? Do you think that the member countries can benefit from RCEP? Why

or why not? |

|

What is the

RCEP? | CNBC Explains (youtube)

China and 14

partners sign world's biggest trade deal without US | DW News (video)

RCEP Trade Deal: Significance of Massive Asia

Pacific Pact Sometimes who is not at the party matters as

much as who is By JAMES CHEN Published November 25, 2020 https://www.investopedia.com/rcep-trade-deal-significance-of-massive-asia-pacific-pact-5088935 Trade deals are

economically significant and have a real impact when companies use them to

access previously limited markets, but they are a political creation with

economic implications that are not usually seen immediately after

implementation. The Regional Comprehensive Economic Partnership (RCEP) is no

different in that it will take years to know which countries and companies

have benefited most from this political deal. What is important to

investors to note, however, is that RCEP is now the second major trade

deal focusing on Asia being signed without the United States. In this

article, we'll look at RCEP, why it matters, and what it may be signaling for

the future of global trade. KEY TAKEAWAYS · RCEP is the second major trade deal in Asia to take place without any

U.S. involvement. · China is seen as the crown jewel of the RCEP and is the largest economy

among the signatories. · The RCEP agreement is not as comprehensive as the Comprehensive and

Progressive Agreement for Trans-Pacific Partnership (CPTPP) in harmonizing

economic philosophies on issues like labor and environment. Overview of RCEP The RCEP comprises

15 countries, including seven that were part of the CPTPP. The countries that

signed the deal on Nov. 15 are: Australia (CPTPP

member) Brunei (CPTPP

member) Cambodia China Indonesia Japan (CPTPP member) Laos Malaysia (CPTPP

member) Myanmar New Zealand (CPTPP

member) Philippines Singapore (CPTPP

member) South Korea Thailand Vietnam (CPTPP

member) India was

initially part of the RCEP but has since pulled out. It should be noted that the

door is open for the country to join later. The deal covers roughly one-third

of the world's population and just under one-third of global GDP. The

Brookings Institute estimates that the deal will increase global GDP by $500

billion in the next 10 years, but estimates vary widely as with all trade

deals. Most agree that the RCEP has the potential to add well over $100

billion to national incomes within the trading block. What Makes RCEP

Different Despite having seven

CPTPP members as part of the RCEP, the RCEP is a different type of trade

deal. The CPTPP went a long way to harmonize key points such as intellectual

property, environment, labor, and rules around state-owned enterprises. All

these areas in the CPTPP required higher standards among many signatories in

order to enjoy freer trade with other members. The RCEP is silent on almost

all of these points, which has been spun as a direct influence of having

China involved as the largest, and arguably key, economy. Even if this is a

sign of China's influence, the biggest win for members of the RCEP is

having reduced tariffs on products that are sourced within the trading

block. This means, for example, that a Japanese-designed car pulling in parts

from South Korea and assembled in China can be sold in Australia without

triggering tariffs based on third-country content. This sets up an incentive

for the RCEP members to source more freely within their region, which should

result in them trading more freely in general. The Layers of Trade

Agreements in Asia Pacific The world of

bilateral and multilateral trade agreements requires more than a few

whiteboards to map out. The RCEP is China's first multilateral agreement, but

the country has a number of bilateral trade agreements, including with

Australia – a country that, along with New Zealand, has a deal with every

other country in the RCEP. In these cases, the

countries with more developed bilateral agreements generally keep the deeper

trade ties but respect the new unified sourcing rules under the RCEP. In this

sense, the RCEP still removes a country-of-origin headache from regionally

sourced supply chains. Leadership May be

Shifting East The CPTPP and RCEP

are both deals that, judging solely on membership location, tilt toward Asia.

Most importantly, these do not involve the United States. The United States

has signed the United-States-Mexico-Canada Agreement (USMCA) that replaced

NAFTA recently, but the last free trade agreement other than that was signed

with Panama in 2007. The United States' 14 free trade

agreements encompass 20 countries, but only three of these countries are also

members of RCEP. The exit of the United States from the CPTPP

represented a pull back for a country that once was a global champion of free

trade. The inclusion of China in RCEP and the absence of the United States

suggests that the Asia Pacific region is moving ahead on its own. The deals may be

less comprehensive, but they are still getting done. The Bottom Line RCEP members will benefit from lower tariffs

