FIN301 Class Web Page, Spring ' 25

Instructor: Maggie Foley

Jacksonville University

The

Syllabus PDF file Risk Tolerance Test (FYI) Term Project Guidelines Grade Calculator

Weekly SCHEDULE, LINKS, FILES and Questions

|

Chapter |

Coverage, HW, Supplements -

Required |

References |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Chapter 1: Introduction Flow

of funds describes the financial assets flowing from various sectors through financial

intermediaries for the purpose of buying physical or financial assets. *** Household, non-financial business, and our government Financial

institutions facilitate exchanges of funds and financial products. ***

Building blocks of a financial system. Passing and transforming funds and

risks during transactions. ***

Buy and sell, receive and deliver, and create and underwrite financial

products. ***

The transferring of funds and risk is thus created. Capital utilization for

individual and for the whole economy is thus enhanced. Part

1 - Who Wants to Chair the Fed? Quiz 1 Game: https://lewis500.github.io/macro/ The

Federal Reserve (Fed) often faces the challenging dilemma of balancing economic

growth with price stability - commonly

referred to as the trade-off between controlling inflation

and minimizing unemployment. 1. Inflation vs. Unemployment

2. Long-term Stability vs. Short-term Relief

3. Uncertainty and Lag Effects

In

the game, you play as the Fed chair and must make interest rate decisions to

strike this delicate balance while keeping inflation and unemployment within

acceptable ranges. Success depends on how well you manage these competing

goals over time. Factors

to Consider:

1.

Current Inflation Rate:

2.

Unemployment Rate:

3.

Economic Growth:

4.

Consumer and Business

Confidence:

5.

Financial Market

Conditions:

6.

Global Economic Trends:

7.

Lag Effects of Monetary

Policy:

8.

Federal Reserve’s Dual Mandate:

In-Class

Debate: Should the Fed Reduce Interest Rates Soon, or Is It Better to Wait?

The next Federal Open Market Committee (FOMC) meeting is scheduled for January 28–29, 2025. Let’s wait and see what unfolds leading up to this critical decision. Chapter 2 Introduction

of Financial Market 1.

What are the six parts of the financial

markets

Money: ·

To pay for purchases and store wealth

(fiat money, fiat currency) Financial

Instruments: ·

To transfer resources from savers to investors

and to transfer risk to those best equipped to bear it. Financial

Markets: ·

Buy and sell financial instruments ·

Channel funds from savers to investors,

thereby promoting economic efficiency ·

Affect personal wealth and behavior of business

firms. Example? Financial

Institutions. ·

Provide access to financial markets,

collect information & provide services ·

Financial Intermediary: Helps get funds

from savers to investors Central

Banks ·

Monitor financial Institutions and

stabilize the economy Regulatory

Agencies ·

To provide oversight for financial system.

2. What are the five core

principals of finance

No homework for chapters 1, 2 |

The Implications of Trump's Return on U.S.

Trade Policy: Will Tariffs and Trade Wars Resurface? (FYI) Background Trump's

presidency (2017-2021) featured aggressive trade policies, including significant

tariffs on China and other trading partners, renegotiations of trade

agreements, and discussions about protecting American manufacturing through

quotas and tariffs.

Key

Insights

1.

Jobs:

2.

Cost of Living: ·

Prices rise for everyday goods (e.g.,

food, clothes, electronics) when tariffs increase import costs. ·

Higher energy costs can have widespread

effects across industries. 3.

Availability of Goods: ·

Imported goods (e.g., seasonal produce,

luxury cars, and tech gadgets) may become limited or delayed. ·

Domestic alternatives might not match global

competition in terms of quality, price, or innovation. Now,

let’s work on this survey about tariffs. Tariff Survey Game: Tariff Trade Simulation A simple game What Determines the

Strength of the US Dollar? (self-produced video) Swiss franc carry trade

comes fraught with safe-haven rally risk (FYI) By Harry Robertson September 2, 20241:03 AM EDTUpdated 5 months ago LONDON, Sept 2 (Reuters) - As investors turn to the Swiss

franc as an alternative to Japan's yen to fund carry trades, the risk of the

currency staging one of its rapid rallies remains ever present. The Swiss franc has long been used in the popular strategy

where traders borrow currencies with low interest rates then swap them into

others to buy higher-yielding assets. Its appeal has brightened further as the yen's has dimmed. Yen

carry trades imploded in August after the currency rallied hard on weak U.S.

economic data and a surprise Bank of Japan rate hike, helping spark global

market turmoil. The Swiss National Bank (SNB) was the first major central bank

to kick off an easing cycle earlier this year and its key interest rate

stands at 1.25%, allowing investors to borrow francs cheaply to invest

elsewhere. By comparison, interest rates are in a 5.25%-5.50% range in

the United States, 5% in Britain, and 3.75% in the euro zone. "The Swiss franc is back as a funding currency,"

said Benjamin Dubois, global head of overlay management at Edmond de

Rothschild STABILITY The franc is near its highest in eight months against the

dollar and in nine years against the euro , reflecting its status as a

safe-haven currency and expectations for European and U.S. rate cuts. But investors hope for a gradual decline in the currency's

value that could boost the returns on carry trades. Speculators have held on to a $3.8 billion short position against

the Swiss franc even as they have abruptly moved to a $2 billion long

position on the yen , U.S. Commodity Futures Trading Commission data shows. "There is more two-way risk now in the yen than there has

been for quite some time," said Bank of America senior G10 FX strategist

Kamal Sharma. "The Swiss franc looks the more logical funding currency

of choice." BofA recommends investors buy sterling against the franc ,

arguing the pound can rally due to the large interest rate gap between

Switzerland and Britain, in a call echoed by Goldman Sachs. The SNB appears set to cut rates further in the coming months

as inflation dwindles. That would lower franc borrowing costs and could weigh

on the currency, making it cheaper to pay back for those already borrowing

it. Central bankers also appear reluctant to see the currency

strengthen further, partly because of the pain it can cause exporters. BofA

and Goldman Sachs say they believe the SNB stepped in to weaken the currency

in August. "The SNB will likely guard against currency appreciation

through intervention or rate cuts as required," said Goldman's G10

currency strategist Michael Cahill. 'INHERENTLY RISKY' Yet the Swissie, as it is known in currency markets, can be an

unreliable friend. Investors are prone to pile into the currency when they get

nervous, thanks to its long-standing safe-haven reputation. Cahill said the franc is best used as a funding currency at

moments when investors are feeling optimistic. A quick rally in the currency used to fund carry trades can

wipe out gains and cause investors to rapidly unwind their positions, as the

yen drama showed. High levels of volatility or a drop in the higher-yielding

currency can have the same effect. The SNB and Swiss regulator Finma declined to comment when

asked by Reuters about the impact of carry trades on the Swiss currency. As stock markets tumbled in early August, the Swiss franc

jumped as much as 3.5% over two days. The franc-dollar pair has proven

sensitive to the U.S. economy, often rallying hard on weak data that causes

U.S. Treasury yields to fall. "Any carry trade

is inherently risky and this is particularly true for those funded with

safe-haven currencies," said Michael Puempel, FX strategist at

Deutsche Bank. "The main risk is that when yields move lower in a

risk-off environment, yield differentials compress and the Swiss franc can

rally," Puempel added. A gauge of how much investors expect the Swiss currency to

move , derived from options prices, is currently at around its highest since

March 2023. "Considering the central banks, you can see how there may

be more sentiment for some carry players to prefer the franc over the

yen," said Nathan Vurgest, head of trading at Record Currency

Management. "The ultimate success of this carry trade might still be

dependent on how quickly it can be closed in a risk-off scenario,"

Vurgest said, referring to a moment where investors cut their riskier trades

to focus on protecting their cash. Get the latest news and expert analysis about the state of the

global economy with the Reuters Econ World newsletter. Sign up here. Reporting by Harry Robertson; Editing by Dhara Ranasinghe and

Alexander Smith Key Insights from the

Article:

1.

Swiss Franc as a Funding

Currency:

2.

Carry Trade Dynamics:

3.

Safe-Haven Risks:

4.

Central Bank Influence:

5.

Strategist Views:

6.

Risks of Swiss Franc

Carry Trades:

7.

Investor Sentiment:

This

analysis highlights the opportunities |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 5 Time value of Money Key Topics Covered: 1.

Future Value (FV): ·

Definition: The amount of money an

investment will grow to after earning interest over a specific period. ·

Formula: See the column to the right for

details. ·

Application: Learn how to calculate the

future value of savings or investments. 2.

Present Value (PV): ·

Definition: The current worth of a future

sum of money or cash flow, discounted at a specific rate. ·

Formula: See the column to the right for

details. ·

Application: Understand how to assess the

value of future payments or investments today. 3.

Payment (PMT): ·

Definition: The fixed payment required to

repay a loan over time, including interest. ·

Formula: See the column to the right for

details. ·

Application: Learn how to calculate

payments for loans, such as car loans or mortgages. 4.

Interest Rate (Rate): ·

Definition: The rate of return or cost of

borrowing, expressed as a percentage. ·

Formula: See the column to the right for

details. ·

Application: Learn how to determine the

interest rate needed to achieve a financial goal. 5.

Number of Periods (NPER): ·

Definition: The number of time periods

required for an investment to reach a specific future value or for a loan to

be paid off. ·

Formula: See the column to the right for

details. ·

Application: Determine how long it will

take to save or grow your money. 6.

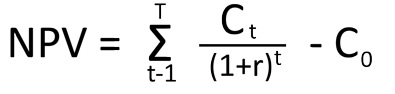

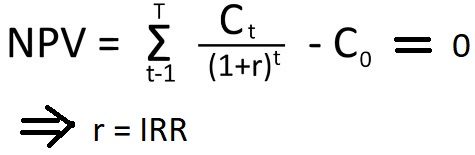

Net Present Value (NPV), Net Future Value

(NFV) ·

Net Present Value (NPV): The difference between the

present value of cash inflows and outflows over a period of time. It is used

to assess the profitability of an investment or project. ·

Net Future Value (NFV): The future value of all

cash inflows and outflows accumulated at a specific interest rate. It

provides a measure of the total future worth of an investment. 7.

Effective Annual Rate (EAR) and Annual

Percentage Rate (APR) ·

Effective Annual Rate (EAR): ·

Annual Percentage Rate (APR): 8. Ordinary Annuity (PMT) and

Annuity Due (PMT, type=1) •

Ordinary Annuity (PMT): •

Annuity Due (PMT, type=1): Real-World Applications:

1.

Planning

for the Future: o Use

TVM concepts to plan for retirement, save for large purchases, or achieve

financial goals. 2.

Loan

Management: o Calculate

loan payments for car loans, mortgages, or student loans. o Compare

loans and understand the cost of borrowing. 3.

Credit

Card Decisions: o Evaluate

interest rates and payment terms to choose the best credit card. 4.

Investment

Opportunities: o Compare

investment options by calculating present and future values. Key Takeaways:

The time value of money - German Nande (video)

Tutoring of Time Value of Money

calculation in Excel (video) Chapter 5 – Escape Room – To Earn

Fake Etherum and Meme Coins Questions in the escape

room exercises: 1.

You

are investing $5,000 (Present Value) in an account that earns 4% annual

interest (Rate) for 8 years (Number of Periods). What is the Future Value of

your investment? (fv=abs(fv(4%, 8,

0, 5000)), or fv =5000*(1+4%)^8) 2.

You are investing $3,000 (Present Value) in

an account that earns 3% annual interest (Rate) for 12 years (Number of

Periods). What is the Future Value of your investment? (fv=abs(fv(3%, 12, 0, 3000)), or fv =3000*(1+3%)^12) 3.

You

need $20,000 in 10 years (Future Value) and can earn 3% annual interest

(Rate). What is the Present Value of your investment? (pv=abs(pv(3%, 10, 0, 20000)), or pv =20000/(1+3%)^10) 4. You need $15,000 in 5 years (Future

Value) and can earn 2% annual interest (Rate). What is the Present Value of

your investment? (pv=abs(pv(2%, 5,

0, 15000)), or pv =15000/(1+2%)^5) 5. You invested $5,000 (Present Value) and it

grew to $6,500 (Future Value) in 5 years. What was the annual interest rate? (rate=rate(5, 0, 5000, -6500)), or

rate = ln(6500/5000)^(1/5)-1) 6. You invested $8,000 (Present Value) and it

grew to $10,000 (Future Value) in 6 years. What was the annual interest rate?

(rate=rate(6, 0, 8000, -10000)), or

rate = ln(10000/5=6000)^(1/6)-1) 7. You invested $5,000 (Present Value) at an

annual interest rate of 4% and it grew to $6,000 (Future Value). How many

years did it take? (nper = nper(4%,

0, 5000, -6000), nper = ln(6000/5000)/(ln(1+4%)) 8. You invested $10,000 (Present Value) at an

annual interest rate of 5% and it grew to $15,000 (Future Value). How many

years did it take? (nper = nper(5%,

0,10000, -15000), nper = ln(15000/10000)/(ln(1+5%)) 9.

You take a $30,000 loan (Present Value) at 4% annual interest (Rate) for 5 years

(Number of Periods). What is your monthly payment? (pmt=pmt(4%/12, 5*12, 30000, 0)) 10. You take a $20,000 loan (Present

Value) at 3% annual interest (Rate) for 10 years (Number of Periods). What is

your monthly payment? (pmt=pmt(3%/12,

10*12, 20000, 0)) Chapter 5 Homework (due with the

first mid term) 1.

You

deposit $5,000 in a saving account at 10% compounded annually. How much is

your first year interest? How much is your second year interest? (500, 550) 2.

What

is the future value of $5,000 invested for 3 years at 10% compounded

annually? ( 6,655) 3.

You

just bought a TV for $518.4 on credit card. You plan to pay back of $50 a

month for this credit card debt. The credit card charges you 12% of interest

rate on the monthly basis. So how long does it take to pay back your credit

card debt? (11 months) 4.

You

are going to deposit certain amount in the next four years. Your saving

account offers 5% of annual interest rate. First year: $800 Second year: $900 Third year: $1000 Fourth year: $1200. How much you can withdraw four years later? (4168.35) (hint:

refer to https://www.jufinance.com/nfv/

) 5.

You

are going to deposit certain amount in the next four years. Your saving

account offers 5% of annual interest rate. First year: $800 Second year: $900 Third year: $1000 Fourth year: $1200. How much is the lump sum value as of today (NPV)? (3429.31)

(Hint: use npv function in excel) 6.

Ten

years ago, you invested $1,000. Today it is worth $2,000. What rate of

interest did you earn? (7.18%) 7.

At

5 percent interest, how long would it take to triple your

money? (22.52) 8.

What

is the effective annual rate if a bank charges you 12 percent compounded

monthly? (12.68%) (hint: use effect function in excel) 9.

Your

father invested a lump sum 16 years ago at 8% interest for your education.

Today, that account worth $50,000.00. How much did your father deposit 16

years ago? ($14594.52) 10.

You

are borrowing $300,000 to buy a house. The terms of the mortgage call for

monthly payments for 30 years at 3% interest. What is the amount of each

payment? ($1264.81) 11.

You

deposit $200 at the beginning of each month into your saving account

every month. After two years (24 deposits total), your account value is

$6,000. Assuming monthly compounding, what is your monthly rate that the bank

provides? (1.74%) 12.

You want to buy a fancy car. For this goal,

you plan to save $5,500 per year, beginning immediately. You will make 4 deposits in an account that

pays 8% interest. Under these

assumptions, how much will you have 4 years from today? ($26,766.31) 13. The Thailand Co. is considering the

purchase of some new equipment. The quote consists of a quarterly payment of

$4,740 for 10 years at 6.5 percent interest. What is the purchase price of

the equipment? ($138,617.88) 14. Today, you are purchasing a 15-year, 8

percent annuity at a cost of $70,000. The annuity will pay annual payments.

What is the amount of each payment? ($8,178.07) 15. Shannon wants to have $10,000 in an

investment account three years from now. The account will pay 0.4 percent

interest per month. If Shannon saves money every month, starting one month

from now, how much will she have to save each month? ($258.81) 16. Trevor's Tires is offering a set of 4

premium tires on sale for $450. The credit terms are 24 months at $20 per

month. What is the interest rate on this offer? (6.27 percent) 17. Top Quality Investments will pay you

$2,000 a year for 25 years in exchange for $19,000 today. What interest rate

are you earning on this annuity? (9.42 percent) 18. Around Town Movers recently purchased a

new truck costing $97,000. The firm financed this purchase at 8.25 percent

interest with monthly payments of $2,379.45. How many years will it take the

firm to pay off this debt? (4.0 years) 19. You just received a credit offer in an

email. The company is offering you $6,000 at 12.8 percent interest. The

monthly payment is only $110. If you accept this offer, how long will it take

you to pay off the loan? (82.17 months) 20. What is the future value of weekly

payments of $25 for six years at 10 percent? ($10,673.90) |

Summary of math and excel equations Math Formula FV = PV *(1+r)^n PV = FV / ((1+r)^n) N = ln(FV/PV) / ln(1+r) Rate = (FV/PV)1/n -1 Annuity: N = ln(FV/C*r+1)/(ln(1+r)) Or N = ln(1/(1-(PV/C)*r)))/ (ln(1+r))