on products sourced and traded in the region, making the ties between these

countries deeper. The larger economies like China, Japan, South Korea, and

Australia will likely benefit the most at first, but the whole region will

see more income over time in the form of regional sourcing. The most important

takeaway, however, is that the United States may be losing its global

leadership on trade to nations within the Asia Pacific region. Of course,

this situation can be reversed – the door is still open for the United States

on the CPTPP, for example – and the hopes are high that an incoming Biden

administration will do just that. Whether that reversal takes place or not is

another loaded question facing the global economy in 2021. Rust Belt https://www.investopedia.com/terms/r/rust-belt.asp (FYI) By JAMES CHEN Updated Aug 25, 2020 What Is the Rust Belt? The Rust Belt is a colloquial term used to

describe the geographic region stretching from New York through the Midwest

that was once dominated by the coal industry, steel production,

and manufacturing. The Rust Belt became an industrial hub due to its proximity to

the Great Lakes, canals, and rivers, which allowed companies to

access raw materials and ship out finished products. The region received the name Rust Belt in the

late 1970s, after a sharp decline in industrial work left many

factories abandoned and desolate, causing increased rust from exposure to the

elements. It is also referred to as the Manufacturing Belt and the

Factory Belt. KEY TAKEAWAYS

Understanding the Rust Belt The term Rust Belt is often used in a derogatory sense to

describe parts of the country that have seen an economic decline—typically

very drastic. The rust belt region

represents the deindustrialization of an area, which is often accompanied

by fewer high-paying jobs and high poverty rates. The result has been a

change in the urban landscape as the local population has moved to other

areas of the country in search of work. Although there is no definitive boundary, the states that are

considered in the Rust Belt–at least partly–include the following:

There are other states in the U.S. that have also experienced

declines in manufacturing, such as states in the deep south, but they are not

usually considered part of the Rust Belt. The region was home to some of

America's most prominent industries, such as steel production

and automobile manufacturing. Once recognized as the industrial

heartland, the region has experienced a sharp downturn in industrial activity

from the increased cost of domestic labor, competition from overseas,

technology advancements replacing workers, and the capital

intensive nature of manufacturing. Poverty in the Rust Belt Blue-collar jobs have increasingly moved

overseas, forcing local governments to rethink the type of manufacturing

businesses that can succeed in the area. While some cities managed to adopt new technologies, others

still struggle with rising poverty levels and declining populations. Below are the poverty rates from the U.S. Census

Bureau as of 2018 for each of the Rust Belt states listed above. Poverty Rates in the Rust Belt. There are other U.S. states that have high poverty rates, such

as Kentucky (16.9%), Louisiana (18.6%), and Alabama (16.8%). However, the

rust belt states have–at a minimum–a double-digit percentage of their

population in poverty.1 History of the Rust Belt Before being known as the Rust Belt, the area was generally

known as the country's Factory, Steel, or Manufacturing Belt. This area, once

a booming hub of economic activity, represented a great portion of U.S.

industrial growth and development. The natural resources that were found in the area led to its

prosperity—namely coal and iron ore—along with labor and ready access to

transport by available waterways. This led to the rise in coal and steel

plants, which later spawned the weapons, automotive, and auto parts

industries. People seeking employment began moving to the area, which was

dominated by both the coal and steel industries, changing the overall

landscape of the region. But that began to change between the 1950s and 1970s. Many

manufacturers were still using expensive and outdated equipment and

machinery and were saddled with the high costs of domestic labor and

materials. To compensate, a good portion of them began looking elsewhere for

cheaper steel and labor—namely from foreign sources—which would ultimately

lead to the collapse of the region. There is no definitive boundary for the Rust

Belt, but it generally includes the area from New York through the Midwest. Decline of the Rust Belt Most research suggests the Rust Belt started to falter in the

late 1970s, but the decline may have started earlier, notably in the 1950s,

when the region's dominant industries faced minimal competition.

Powerful labor unions in the automotive and steel manufacturing

sectors ensured labor competition stayed to a minimum. As a result, many of

the established companies had very little incentive to innovate or expand

productivity. This came back to haunt the region when the United States

opened trade overseas and shifted manufacturing production to the south. By the 1980s, the Rust Belt faced competitive

pressure—domestically and overseas—and had to ratchet down wages and prices. Operating in

a monopolistic fashion for an extended period of time played an

instrumental role in the downfall of the Rust Belt. This shows that

competitive pressure in productivity and labor markets are important to

incentivize firms to innovate. However, when those incentives are weak,

it can drive resources to more prosperous regions of the country. The region's population also showed a rapid

decline. What was once a hub

for immigrants from the rest of the country and abroad, led to an exodus of

people out of the area. Thousands of

well-paying blue-collar jobs were eliminated, forcing people to move away in

search of employment and better living conditions. Politics and the Rust Belt The term Rust Belt is generally attributed to Walter Mondale,

who referred to this part of the country when he was the Democratic

presidential candidate in 1984. Attacking President Ronald Reagan, Mondale

claimed his opponent's policies were ruining what he called the Rust

Bowl. He was misquoted by the media as saying the rust belt, and the term

stuck. Since then, the term has consistently been used to describe the area's

economic decline. From a policy perspective, addressing the specific needs of the