Excel Formulas To get FV, use FV function. =abs(fv(rate, nper,

pmt, pv)) To get PV, use PV

function = abs(pv(rate, nper,

pmt, fv)) To get r, use rate

function =

rate(nper, pmt, pv, -fv) To get number of years,

use nper function = nper(rate, pmt, pv,

-fv) To

get annuity payment, use PMT function = pmt(rate, nper, pv,

-fv) To

get Effective rate (EAR), use Effect function =

effect(nominal_rate, npery) To

get annual percentage rate (APR), use nominal function =

nominal(effective rate, npery) NPV NFV calculator(FYI, might be helpful) Time Value of Money

Calculator |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 3 Financial Statement Analysis Ppt

Quiz on BS and IS

Quiz on Cash Flow

Statement Explaining 4

Financial Statements (youtube)

*************

Introduction *************** Let’s

compare Nike with GoPro based on 10K (www.nasdaq.com) https://www.nasdaq.com/market-activity/stocks/nke/financials https://www.nasdaq.com/market-activity/stocks/nke/financials Nike’s

Income Statement

Nike’s

Balance Sheet

Nike’s

Cash Flow Statement

Nike’s

Financial Ratios

Nike vs GoPro Financial Summary

Let’s

find it out by comparing stock performance between the two firms. Nike Stock Performance (finance.yahoo.com) https://finance.yahoo.com/quote/NKE/

Observations:

******* Part I: Balance Sheet and

Income Statement ************** Home Depot (Ticker in the market:

HD) reported the following information for the year ended January 30th,

2011 (expressed in millions). Sales: $67,977 Cost of goods sold: $44,693 Marketing, general and

administrative expenses: $15,885 Depreciation expenses:

$1,616 Interest expense: $530 Tax rate: 36.70% Number of shares

outstanding: 1,623 Dividends paid to

stockholders: $1,569. Use the above information

to try to prepare the income statement of Home Depot

for the year ended January 30th, 2011 Home Depot (Ticker in the

market: HD) reported the following information for the year ended January 30th,

2011 (expressed in millions). Cash: $545 Accounts receivables: $1,085 Inventories: $10625 Other current assets: $1,224 Gross fixed assets: $38,471 Accumulated depreciation:

$13,411 Other fixed assets: $1,586 Accounts payable: $9,080 Short term notes payable:

$1,042 Long term debt: $11,114 Total common stock: $3,894 Retained earnings: $14,995 Use the

above information to try to prepare the balance sheet

of Home Depot for the year ended January 30th, 2011 |

https://www.nasdaq.com/market-activity/stocks/gpro/financials

GoPro GoPro’s

Income Statement

GoPro’s

Balance Sheet

GoPro’s

Cash Flow Statement

GoPro’s

Financial Ratios

* GoPro

Stock performance ( finance.yahoo.com

) https://finance.yahoo.com/quote/GPRO/

http://www.jufinance.com/10k/bs http://www.jufinance.com/10k/is http://www.jufinance.com/10k/cf Ratio Analysis (plus balance sheet, income statement) http://www.jufinance.com/ratio * |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

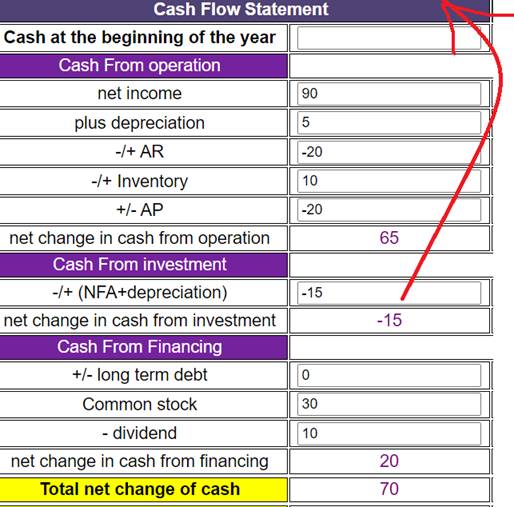

********* Part II: Cash Flow Statement ******************

·

Self produced video On

Cash Flow Statement

·

Cash Flows Explained

(youtbe)

Here

is the cash flow statement of home depot as of 2/2/2014.

Discussion: 2. What does net change in cash mean?

Now

let’s learn how to calculate cash changes in each session Source

of cash

Use

of Cash

Cash

Flow from Operations: Five Steps 1. Add back depreciation. 2. Subtract (add) any increase (decrease) in accounts

receivable. 3. Subtract (add) any increase (decrease) in inventory. 4. Subtract (add) any increase (decrease) in other current

assets. 5. Add (subtract) any increase (decrease) in accounts payable

and other accrued expenses

Chapter 3 HW (due with the First midterm exam) 1.

Firm AAA

just showed how it operated in the prior year. Sales

= $2,000; Cost of Goods Sold = $1,000; Depreciation Expense = $200;

Administrative Expenses = $180; Interest Expense = $30; Marketing Expenses =

$50; and Taxes = $200. Prepare income

statement 2.

A firm has $2000 in current assets, $3000

in fixed assets, $300 in accounts receivables, $300 accounts payable, and

$800 in cash. What is the amount of the inventory? (hint: 900) 3.

A

firm has net working capital of $1000. Long-term debt is $5000, total assets

are $8000, and fixed assets are $5000. What is the amount of the total

equity? (Hint: to find total equity, you need to calculate total debt, which

is a sum of long term debt and short term debt. Short term can be found from

new working capital.) (hint: 1000) 4.

Andre's Bakery has sales of $100,000 with

costs of $50,000. Interest expense is $20,000 and depreciation is $10,000. The

tax rate is 35 percent. What is the amount of tax paid? (hint:

7000)(hint: tax = taxable income * tax rate and taxable income = EBT) 5.

Andre's Bakery has sales of $100,000 with

costs of $50,000. Interest expense is $20,000 and depreciation is $10,000. The

tax rate is 35 percent. The company also paid $3,000 for dividend. What is

the retained earning? (hint: retained earning = net income -

dividend)(hint: 10,000) 6.

The Blue Bonnet's 2018 balance

sheet showed net fixed assets of $2.2 million, and the 2019 balance sheet

showed net fixed assets of $2.6 million. The company's income statement

showed a depreciation expense of $1,000,000. What was the amount of the net

capital spending for 2019? ($1,400,000) 7.

A firm has $500 in inventory,

$1,860 in fixed assets, $190 in accounts receivables, $210 in accounts

payable, and $70 in cash. What is the amount of the current assets? (760) 8.

A firm has net working capital

of $640. Total liability is $5,860. Total assets are $6,230, and fixed assets

are $3,910. What is the amount of long term debt? (4180) 9.

Which one of the following is

a use of cash? (answer: B) 10. A firm generated net income of $878. The depreciation

expense was $40 and dividends were paid in the amount of $25. Accounts

payables decreased by $13, accounts receivables increased by $20, inventory

decreased by $14, and net fixed assets decreased by $8. There was no interest

expense. What was the net cash flow from operating activity? (899) 11.

Teddy’s Pillows has beginning net fixed assets of $480 and ending net fixed

assets of $530. Assets valued at $300 were sold during the year. Depreciation

was $40. What is the amount of capital spending? (90) 12.

Art’s Boutique has sales of $640,000 and costs of $480,000. Interest expense

is $40,000 and depreciation is $60,000. The tax rate is 34%. What is the net

income? (39,600) |

(The excel file of the above cash flow statement is

here) More

exercises of chapter 3 (word file here) (solution) In class exercise 1.

Refer to the above table. Inventory has increased from $18,776

to $21,908. This is ____________ of cash; Long term

debt has increased from $9,800 to $11,500. This is ____________ of

cash. 2.

Prepare cash flow statement based on

information given Increase

in accounts receivable $20 Decrease

in inventory 10 Operating

income 120 Interest

expense 20 Decrease

in accounts payable 20 Dividend 10 Increase

in common stock 30 Increase

in net fixed asset 10 Depreciation 5 Income

tax 10 Beginning

cash 100 Why is

Investment Cash flow -$15? Assume

that Net fixed assets =$10 in previous year. Depreciation

= $5 è Net fixed assets will drop by $5 due to depreciation, so net fixed assets should be $10-$5=$5,

if the company has done nothing on fixed assets. However,

increase in Net Fixed Asset = $10 è net fixed assets = $10 + $10 = $20 this

year. How

much has been spent on fixed assets? $20-$5=$15

è It is a cash outflow, so -$15.

Solution: see above Note:

NI = EBIT – Interest – Tax = 120-20-10=90 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 4: Ratio

Analysis 3 Minutes! Financial Ratios & Financial

Ratio Analysis Explained & Financial Statement Analysis

Ratio

analysis template ( https://www.jufinance.com/ratio) Stock

screening tools FINVIZ.com http://finviz.com/screener.ashx We will focus on the following several ratios: P/E (price per share/earning per share, P/E < 15, a bargain) PEG (PE ratio / growth rate. PEG<1, undervalued stock)

(optional) EPS (earning per share) ROA (Return on Asset = NI/TA, ROA>10% should be a nice benchmark) ROE (return on equity = NI/TE, ROE>15% should be good) Current ratio (liquidity measure. = CA/CL, has to be

greater than one) Quick ratio (liquidity measure. = (CA-Inventory)/CL, has to be greater

than one) Debt Ratio (Leverage measure. = TD/TA, need to be optimal, usually

between 30% and 40%) Gross margin (profit measure. = EBITDA/sales, or = Gross margin/sales,

has to be positive) Operating margin (profit measure. = EBIT/sales, or = operating

income/sales, has to be positive) Net profit margin (profit measure. = NI/sales, has to be

positive) Payout ratio (= dividend / NI, measures distribution to shareholders.

No preferences. Usually value stocks have high payout ratio; Growth stocks

have low payout ratio). Total assets turnover = Sales/TA Inventory turnover ratio = Sales/Inventory Fixed assets turnover ratio = Cost of goods sold / Fixed assets Ratios &

Margins Nike Inc. Cl B

All values updated annually at fiscal year

end

Valuation

https://www.wsj.com/market-data/quotes/NKE/financials

In class exercise

How much is ROA in 2009? ROA in 2009? Quick

Ratio? Current Ratio? Debt Ratio? Payout Ratio? Operating margin? Net profit

margin? If the company’s stock is traded at $40 per

share and there are 2,000 shares outstand. How much is PE? Homework of chapter 4 ( due with the first midterm exam) 1. 1 .A firm has total

equity of $2,000 and a debt-equity ratio of 2. What is the value of the total

assets? (answer: $6,000) 2, The Co. has sales =

$50 million, total assets = $30 million, and total debt = $15 million. The

profit margin = 20%. What is the return on equity (ROE)? (answer: 66.67%. Hint: TE= 15 million; NI =10 million) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Firm Midterm

Exam Solutions T/F Calculations Study

Guide 2.25.

- In Class Exam - Closed Book Closed

Notes

Time

Value of Money (TVM) - You Should Know:

Financial

Statements - You Should Know:

Cash

Flow - You Should Know:

Understanding

cash flow is important

because it shows how money moves in and out of a business. Even if a company

is profitable, it can still run out of cash if it doesn’t

manage its finances well. 1. What is Cash Flow?

2. Three Sections of the Cash Flow Statement

Operating

Activities (Day-to-Day Business Cash Flow)

Investing

Activities (Buying & Selling Assets)

Financing Activities (Raising Money &

Paying Debt)

3. Cash Flow vs. Profit –

What’s the Difference?

Example: A

company sells $10,000 worth of products but only collects $2,000 in cash now.

Profit looks good on paper, but cash

flow is low, which could cause trouble paying bills! 4. Why is Cash Flow Important?

·

Tells if a company can

survive – A company needs

enough cash to pay expenses. ·

Shows real financial

health – Net income

(profit) can be misleading, but cash flow is real. ·

Helps in decision-making – Investors look at cash flow to see if a company is a good

investment. 5. Key Cash Flow Red Flags

·

Negative Operating Cash

Flow – The company

isn't making enough money from its business. ·

High Debt Payments – If too much cash is going toward debt, the company may

struggle. ·

Declining Free Cash Flow – Less money available for growth or returning money to

investors. Final Takeaways

Financial

Ratios - You Should Know:

Liquidity Ratios (Can a company pay its

short-term bills?)

Profitability Ratios (Is the company

making money?)

Efficiency Ratios (How well does the

company use its assets?)

Leverage Ratios (How much debt does the

company have?)

Market Ratios (How valuable is the

company’s stock?)

Final Reminders:

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 6 Risk and Return ppt Quiz

on Diversification Quiz on CAPM

ICE Data and Results Topic

1: Single Stock - Risk and Return Tradeoff

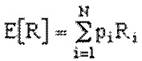

Given a

probability distribution of returns, the expected return can be calculated

using the following equation:

where

https://www.zenwealth.com/businessfinanceonline/RR/ExpectedReturn.html Given an asset's

expected return, its variance can be calculated using the following equation:

where

The standard deviation

is calculated as the positive square root of the variance.

https://www.zenwealth.com/businessfinanceonline/RR/MeasuresOfRisk.html Exercise: Stock A has the following returns for various

states of the economy:

Stock A's expected return is? Standard

deviation? Solution: · Expected return = 10%*(-30%)) + 20%*(-2%) +

40% *10% + 20%*18% + 10%*40% = 8.2% · Standard deviation (not required) = sqrt(10%*(-30%-8.2%)2 +

20%*(-2%-8.2%)2 +40%*(10%-8.2%)2 +

20%*(18%-8.2%)2 +10%*(40%-8.2%)2) = 16.98% Or, https://www.jufinance.com/return/

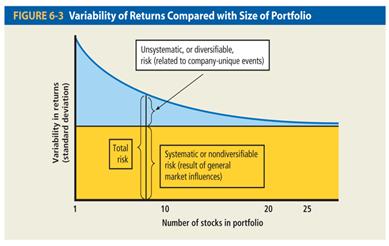

Drawbacks of Holding One Stock: ·

Holding

only one stock is risky due to lack of diversification. ·

All

your “eggs” are in one basket, so company-specific bad news can severely hurt

your portfolio. ·

This

concentration leads to high volatility and uncompensated risk – risk

that could be diversified away but isn’t. Topic

2: A Portfolio with Two Stocks - Risk

and Return Tradeoff Quiz Key

Insights on Two-Stock Portfolio and Diversification

1) If

two stocks have high correlation (+1),

they move together, offering little

risk reduction. 2) If

they have low correlation (~0),

they move independently, reducing

overall volatility. 3) If

they have negative correlation

(-1), one stock rises while the other falls, potentially eliminating risk.

For example: By thoughtfully selecting stocks with varying correlations

to NVIDIA, investors can construct a portfolio that balances potential

returns with reduced risk. 1. NVIDIA and Intel Corporation (INTC):

2. NVIDIA and Amazon.com Inc. (AMZN):

3. NVIDIA and Advanced Micro Devices, Inc. (AMD):

Key Takeaways:

W1 and W2 are the percentage of

each stock in the portfolio.

Exercise: Stocks A and B have the following returns for

various states of the economy:

Solution: (or use calculator at https://www.jufinance.com/return/) Stock 1: · Expected return = 10%*(-30%)) + 20%*(-2%) +

40% *10% + 20%*18% + 10%*40% = 8.2% · Standard deviation (not required) = sqrt(10%*(-30%-8.2%)2 +

20%*(-2%-8.2%)2 +40%*(10%-8.2%)2 +

20%*(18%-8.2%)2 +10%*(40%-8.2%)2) = 16.98% Stock 2: · Expected return = 10%*(10%)) + 20%*(2%) + 40%

*1% + 20%*2% + 10%*(-5)% = 1.7% · Standard deviation (not required) =

sqrt(10%*(10%-1.7%)2 + 20%*(2%-1.7%)2 +40%*(1%-1.7%)2 +

20%*(2%-1.7%)2 +10%*((-5)%-1.7%)2) = 3.41% Covariance (not required): · Covariance =

10%*(-30%-8.2%)*(10%-1.7%)+20%*(-2%-8.2%)*(2%-1.7%)+40%*(10%-8.2%)*(1%-1.7%)+20%*(18%-8.2%)*(2%-1.7%)+10%*(40%-8.2%)*((-5%)-1.7%)

= -0.54% Correlation (not required): · Correlation = -0.54%/(16.98%* 3.41%) = -0.93

Topic

3: A Portfolio with Three Stocks -

Risk and Return Tradeoff Quiz Key Insights:

1) Tech stock

(growth potential) 2) Consumer staples stock

(stable in recessions) 3) Utility stock

(defensive, steady returns) 6. Bottom Line: The third stock acts as a buffer, making the portfolio more

resilient and reducing reliance on any single stock or sector. In class Exercise 1.

Pick three stocks. Has to be the leading firm

in three different industries. We

chose Stock 1, Stock 2,

Stock 3 (Use following app to get monthly stock returns in the past

five years) https://script.google.com/macros/s/AKfycbxao_yHFToaMAs2fuEiYMfHapioFAjIukvBAFyJIOS6ccYL2WAepMMyrO8afpRjsVBA/exec) · Stock Prices Raw Data, Risk, Beta, CAPM (stock

1, Stock 2, Stock 3, S&P500 (Raw data), will be updated based

on the new stocks chosen in class (template)) 2. From finance.yahoo.com, collect stock prices

of the above firms, in the past five years Steps: · Goto finance.yahoo.com,

search for the company · Click

on “Historical prices” in the left column on the top and choose monthly stock

prices. · Change

the starting date and ending date to “1/31/2020” and “1/31/2025”,

respectively. · Download

it to Excel · Delete

all inputs, except “adj close”

– this is the closing price adjusted for dividend. · Merge

the three sets of data just downloaded 3. Evaluate the performance of each stock: · Calculate

the monthly stock returns. · Calculate

the average return · Calculate

standard deviation as a proxy for risk · Calculate

correlation among the three stocks. · Calculate

beta. But you need to download S&P500 index values in the past five years from

finance.yahoo.com. · Calculate stock returns based on CAPM. · Draw SML

· Conclusion and take away?