Rust Belt states was a political imperative for both parties during the 2016

election. Many believe the national

government can find a solution to help this failing region succeed again. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 2 Let’s watch this video together. Imports, Exports,

and Exchange Rates: Crash Course Economics #15 Topic

1- What is BOP? The balance of payment of a country contains two

accounts: current and capital. The current account records exports and imports of goods and services

as well as unilateral transfers, whereas the capital account records purchase and sale transactions of foreign

assets and liabilities during a particular year. What

is the current account? Balance

of payments: Current account (video, Khan academy)

From

khan academy

Current vs. Capital Accounts: What's the

Difference? By

THE INVESTOPEDIA TEAM, Updated June

29, 2021, Reviewed by ROBERT C. KELLY Current

vs. Capital Accounts: An Overview The

current and capital accounts represent two halves of a nation's balance of

payments. The current account

represents a country's net income over a period of time, while the capital

account records the net change of assets and liabilities during a particular

year. In

economic terms, the current account deals with the receipt and payment in

cash as well as non-capital items, while the capital account reflects sources

and utilization of capital. The sum of

the current account and capital account reflected in the balance of payments

will always be zero. Any surplus or deficit in the current account is matched

and canceled out by an equal surplus or deficit in the capital account. KEY

TAKEAWAYS ·

The current and

capital accounts are two components of a nation's balance of payments. ·

The current account

is the difference between a country's savings and investments. ·

A country's capital

account records the net change of assets and liabilities during a certain

period of time. Current Account The

current account deals with a country's short-term transactions or the

difference between its savings and investments. These are also referred to as

actual transactions (as they have a real impact on income), output and

employment levels through the movement of goods and services in the economy. The current account consists of visible trade

(export and import of goods), invisible trade (export and import of services),

unilateral transfers, and investment income (income from factors such as land

or foreign shares). The credit and debit of foreign exchange from these

transactions are also recorded in the balance of the current account. The

resulting balance of the current account is approximated as the sum total of

the balance of trade. Current Account vs. Capital Account Transactions

are recorded in the current account in the following ways: Exports are noted as credits in the balance

of payments Imports are recorded as debits in the

balance of payments The

current account gives economists and other analysts an idea of how the country

is faring economically. The difference

between exports and imports, or the trade balance, will determine whether a

country's current balance is positive or negative. When it is positive, the

current account has a surplus, making the country a "net lender" to

the rest of the world. A deficit means the current account balance is

negative. In this case, that country is considered a net borrower. If

imports decline and exports increase to stronger economies during a

recession, the country's current account deficit drops. But if exports

stagnate as imports grow when the economy grows, the current account deficit

grows. Capital Account The capital account is a record of the

inflows and outflows of capital that directly affect a nation’s foreign

assets and liabilities. It is concerned

with all international trade transactions between citizens of one country and

those in other countries. The

components of the capital account include foreign investment and loans,

banking, and other forms of capital, as well as monetary movements or changes

in the foreign exchange reserve. The capital account flow reflects factors

such as commercial borrowings, banking, investments, loans, and capital. A surplus in the capital account means

there is an inflow of money into the country, while a deficit indicates money

moving out of the country. In this case,

the country may be increasing its foreign holdings. In

other words, the capital account is concerned with payments of debts and

claims, regardless of the time period. The balance of the capital account

also includes all items reflecting changes in stocks. The

International Monetary Fund divides capital account into two categories: The

financial account and the capital account. The term capital account is also used in accounting. It