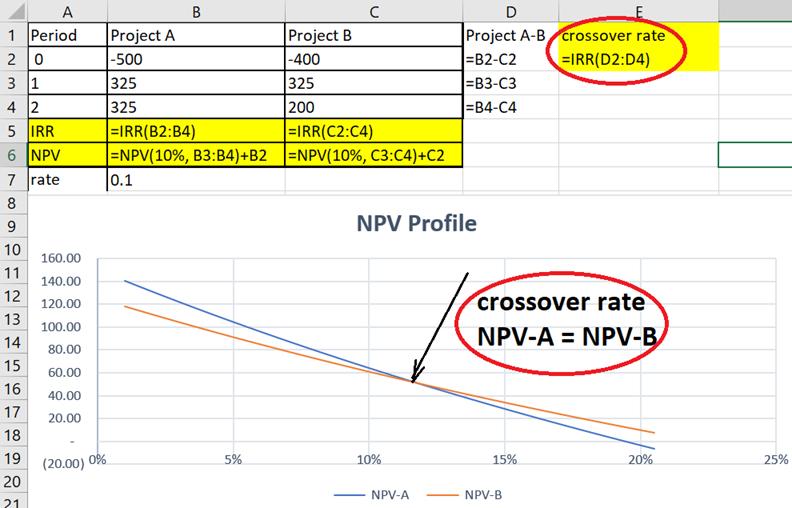

Conclusion:

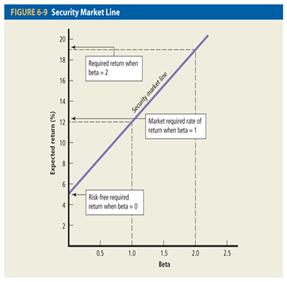

More than 25 stocks should do the trick for diversification. Quiz Please refer to template Topic 4 - What Is the Capital Asset Pricing

Model? Quiz

The Capital Asset Pricing Model (CAPM)

describes the relationship between systematic risk and expected

return for assets, particularly stocks. CAPM is widely used throughout

finance for pricing risky securities and generating expected

returns for assets given the risk of those assets and cost of capital. Ri = Rf + βi *

(Rm - Rf) ------ CAPM model Ri = Expected return

of investment Rf =

Risk-free rate βi =

Beta of the investment Rm =

Expected return of market (Rm -

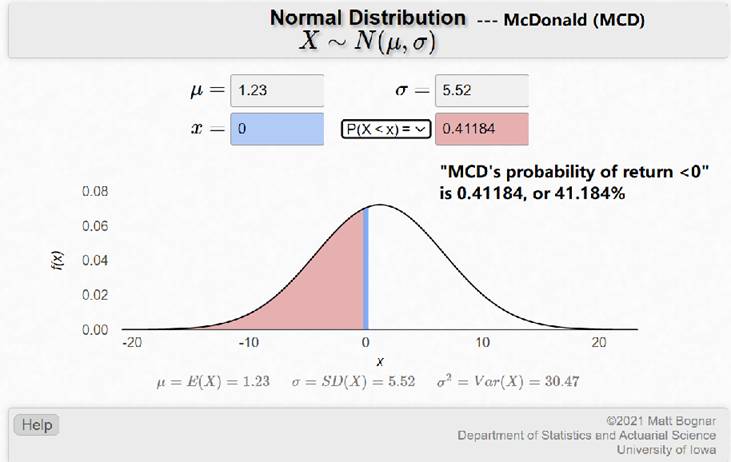

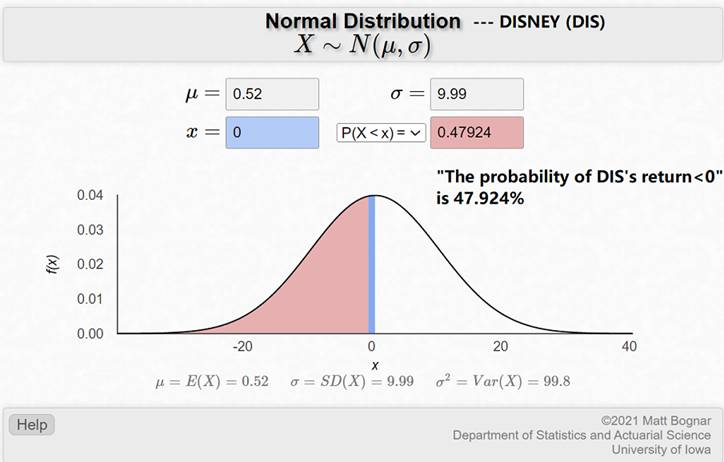

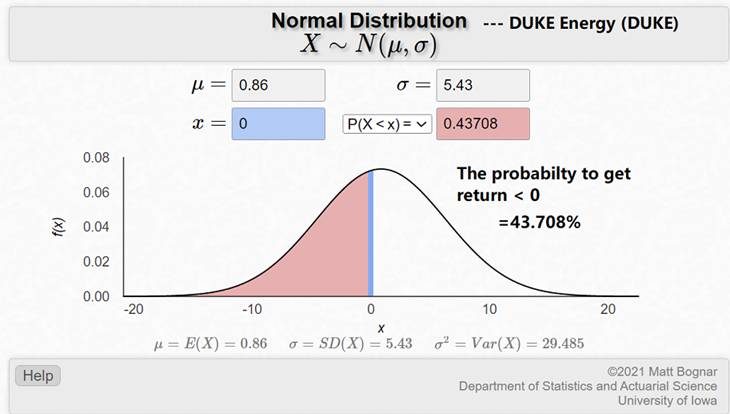

Rf) = Market risk premium Topic 5 – Normal Distribution – Predict Stock

Returns (FYI only)

Stock Price Normal Distribution (FYI) ( https://homepage.divms.uiowa.edu/~mbognar/applets/normal.html) For

example: from our in class exercise

Excel

command to get the probability to earn less than 0% for MCD: =NORM.DIST(0%,

1.23%, 5.52%, 1)

Excel

command to get the probability to earn less than 0% for DIS: =NORM.DIST(0%,

0.52%, 9.99%, 1)

Excel

command to get the probability to earn less than 0% for DUKE: =NORM.DIST(0%,

0.86%, 5.43%, 1) Topic 6: Step-by-Step Guide for Screening Mutual

Funds (FYI)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Advice Category |

Key Insights |

|

Reducing Unsystematic vs. Systematic Risk |

Adding more stocks reduces company-specific risk (unsystematic

risk), but market-wide risk (systematic risk) remains. Diversification

helps prevent the collapse of an entire portfolio due to one company's

failure. |

|

Diminishing Marginal Benefits of Diversification |

The first few added stocks provide the greatest risk

reduction. Research shows about 20 well-chosen stocks across industries

eliminate most diversifiable risk. Beyond that, the additional benefit

diminishes. |

|

Sector & Asset Allocation Diversification |

True diversification isn’t just about quantity but variety.

Stocks should be spread across different sectors (tech, healthcare, energy,

etc.) and asset classes (stocks, bonds, real estate) to improve stability. |

|

Balancing Risk and Return |

The risk-return tradeoff remains: higher returns require

higher risk. However, diversification allows investors to lower risk

without significantly reducing returns. A well-balanced portfolio smooths

out volatility while capturing market gains. |

Chapter 6 Homework (due with the second midterm exam)

Need help? Watch this guide video: Chapter 6 Homework Help

1)

Stock A has the following returns for various states of the economy:

State

of

the

Economy Probability Stock

A's Return

Recession 10% -30%

Below

Average 20% -2%

Average 40% 10%

Above

Average 20% 18%

Boom 10% 40%

Stock

A's expected return is? (ANSWER: 8.2%)

2)

Joe purchased 800 shares of Robotics Stock at $3 per share on 1/1/19. Bill

sold the shares on 12/31/19 for $3.45. Robotics stock has a beta of 1.9, the

risk-free rate of return is 4%, and the market risk premium is 9%. Joe's

holding period return is? (ANSWER:

15%)

3. You

own a portfolio with the following expected returns given the various states

of the economy. What is the overall portfolio expected return? (ANSWER:

9.05%)

State

of

economy probability

of state of

economy rate

of return if state occurs

Boom 27% 14%

Normal 70% 8%

Recession 3% -11%

4)

The prices for the Electric Circuit Corporation for the first quarter of 2019

are given below. The price of the stock on January 1, 2019 was

$130. Find the holding period return for an investor who purchased the stock

onJanuary 1, 2009 and sold it the last day of March 2019. (ANSWER: 2.12%)

Month

End Price

January $125.00

February 138.50

March 132.75

5)

Collectibles Corp. has a beta of 2.5 and a standard deviation of returns of

20%. The return on the market portfolio is 15% and the risk free rate is 4%.