is a general ledger account used to record the contributed capital of

corporate owners as well as their retained earnings. These balances are

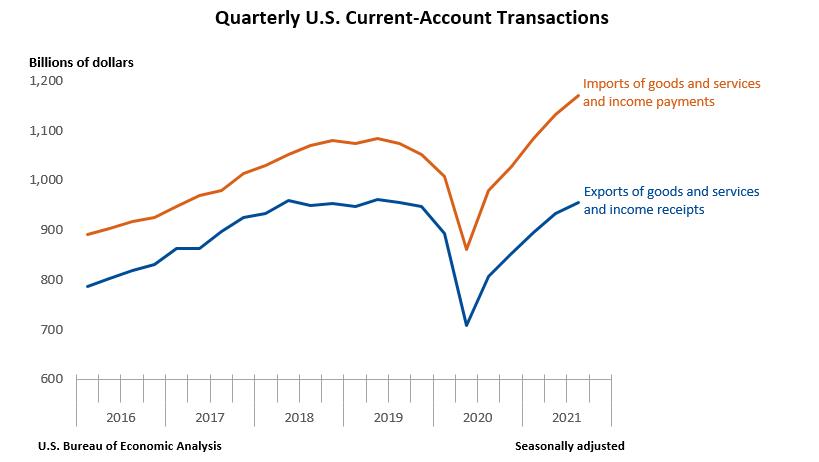

reported in a balance sheet's shareholder's equity section. https://www.bea.gov/data/intl-trade-investment/international-transactions U.S. Current-Account Deficit Widens in Third

Quarter 2021 https://www.bea.gov/news/blog/2021-12-20/us-current-account-deficit-widens-third-quarter-2021#:~:text=The%20U.S.%20current%2Daccount%20deficit,the%20third%20quarter%20of%202021 December 20,

2021 The U.S. current-account deficit, which reflects

the combined balances on trade in goods and services and income flows between

U.S. residents and residents of other countries, widened by $16.5 billion, or

8.3 percent, to $214.8 billion in the third quarter of 2021. The widening

reflected a reduced surplus on services and expanded deficits on secondary

income and on goods that were partly offset by an expanded surplus on primary

income. The

third-quarter deficit was 3.7 percent of current-dollar gross domestic

product, up from 3.5 percent in the second quarter.

COVID-19 Impact on Third-Quarter 2021 International

Transactions (FYI) https://www.bea.gov/news/2021/us-international-transactions-third-quarter-2021 Current-Account Transactions Exports of goods and services to, and income

received from, foreign residents increased $22.8 billion to $955.9 billion in

the third quarter. Imports of goods and services from, and income paid to,

foreign residents increased $39.3 billion to $1.17 trillion.

Trade in goods Exports of goods increased $4.8 billion to

$441.6 billion, mainly reflecting increases in industrial supplies and

materials, mostly natural gas and petroleum and products, and in consumer

goods, mostly medicinal, dental, and pharmaceutical products. A decrease in

foods, feeds, and beverages, mostly corn and soybeans, partly offset these

increases. Imports of goods increased $10.0 billion to $716.4 billion,

primarily reflecting an increase in industrial supplies and materials, mostly

petroleum and products and chemicals. Trade in services Exports of services decreased $0.1 billion

to $190.8 billion, primarily reflecting decreases in charges for the use of

intellectual property, mostly licenses for the use of outcomes of research

and development (such as patents and trade secrets), and in

telecommunications, computer, and information services, mostly computer

services. An increase in other business services, mostly professional and

management consulting services, partly offset these decreases. Imports of

services increased $12.6 billion to $141.0 billion, mostly reflecting

increases in travel, primarily other personal travel, and in transport,

primarily sea freight and air passenger transport. Primary income Receipts of primary income increased $17.9

billion to $281.9 billion, mainly reflecting increases in direct investment

income, primarily earnings, and in portfolio investment income, mostly equity

securities. Payments of primary income increased $8.6 billion to $233.7

billion, primarily reflecting an increase in portfolio investment income,

mostly interest on long-term debt securities. Secondary income Receipts of secondary income increased $0.1

billion to $41.6 billion, reflecting an increase in general government

transfers, mainly taxes on income and wealth. Payments of secondary income

increased $8.0 billion to $79.6 billion, mainly reflecting an increase in

general government transfers, mostly international cooperation. Capital-Account Transactions Capital-transfer receipts were $3.8 billion

in the third quarter. The transactions reflected receipts from foreign

insurance companies for losses resulting from Hurricane Ida Financial-Account Transactions Net financial-account transactions were