What is the risk premium on the market?

(ANSWER: 11%)

6)

An investor currently holds the following portfolio:

Amount

Invested

8,000

shares of

Stock A $16,000 Beta = 1.3

15,000

shares of Stock B $48,000 Beta = 1.8

25,000

shares of Stock C $96,000 Beta = 2.2

The

beta for the portfolio is? (ANSWER:

1.99)

7)

Assume that you have $165,000 invested in a stock that is returning 11.50%,

$85,000 invested in a stock that is returning 22.75%, and $235,000 invested

in a stock that is returning 10.25%. What is the expected return of your

portfolio? (ANSWER: 13%)

8)

If you hold a portfolio made up of the following stocks:

Investment

Value Beta

Stock

A $8,000 1.5

Stock

B $10,000 1.0

Stock

C $2,000 .5

What

is the beta of the portfolio? (ANSWER:

1.15)

9. The risk-free rate of

return is 3.9 percent and the market risk premium (rm –rf)

is 6.2 percent. What is the expected rate of return on a stock with a beta of

1.21? (ANSWER: 11.4%)

10. You own a portfolio consisting of the stocks below.

Stock Percentage

of

portfolio Beta

1. 20% 1

2. 30% 0.5

3. 50% 1.6

The risk free rate is 3% and

market return is 10%.

a. Calculate

the portfolio beta. (ANSWER:

1.15)

b. Calculate

the expected return of your portfolio. (ANSWER: 11.05%)

11. Computing holding period return for Jazman and

Solomon for period 1 through 3 (bought in period 1 and sold in period 3).

Show the holding period returns for each company. (ANSWER: 50%, -25%)

Period Jazman Solomon

1 $10 $20

2 $12 $25

3 $15 $15

12. Calculate expected return

(ANSWER:

12%)

|

State of the economy |

Probability of the states |

% Return (Cash Flow/Inv. Cost) |

|

Economic Recession |

30% |

5% |

|

Strong and moderate Economic Growth |

70% |

15% |

13. Calculate the expected returns of the

following cases, respectively

1) Invest

$10,000 in Treasury bill with guaranteed return of 4%. (ANSWER: 4%)

2) Investment

$10,000 in Apple. 50% possibility to earn 20% return and 50% possibility to

lose 10% of investment.(ANSWER: 5%)

3) Investment

$10,000 in Wal-Mart. 50% possibility to earn 5% return and 50% possibility to

earn 0% of investment.(ANSWER: 2.5%)

14. Rank the risk of the following cases, from

the least risky one the most risky one

(ANSWER: 1, 3, 2)

1) Invest

$10,000 in Treasury bill with guaranteed return of 4%.

2) Investment

$10,000 in Apple. 50% possibility to earn 20% return and 50% possibility to

lose 10% of investment.

3) Investment

$10,000 in Wal-Mart. 50% possibility to earn 5% return and 50% possibility to

earn 0% of investment.

15. An

investor currently holds the following portfolio:

Amount

Invested

8,000

shares of

Stock A $10,000 Beta = 1.5

15,000

shares of Stock B $20,000 Beta = 0.8

25,000

shares of Stock C $20,000 Beta = 1.2

Calculate

the beta for the portfolio.(ANSWER:

1.1)

Excel Command:

sumproduct(array1,

array2) ---- to get expected returns

stdev(observation1,

obv2, obv3,….) ---- to get standard deviation

correl(stock

1’s return, stock 2’s return) --- to get correlation between stocks

beta

= slope(stock return, sp500 return) --- to get the stock’s beta

Holding

Period Return Calculator

Two

Stock Portfolio Return and Standard Deviation

FYI only

![]()

W1 and W2 are the percentage of each stock in the

portfolio.

![]()

- r12 = the

correlation coefficient between the returns on stocks 1 and 2,

- s12 = the

covariance between the returns on stocks 1 and 2,

- s1 = the

standard deviation on stock 1, and

- s2 = the

standard deviation on stock 2.

![]()

- s12 = the

covariance between the returns on stocks 1 and 2,

- N = the number of states,

- pi = the probability of state i,

- R1i = the return on stock 1 in state i,

- E[R1] = the expected return on stock 1,

- R2i = the return on stock 2 in state i, and

- E[R2] = the expected return on stock 2.

2022 High Beta Stocks List | The 100 Highest Beta S&P 500

Stocks (FYI)

Updated

on September 15th, 2022 by Bob Ciura

https://www.suredividend.com/high-beta-stocks/

#5: Fortinet, Inc. (FTNT)

Fortinet,

Inc. provides broad, integrated, and automated cybersecurity solutions around

the world. It offers FortiGate hardware and software licenses that provide

various security and networking functions. Fortinet is a large-cap stock with

a market cap above $40 billion.

In

the 2022 second quarter, Fortinet generated revenue of $1.03 billion, up 29%

from the same quarter last year. Product and service revenue grew 34% and

25%, respectively. Adjusted earnings-per-share increased 26% year-over-year.

For

2022, Fortinet expects revenue of $4.25 billion to $4.40 billion, consisting

of $2.62 billion to $2.67 billion in service revenue. Billings are expected

between $5.56 billion and $5.64 billion. Adjusted earnings-per-share are

expected in a range of $1.01 to $1.06 for the full year.

FTNT

has a Beta value of 1.71.

#4: Paycom Software Inc. (PAYC)

Paycom

is a technology stock that produces cloud-based human capital management

(HCM) as-a-service software. Services help employers manage a variety of HCM

tasks such as talent acquisition, and time and labor management.

In

the most recent quarter, Paycom generated $317 million in revenue, up 31%

year-over-year. Recurring revenue grew 31%, and represented 98% of total

revenue. Earnings-per-share of $1.26 increased 30% compared with $0.97 in the

year-ago quarter.

PAYC

has a Beta

value of 1.71.

#3: ServiceNow (NOW)

ServiceNow

is a high-quality technology company, which transforms old, manual ways of

working into modern digital workflows. It reduces the complexity of jobs and

makes work more pleasant to employees, thus resulting in increased

productivity.

ServiceNow

currently has more than 7,400 enterprise customers, which include about 80%

of the Fortune 500. All these customers use the Now Platform, which is an

intelligent cloud platform that carries out their digital transformation.

ServiceNow

is a leader in the digital transformation of companies towards making work

better for their employees. According to a research of IDC, more than $3

trillion has been invested in digital transformation initiatives but only 26%

of the investments have delivered acceptable returns.

NOW has

a Beta value of 1.77.

#2: Advanced Micro Devices (AMD)

Advanced

Micro Devices was founded in 1959 and in the decades since it has become a

sizable player in the chip market. AMD is heavy in gaming chips, competing

with others like NVIDIA for the lucrative, but competitive market.

In

the 2022 second quarter, AMD reported revenue of $6.6 billion. This was a 70%

year-over-year increase, driven by organic growth as well as the contribution

from Xilinx. Gross margin contracted two percentage points to 46% for the

quarter. Operating income rose 22% to $526 million. Adjusted

earnings-per-share of $1.05 increased 67%.

AMD has

a Beta value of 2.09.

#1: NVIDIA Corporation (NVDA)

NVIDIA

Corporation is a specialized semiconductor company that designs and

manufactures graphics processors, chipsets and related software products.

Its

products include processors that are specialized for gaming, design,

artificial intelligence, data science and big data research, as well as chips

designed for autonomous vehicles and robots.

Over

the last five years, NVIDIA’s growth exploded. This

growth was partially driven by cryptocurrency mining, although that has

mostly ceased to be a tailwind, and future growth will be centered on other

growth drivers. NVIDIA’s GPUs are very versatile in

AI applications, which was an unintended benefit of the company’s research and development efforts.

The

company has immediately started to capitalize on this trend by offering GPUs that

are optimized for deep learning and other specialized applications. These

GPUs act as the brains of computers, robots, and self-driving cars. Those

GPUs are, among others, utilized in professional visualization and data

centers. The markets NVIDIA supplies GPUs for have strong growth tailwinds,

which bodes well for NVIDIA’s long-term revenue

outlook.

NVDA

has a Beta value of 2.31.

Negative Beta Stocks | The 1 Negative Beta S&P 500 Stock

In 2022 (FYI)

Updated

on January 19th, 2022 by Bob Ciura

https://www.suredividend.com/negative-beta-stocks/

Negative

Beta Stock: Clorox Company (CLX)

With

over 40 years of dividend increases, Clorox is on the exclusive Dividend

Aristocrats list.

Clorox

is a manufacturer and marketer of consumer and professional products,

spanning a wide array of categories from charcoal to cleaning supplies to

salad dressing.

More

than 80% of its revenue comes from products that are #1 or #2 in their

categories across the globe, helping Clorox produce more than $7 billion in

annual revenue.

Clorox

reported first quarter earnings on November 1st, 2021, and results were

better than expected, although expectations were low.

Total

revenue declined nearly –6% year–over–year to $1.8 billion, as organic sales

fell –5% during the quarter. The decline was due to unfavorable pricing and

mix, a decline in volume, and forex translation.

Cleaning

and professional products were higher, but consumer products like vitamins

and supplements posted strong declines.

Clorox

stock has a Beta value of -0.24.

https://ycharts.com/companies/CLX/performance/price

Chapter 7 Bond pricing

·

Ppt

Yield Curve http://finra-markets.morningstar.com/BondCenter/Default.jsp 3/24/2025

https://www.gurufocus.com/yield_curve.php

Investing

Basics: Bonds(video)

FINRA

– Bond market information

https://www.finra.org/finra-data/fixed-income

Chapter 7 Study guide

1.

Go to https://www.finra.org/finra-data/fixed-income,

the bond market data website of FINRA to find bond information. For example,

find bonds sponsored by Wal-mart

Corporate

Bond

Understand what is coupon,

coupon rate, yield, yield to maturity, market price, par value, maturity,

annual bond, semi-annual bond, current yield. https://finra-markets.morningstar.com/BondCenter/

For

WALMART bond Symbol: WMT5571329CUSIP: 931142FE8 Bond Type: CORP

https://www.finra.org/finra-data/fixed-income/bond?symbol=WMT5571329&bondType=CORP

3. 3. Understand how to

price bond

Bond price = abs(pv(yield, maturity, coupon, 1000)) ------- annual coupon

Bond price = abs(pv(yield/2, maturity*2, coupon/2, 1000))

------- semi-annual coupon

Also change the yield and observe the price changes.

Summarize the price change pattern and draw a graph to demonstrate your

findings.

Again, when yield to maturity of this semi_annual coupon

bond is 3%, how should this WMT bond sell for?

4. Understand how to

calculate bond returns

Yield to maturity = rate(maturity,

coupon, -market price, 1000) – annual coupon

Yield to maturity = rate(maturity*2,

coupon/2, -market price, 1000)*2 – semi-annual coupon

For example, when the annual coupon bond is selling for

$1,200, what is its return to investors?

For example, when the semi-annual coupon bond

is selling for $1,200, what is its return to investors?

5. Current yield: For the

above bond, calculate current yield

(hint: current yield = annual

coupon / bond price)

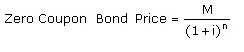

6. Zero coupon bond:

coupon=0 and treat it as semi-annual coupon bond.

Example:

A ten year zero coupon bond is selling for $400. How much is its yield to

maturity?

A ten year zero coupon bond’s yield to maturity is 10%.

How much is its price?

7. Understand

what is bond rating and how to read those ratings. (based on z

score. What is z score?)

a. Who are Moody,

S&P and Fitch?

b. What is IBM’s

rating?

c. Is the rating

for IBM the highest?

d. Who earned the

highest rating?

8.

Understand the cash flows from a bond as a bond investor

For

example, a five year, annual coupon bond, with 5% coupon rate. Its cash flows

are as follows.

Chapter 7 Home

Work (due with the second mid-term)

Instructor Walkthrough for Chapter 7 Homework: Click to watch

1. IBM

5 year 2% annual coupon bond is selling for $950. How much

this IBM bond’s YTM? 3.09%

2. IBM

10 year 4% semi_annual coupon bond is selling for $950. How

much is this IBM bond’s YTM? 4.63%

3. IBM

10 year 5% annual coupon bond offers 8% of return. How much

is the price of this bond? 798.7

4. IBM

5 year 5% semi-annual coupon bond offers 8% of return. How

much is the price of this bond? $878.34

5. IBM

20 year zero coupon bond offers 8% return. How much is the price of this

bond? 208.29

6. Collingwood

Homes has a bond issue outstanding that pays an 8.5 percent coupon and

matures in 18.5 years. The bonds have a par value of $1,000 and a market

price of $964.20. Interest is paid semiannually. What is the yield to

maturity? 8.9%

7. Grand

Adventure Properties offers a 9.5 percent coupon bond with annual payments.

The yield to maturity is 11.2 percent and the maturity date is 11 years from

today. What is the market price of this bond if the face value is

$1,000? 895

8. The

zero coupon bonds of D&L Movers have a market price of $319.24, a face

value of $1,000, and a yield to maturity of 9.17 percent. How many years is

it until these bonds mature? 12.73 years

9. A

zero coupon bond with a face value of $1,000 is issued with an initial price

of $212.56. The bond matures in 25 years. What is the yield to

maturity? 6.29%

10.

The bonds issued by Stainless Tubs bear a 6 percent coupon, payable semiannually.

The bonds mature in 11 years and have a $1,000 face value. Currently, the

bonds sell for $989. What is the yield to maturity? 6.14%

Summary of bond pricing EXCEL functions

To calculate bond price (annual coupon bond):

Price=abs(pv(yield to maturity, years left to maturity,

coupon rate*1000, 1000)

To calculate yield to maturity (annual coupon

bond):

Yield to maturity = rate(years left to

maturity, coupon rate *1000, -price, 1000)

To calculate bond price (semi-annual

coupon bond):

Price=abs(pv(yield to maturity/2, years

left to maturity*2, coupon rate*1000/2, 1000)

To calculate yield to maturity (semi-annual

coupon bond):

Yield to maturity = rate(years left to

maturity*2, coupon rate *1000/2, -price, 1000)*2

To calculate number of years left(annual

coupon bond)

Number of years =nper(yield to

maturity, coupon rate*1000, -price, 1000)

To calculate number of years left(semi-annual

coupon bond)

Number of years =nper(yield to

maturity/2, coupon rate*1000/2, -price, 1000)/2

To calculate coupon (annual coupon bond)

Coupon = pmt(yield to maturity, number of

years left, -price, 1000)

Coupon rate = coupon / 1000

To calculate coupon (semi-annual coupon bond)

Coupon = pmt(yield to maturity/2, number of

years left*2, -price, 1000)*2

Coupon rate = coupon / 1000

Current Yield = annual coupon / bond market price

·

Current yield is the return you earn just from

the bond’s coupon payments, not including any price gain or loss (this is

capital gain yield).

·

Yield to maturity = total return =

current yield + capital gain yield

Math

Formula (FYI)

C: Coupon, M: Par, $1,000; i: Yield to maturity; n:

years left to maturity

For Semi-annual, F=2 for semi-annual coupon

M: Par, $1,000; i: Yield to maturity; n:

years left to maturity

Second Midterm

Exam (chapters 6 and 7 only)

·

Date: 4/3

·

T/F Solution (33

questions, 33*1.5=49 points, closed book close notes)

·

Multiple

Choice Solution (17 questions, 17*3=51 points)

Chapter 6 Study Guide

1.

Single Stock – Risk & Return Tradeoff

- Expected Return (E[R]): Weighted average of returns

using probabilities.

v Formula: E[R] = Σ (pi * Ri)

- Variance & Standard Deviation: Measures of total risk

(volatility).

v Std Dev = √Variance

- Higher standard deviation = more risk

- Holding one stock = High risk (lack of

diversification)

- Risk

cannot be eliminated with one stock.

2.

Two-Stock Portfolio

- Diversification: Reduces risk if stocks are not perfectly

correlated.

- Correlation (ρ):

v +1 = perfect positive (no diversification benefit)

v 0 = no relationship (moderate benefit)

v -1 = perfect negative (best risk reduction)

- Portfolio Variance depends on weights, std dev,

and correlation.

- Correlation

example: -0.93 between Stock A and B (strong diversification)

- You

can lower risk without lowering return via diversification.

3.

Three-Stock Portfolio

Key Concepts:

- More stocks = more diversification

- Correlation is key: Low/negative correlation

helps most.

- Portfolio Expected Return = Weighted average of

individual expected returns.

- Combining

3 stocks reduces risk more than 2, especially from different sectors.

- After

~20 well-chosen stocks, diversification benefit flattens.

4.

Capital Asset Pricing Model (CAPM)

Key Formula:

- Ri

= Rf + βi * (Rm - Rf)

Key Concepts:

- Beta (β): Measures stock’s volatility relative to the market.

1.

β

= 1 → same risk as market

2.

β

> 1 → more volatile

3.

β

< 1 → less volatile

- Market Risk Premium (Rm - Rf): Additional return for

market risk.