–$127.2 billion in the third quarter, reflecting net U.S. borrowing from

foreign residents. Financial assets Third-quarter transactions increased U.S. residents’

foreign financial assets by $494.1 billion. Transactions increased portfolio

investment assets, mainly debt securities, by $311.7 billion; reserve assets,

primarily special drawing rights (SDRs), by $112.6 billion; and direct

investment assets, mostly equity, by $98.2 billion. Transactions decreased

other investment assets, mostly deposits, by $28.5 billion. The increase in

SDRs reflects the U.S. share of the $650 billion SDR allocation approved by

the Board of Governors of the International Monetary Fund (IMF). The SDR is

an international reserve asset created by the IMF to supplement its member

countries’ official reserves; it can be exchanged between members for

currencies, such as the U.S. dollar, the euro, or the yen. The allocation in

the third quarter was the largest in the history of the IMF. Liabilities Third-quarter transactions increased U.S.

liabilities to foreign residents by $613.3 billion. Transactions increased

other investment liabilities, mostly deposits and SDR allocations, by $318.0

billion; direct investment liabilities, mostly equity, by $149.1 billion; and

portfolio investment liabilities, primarily equity, by $146.2 billion. The

SDR allocation liability represents the long-term obligation of each IMF

member country holding SDRs to all other members. In an SDR allocation, the

incurrence of U.S. liabilities offsets the acquisition of U.S. assets so the

SDR allocation has no impact on the net financial-account transactions.

What is the Capital Account

Balance of

payments: Capital account (video, Khan Academy) https://fred.stlouisfed.org/tags/series?t=capital+account Top Trading Partners - November 2021 https://www.census.gov/foreign-trade/statistics/highlights/toppartners.html

Year-to-Date Surpluses

Year-to-Date Deficit

Topic 2: Trade war with China to

reduce trade deficit (current account deficit) For Class Discussion: Has the US won the trade war against

China? Can trade war help reduce the US current account deficit? America v China: why the trade war won't end soon | The Economist (youtube)

Has the US lost the trade war with China? (youtube)

US-China trade deficit skyrockets | DW News (youtube)

2021

: U.S. trade in goods with China

NOTE:

All figures are in millions of U.S. dollars on a nominal basis. https://www.census.gov/foreign-trade/balance/c5700.html

U.S. tariffs on

Chinese goods didn’t bring companies back to the U.S., new research finds These tariffs instead resulted in collateral damage to the

U.S. economy By Jiakun Jack Zhang and Samantha A. Vortherms, September

22, 2021 at 5:00 a.m. EDT Treasury Secretary Janet L. Yellen recently argued that tariffs from the U.S.-China trade war —

covering more than $307 billion worth of goods — “hurt American consumers,”

yet the negotiations “really didn’t address in many ways the fundamental

problems we have with China.” U.S. tariffs on

Chinese exports jumped sixfold between 2018 and 2020, but tariffs failed to decouple the two economies. As the Biden

administration conducts its comprehensive review of China trade policy and

contemplates new tariffs, our research helps explain whether existing tariffs

achieved their policy objective. Tariffs increase the

cost of doing business overseas by making those goods more expensive to

import. The Trump administration’s logic was that tariffs would hurt U.S. and

other multinational corporations engaged in U.S.-China trade — and push more

companies to divest from China and shift supply chains to the United States. Tariff proponents

argued the Chinese economy would suffer, giving U.S. negotiators more

leverage over China at the negotiating table. Fear of ‘terrorism’ shaped U.S. foreign policy after 9/11.

Will the U.S. make China the next big obsession? In fact, these

tariffs resulted in collateral damage to the U.S. economy without pressuring

China to change its economic policies. Here’s why. The U.S. hoped to see

multinationals walk away from China. In a recent working paper, we built a new data set on foreign-invested

enterprises registered in China to identify multinationals that choose to

divest each year. We found that new

U.S. tariffs in 2018 and 2019 had a minimal effect on divestment. More

than 1,800 U.S.-funded subsidiaries closed in the first year of the trade

war, a 46 percent increase over the previous year. U.S. company exits

immediately after the onset of the trade war were not concentrated in

manufacturing or information technology, two sectors most directly affected

by the trade war. We estimate that

less than 1 percent of the increase in U.S. firm exits during this period was

due to U.S. tariffs. And U.S. firms were no more likely to divest than

firms from Europe or Asia. Instead, company exits were driven more by the

company’s capacity to mitigate political risk. Larger and older multinational were significantly less likely to exit

China after the onset of the trade war. These findings may surprise politicians, but are fully in

line with recent research explaining how tariffs pass through to U.S.