- High

beta = higher expected return under CAPM

- Risk-free

rate = return with no risk (e.g., T-bills)

- Only

systematic risk is priced

in CAPM, not company-specific risk.

5.

Portfolio Concepts

Key Concepts:

- Expected Portfolio Return = Weighted average of

individual returns

- Portfolio Beta = Weighted average of each stock's beta

- Unsystematic Risk (company-specific): Can be

diversified away

- Systematic Risk (market risk): Cannot be diversified away

- Diversification reduces unsystematic risk

only

Chapter 7 Study Guide

1. Bond Basics

Understand

these key terms:

|

Term |

Meaning |

|

Par Value |

The face

value of the bond, usually $1,000. |

|

Coupon Rate |

The % of par

paid annually/semi-annually as interest. |

|

Coupon Payment |

Actual

dollar payment (e.g., 5% of $1,000 = $50 annually). |

|

Market Price |

Current

price the bond is trading at (may be above/below par). |

|

Maturity |

The time

when bond repays principal ($1,000). |

|

Yield to Maturity (YTM) |

Investor’s

total return if held to maturity. |

|

Current Yield |

= Annual

Coupon ÷ Current Market Price. |

|

Zero Coupon Bond |

Pays no

coupon. Only pays $1,000 at maturity. |

|

Annual vs. Semiannual |

Semiannual

bonds pay 2x per year, so divide rate and double periods in formulas. |

2. Bond Price-Yield Relationship

- Inverse Relationship:

- When

YTM ↑, Bond Price ↓

- When

YTM ↓, Bond Price ↑

Key takeaway:

Rising interest rates cause bond prices to fall and vice versa.

3. Bond Pricing Formulas

- Annual

Coupon Bond:

Price = abs(pv(YTM, N, Coupon, 1000)) - Semi-Annual

Coupon Bond:

Price = abs(pv(YTM/2, N*2, Coupon/2, 1000))

4. Calculating Yield to

Maturity (YTM)

- YTM is

the interest rate that sets present value of cash flows = current price.

Excel/Calculator

formulas:

- Annual:

=rate(n, coupon, -price, 1000) - Semi-Annual:

=rate(n*2, coupon/2, -price, 1000)*2

5. Current Yield

Formula:

Current Yield = Annual Coupon ÷ Market

Price

Example:

- $50

coupon bond trading at $950 →

50 ÷ 950 = 5.26%

6. Zero-Coupon Bonds

- Coupon = 0, trades

at deep discount.

- Treated

as semi-annual for formulas.

- Only pays

$1,000 at maturity.

Chapter 8 Stock Valuation

· ppt

· Quiz

Part I Dividend payout and

Stock Valuation

Companies that have consistently increased

their dividends over the past 30 years

|

Company |

Ticker |

Sector |

Beta |

Current Quarterly Dividend |

Annual Dividend |

Years of Consecutive Increases |

Recent Increase (%) |

|

Johnson & Johnson |

JNJ |

Health Care |

0.56 |

$1.24 |

$4.96 |

62 |

4.2% (2024) |

|

Coca-Cola |

KO |

Consumer Staples |

0.59 |

$0.51 |

$2.04 |

63 |

5.2% (2025) |

|

Procter & Gamble |

PG |

Consumer Staples |

0.42 |

$1.01 |

$4.03 |

68 |

7% (2024) |

|

PepsiCo |

PEP |

Consumer Staples |

0.55 |

$1.36 |

$5.42 |

51 |

7% (2025) |

|

3M |

MMM |

Industrials |

0.95 |

$1.51 |

$6.04 |

65 |

0.7% (2024) |

|

Lowe’s |

LOW |

Consumer Discretionary |

1.09 |

$1.15 |

$4.60 |

60 |

5% (2024) |

|

Colgate-Palmolive |

CL |

Consumer Staples |

0.6 |

$0.50 |

$2.00 |

62 |

4.2% (2024) |

|

Hormel Foods |

HRL |

Consumer Staples |

0.41 |

$0.29 |

$1.16 |

59 |

2.7% (2025) |

|

Illinois Tool Works |

ITW |

Industrials |

1.12 |

$1.50 |

$6.00 |

50+ |

7% (2024) |

|

AbbVie |

ABBV |

Health Care |

0.56 |

$1.64 |

$6.56 |

10 (post spin-off) |

5.8% (2025) |

Companies with Near-Fixed Dividend Growth

|

Company |

Ticker |

Sector |

Quarterly Dividend (USD) |

Annual Dividend (USD) |

Recent Increase (%) |

Dividend Yield (%) |

Dividend History Link |

|

Microsoft |

MSFT |

Technology |

0.83 |

3.32 |

10 |

0.92 |

https://www.microsoft.com/en-us/Investor/dividendhistory.aspx |

|

Visa |

V |

Financial Services |

0.59 |

2.36 |

13 |

0.76 |

https://investor.visa.com/financial-information/stock-info/default.aspx |

|

McDonald's |

MCD |

Consumer Discretionary |

1.77 |

7.08 |

6 |

2.31 |

https://corporate.mcdonalds.com/corpmcd/investors/stock-information/dividends.html |

|

PepsiCo |

PEP |

Consumer Staples |

1.355 |

5.42 |

5 |

3.93 |

https://www.pepsico.com/investors/stock-information/dividends |

|

Waste Management |

WM |

Industrials |

0.825 |

3.3 |

10 |

1.56 |

Large-cap and well-known smaller companies that haven't

paid dividends in the past decade:

|

Company |

Ticker |

Sector |

Stock Price (USD) |

Beta |

Dividend Paid (Past 10 Years) |

Reason for Not Paying Dividends |

Buy Recommendation |

|

Amazon |

AMZN |

Consumer Discretionary |

175.26 |

1.39 |

No |

Reinvests in logistics, AWS, and growth initiatives |

Buy for long-term growth |

|

Alphabet (Google) |

GOOGL |

Communication Services |

155.2 |

1.06 |

No |

Reinvests in AI, cloud, YouTube, and search technologies |

Buy for AI/cloud exposure |

|

Meta Platforms (Facebook) |

META |

Communication Services |

488.1 |

1.21 |

No |

Focus on innovation and acquisitions; reinvests in VR, AI |

Buy cautiously; growth with volatility |

|

Tesla |

TSLA |

Consumer Discretionary |

168.38 |

2.19 |

No |

Capital goes into production, R&D, and expansion |

Buy only if comfortable with risk |

|

Berkshire Hathaway |

BRK.A / BRK.B |

Financials |

626185 |

0.92 |

No |

Prefers reinvestment; Buffett's philosophy is against

dividends |

Hold; slow but safe compounder |

|

Netflix |

NFLX |

Communication Services |

595.98 |

1.26 |

No |

Spends on original content and global expansion |

Buy for content/streaming growth |

|

Shopify |

SHOP |

Technology |

77.65 |

1.87 |

No |

Focus on reinvestment and expansion of e-commerce tools |

Buy for aggressive tech exposure |

|

Uber Technologies |

UBER |

Technology |

75.1 |

1.58 |

No |

Reinvests heavily in rideshare, freight, and autonomous tech |

Buy if bullish on mobility and AI |

|

Roku |

ROKU |

Communication Services |

63.43 |

1.83 |

No |

Spends on content deals, platform development, and growth |

Speculative buy; high risk/high reward |

|

Palantir Technologies |

PLTR |

Technology |

22.75 |

2.05 |

No |

Invests in AI, government contracts, and data platforms |

Buy for long-term AI and defense exposure |

|

Snowflake |

SNOW |

Technology |

188.9 |

0.9 |

No |

Focus on cloud data growth and scalability |

Buy cautiously; strong revenue, no profits |

|

Twilio |

TWLO |

Technology |

61.3 |

1.41 |

No |

Reinvests in developer tools and enterprise solutions |

Hold; uncertain path to profitability |

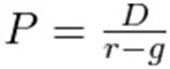

Key Insight: Dividend Growth Model (DGM), Or Gordon’s Growth Model

|

Section |

Details |

|

What Is It? |

A valuation tool that estimates a stock’s true worth

based on the idea that dividends will grow at a constant rate forever. |

|

Where Does It Come From? |

Created by Myron Gordon (1960s). Based on the Discounted

Cash Flow (DCF) concept — except it focuses only on dividends as

future cash flows. |

|

Formula (Equation) |

P0o=D1/(r−g)

(Refer to https://www.jufinance.com/dividend/,

Dividend growth model calculator) |

|

Where: |

|

|

• Po: today's stock price |

|

|

• D1=D0×(1+g) D1 is

next year’s dividend |

|

|

• r: required return |

|

|

• g: growth rate |

|

|

Used For? |

• Pricing dividend stocks |

|

• Checking if a stock is over- or under-valued |

|

|

• Estimating expected return if you know current price |

|

|

Works Best For... |

• Mature companies |

|

• Steady profits and consistent dividend growth |

|

|