consumers. Rather than leaving China

or finding alternative suppliers, U.S. firms simply raised prices for their

customers. Survey data show large

U.S. businesses remain optimistic about the Chinese market and plan to

increase their investments there. Most of these firms are already “In

China, for China” — those that are exposed to tariffs are taking advantage of

workarounds such as the first sale rule or passing on costs to suppliers. Tariffs provided little leverage — for either country If U.S. multinationals aren’t rushing to exit China, are

they pressuring the U.S. government for tariff relief, as the Chinese

government hoped? Many analysts believed the U.S. business community would

push back, and stop the trade war from escalating. We investigated the

political behavior of a sample of 500 large U.S. multinationals with

subsidiaries in China to see if they engaged in political activities such as

commenting, testifying or lobbying in opposition to the U.S. Section 301

tariffs. We found that most U.S. companies adopted an apolitical

strategy. They didn’t exit China, but

also didn’t put public pressure on Washington to roll back the tariffs.

Even though 63 percent of U.S. multinationals in our sample were adversely

impacted by the trade war, only 22 percent chose to voice opposition and 7

percent chose to exit China. The majority (65 percent) did neither. The U.S. and China finally signed a trade agreement. Who

won? Many of the

multinationals we coded as “voicing opposition” did so through associations

such as the US-China Business Council rather than under their own name. An even larger number unsuccessfully lobbied for tariff

exclusion for specific products, rather than a more general rollback of

Section 301 tariffs. Smaller businesses saw greater collateral damage Our findings suggest

that U.S. companies aren’t divesting from China as much as U.S. policymakers

would like — or pushing back against tariffs as much as Chinese policymakers

had hoped. Instead, large

companies responded to the increased cost of business by passing the cost of

tariffs on to their customers. And individual consumers in the United States

paid higher prices for imports from China. Smaller companies and

those newer to China were more likely to exit. Firms with older and larger

subsidiaries in China face higher sunk costs from leaving China altogether,

which makes them more likely to continue China operations. This finding parallels reports about small businesses in

the United States who were unable to find alternative suppliers or afford

expensive lobbyists during the trade war. The higher tariffs on raw materials imported from China made it

tougher for some small businesses, particularly if they lacked the leverage

to pass these costs on to customers or the resources to mitigate them. Would other trade tools work? Despite intensifying political hostility between Beijing

and Washington and the mounting economic cost of tariffs, Chinese and U.S.

businesses remain deeply integrated in terms of financial, knowledge and

production networks. And despite the trade war, foreign investment inflows

into China grew by 4.5 percent from 2019 — and hit a record $144.37 billion

in 2020. There‘s little sign that U.S. multinationals have embraced the idea

of decoupling from China. While U.S. Trade

Representative Katherine Tai justified the Biden administration’s hesitancy

to remove tariffs on the grounds that tariffs provide leverage against China,

our research demonstrates that U.S. tariffs haven’t produced the intended

results. Instead, multinationals continue to navigate the uncertain

U.S.-China relationship and related political risks. Smaller firms, in

particular, may find it difficult to absorb the costs generated by the trade

war. The lack of U.S. leverage resulting from the trade war may

dispel the notion that tariffs are “tough on China” and may help focus the

policy debate on the harm to U.S. consumers from tariffs that remain in

place. The Biden administration has at its disposal an array of alternative

tools besides tariffs for economic competition with China that may result in

less collateral damage on the U.S. economy. After all, economic coercion can be a double-edged sword:

These tools tend to inflict collateral damage on one’s economy while hurting

that of the target, but tariffs are the bluntest tool of all. Chapter 2

(Due with first mid term exam) 1.

Based on the classroom discussion, and documents posted and

available online, do you think that the trade war against China could help US

to reduce its trade deficit (or current account deficit)? Please be specific. 2.

What is your opinion about the increasing current account

deficit during Covid 19 pandemic? Is the current account deficit a problem?

Why or why not? For reference, please

visit https://www.imf.org/external/pubs/ft/fandd/basics/current.htm 3. Internet

exercises (not required, information for intereted students only) a. IMF,

world bank and UN are only a few of the major organizations that

track, report and aid international economic and financial

development. Based on information provided in those websites, you could learn

about a country’s economic outlook. IMF: www.imf.org/external/index.htm UN: www.un.org/databases/index.htm World

bank: www.worldbank.org’ Bank

of international settlement: www.bis.org/index.htm b. St. Louis

Federal Reserve provides a large amount of recent open economy macroeconomic

data online. You can track down BOP and GDP data for the major industrial

countries. Recent

international economic data: research.stlouisfed.org/publications Balance of Payments

statistics: research.stlouisfed.org/fred2/categories/125 |

|

Balance

of payments: Current account (video, Khan academy) (FYI)

Balance of payments:

Capital account (video, Khan Academy) (FYI) Current vs.

capital accounts: what is the difference (youtube)? Reference

of useful websites for global economy International Trade

Statistics (PDF) Current

Account (BOP) Data – World Bank http://data.worldbank.org/indicator/BN.CAB.XOKA.CD IMF,

world bank and UN are only a few of the major organizations that track, report and aid

international economic and financial development.

Using these website, you can summarize the economic outlook for

each country. IMF: www.imf.org/external/index.htm UN: www.un.org/databases/index.htm World

bank: www.worldbank.org Bank

of international settlement: www.bis.org/index.htm St.

Louis Federal Reserve provides a large amount of recent open economy

macroeconomic data online. You can track down BOP and GDP data for the major

industrial countries. Recent international

economic data: research.stlouisfed.org/publicaitons/ie Rolling back U.S.-China tariffs would ease

inflation in the U.S., former Treasury secretary says PUBLISHED TUE, NOV 30

2021, Weizhen Tan https://www.cnbc.com/2021/11/30/removing-us-china-trade-tariffs-would-ease-inflation-jacob-lew.html KEY POINTS ·

Eliminating tariffs imposed on goods during

the worst of the trade war would help ease inflation in the U.S., former

Treasury Secretary Jacob Lew told CNBC. ·

But there’s currently “no political space”

to do so, he said on CNBC’s “Street Signs Asia.” ·

Worries over inflation have shot up this

year, as energy prices spiked and the ongoing supply chain crisis led to

shortages of goods. But Lew said there’s been “a bit of excess nervousness

about inflation.” U.S. fiscal stimulus

package is unlikely despite omicron: Ex-Treasury Secretary Eliminating tariffs

imposed on goods during the worst of the trade war would help ease inflation

in the U.S., former Treasury Secretary Jacob Lew told CNBC on Tuesday. But there’s currently

“no political space” to do so, he said on CNBC’s “Street Signs Asia.” “I think that the

United States and China have deep differences. I’ve never thought it should

just be about negotiating the exchange of one good or another on one side or

the other. It should be about a level playing field,” Lew said. He served as

treasury secretary from 2013 to 2017 during the Obama administration. He continued: “I’ve thought

from the beginning that the tariffs were an ineffective way to deal with

their attacks on American consumers. And right now, with inflation being an

issue, rolling back tariffs would actually reduce inflation in the United

States.” Relations between

Washington and Beijing took a turn for the worse in 2018, when the Trump

administration imposed tariffs on billions of dollars worth of Chinese goods

and Beijing retaliated with similar punitive measures, drawing both sides

into a protracted trade war. U.S. tariffs on Chinese goods stood at an average

of 19.3% on a trade-weighted basis in early 2021, while Chinese tariffs on

American products were at about 20.7%, according to data compiled by think tank

Peterson Institute for International Economics earlier this year. Before the trade war, U.S. tariffs on Chinese

goods were on average 3.1% in early 2018 while China’s tariffs on American

goods were at 8%, the data

showed. Referring to rolling

back tariffs, Lew said: “Both the leaders have to, I think, create political

space in our two countries for these issues to be issues where you can move

and make progress, because otherwise we either stay where we are. It gets

worse. I think we can do better.” American businesses are bearing most of the cost

burden from the elevated tariffs imposed at the height of the U.S.-China

trade war, according

to a report from Moody’s Investors Service earlier this year. The ratings agency said

that U.S. importers absorbed more than 90% of additional costs resulting

from the 20% U.S. tariff on Chinese goods. That means U.S. importers pay

around 18.5% more in price for a Chinese product subject to that 20% tariff

rate, while Chinese exporters receive 1.5% less for the same product,

according to the report. ‘Excess nervousness’

about inflation Worries over inflation

have shot up this year, as energy prices spiked and the ongoing supply chain

crisis led to shortages of goods. The U.S. consumer price

index, which tracks a basket of products ranging from gasoline and health

care to groceries and rent, rose 6.2% in October from a year ago, the highest

in 30 years. But Lew told CNBC it’s

likely “much of the inflation that we’re seeing will work its way through.” “I don’t think anyone

is predicting hyperinflation,” he said. “But I think there’s been a bit of

excess nervousness about inflation. And candidly, the public reaction to

inflation is very strong.” But Lew warned that

policymakers have to walk a fine line and ensure that measures used to combat

inflation don’t slow the economy down so much that they dampen growth. — CNBC’s Yen Nee Lee,

Jeff Cox contributed to this report. Khan Academy’s

view of the trade deficit with China (video) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

In class exercise: 1.

If U.S. imports > exports, then the supply of

dollars > the demand of the dollars in the foreign exchange market, ceteris

paribus. True/False? Solution: Import

means using $ (spending $, or out flow of $) to buy foreign goods In

the FX market, supply of $ increases So

when supply increases and assume that demand is unchanged, the

value of $ will drop 2. If Japan exports

> imports, then yen would appreciate against other

currencies. True/False? Solution: Export

means selling domestic products for yen ( in flow of yen from importers who

will pay yen for the goods made in Japan; there is an increased demand for

yen) In

the FX market, demand of yen increases So

when demand increases and assume that supply is unchanged, the

value of yen will rise. 3. If the interest rate

rises in the U.S., ceteris paribus, then capital will flow out of

the U.S. True/False? Solution: Interest

rate rises financial market will become

more attractive to foreign investors capital

will flow in, not out of the U.S. |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part II of Chapter 2 --- Evolution

of international monetary system Finance: The History of Money (combined) (video,

fan to watch)

Review of history of money: A brief

history of money - From gold to bitcoin and cryptocurrencies (video)

· Bimetallism:

Before 1875 · Classical

Gold Standard: 1875-1914 The Gold Standard Explained in One

Minute (video)

§ International

value of currency was determined by its fixed relationship to gold. § Gold

was used to settle international accounts, so the risk of trading with other

countries could be reduced. · Interwar

Period: 1915-1944 § Countries

suspended gold standard during the WWI, to increase money supply and pay for

the war. § Countries

relied on a partial gold standard and partly other countries’ currencies during the WWII · Bretton Woods System: 1945-1972 The Bretton Woods Monetary

System (1944 - 1971) Explained in One Minute (video)

§ All

currencies were pegged to US$. § US$ was

the only currency that was backed by gold. § US$ was

world currency at that time. · The

Flexible Exchange Rate Regime: 1973-Present FLOATING AND FIXED EXCHANGE RATE (video)

For class discussion: Read

the following. Is there any knowledge that is new to you? Bretton Woods Agreement and System By

JAMES CHEN Updated April 28, 2021, Reviewed by SOMER ANDERSON What

Was the Bretton Woods Agreement and System? The Bretton Woods Agreement was

negotiated in July 1944 by delegates from 44 countries

at the United Nations Monetary and Financial Conference held in Bretton

Woods, New Hampshire. Thus, the name “Bretton Woods Agreement.” Under

the Bretton Woods System, gold was the

basis for the U.S. dollar and other currencies were pegged to the U.S.

dollar’s value. The Bretton Woods

System effectively came to an end in the early 1970s when President Richard

M. Nixon announced that the U.S. would no longer exchange gold for U.S.

currency. The

Bretton Woods Agreement and System Explained Approximately

730 delegates representing 44 countries met in Bretton Woods in July 1944 with the principal goals of creating an

efficient foreign exchange system, preventing competitive devaluations of

currencies, and promoting international economic growth. The Bretton Woods

Agreement and System were central to these goals. The Bretton Woods Agreement

also created two important organizations—the International Monetary Fund

(IMF) and the World Bank. While the Bretton Woods System was dissolved in

the 1970s, both the IMF and World Bank have remained strong pillars for the

exchange of international currencies. Though

the Bretton Woods conference itself took place over just three weeks, the

preparations for it had been going on for several years. The primary

designers of the Bretton Woods System were the famous British economist John

Maynard Keynes and American Chief International Economist of the U.S.

Treasury Department Harry Dexter White. Keynes’ hope was to establish a

powerful global central bank to be called the Clearing Union and issue a new

international reserve currency called the bancor. White’s plan envisioned a

more modest lending fund and a greater role for the U.S. dollar, rather than

the creation of a new currency. In the end, the adopted plan took ideas from

both, leaning more toward White’s plan. It wasn't until 1958 that the Bretton

Woods System became fully functional. Once implemented, its

provisions called for the U.S. dollar to be pegged to the value of gold.

Moreover, all other currencies in the system were then pegged to the U.S.

dollar’s value. The exchange rate applied