FIN 509 Class Web Page, Fall 2 semester' 24

The

Syllabus Grade

Calculator Overall

Grade Calculator Risk Tolerance Test (FYI)

Weekly SCHEDULE, LINKS, FILES and Questions

|

Week |

Coverage, HW, Supplements -

Required |

Equations and

Assignments |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

·

Weekly Thursday class url on

blackboard collaborate: On Blackboard under “Join Course Room” Or from here https://us.bbcollab.com/guest/a070558d332041888dd5772fefccc290 ·

Weekly

Q&A Session on Blackboard URL (on Saturday from 7 – 8 PM): https://us.bbcollab.com/guest/7ee6be25e06546949517ebf89ef980b5 Class Schedule:

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Week 0 |

Market

Watch Game Use the information and directions

below to join the game. 1.

URL for

your game: 2. Password for this private game: havefun 3. Click on the 'Join Now' button to get

started. 4. If you are an existing MarketWatch member, login. If you are a new user,

follow the link for a Free account - it's

easy! 5. Follow the instructions and start trading! ·

How To Win The MarketWatch

Stock Market Game (youtube) based on https://www.finviz.com

·

A shorting strategy based on finviz.com (FYI) https://www.jufinance.com/game/short_selling.html |

Pre-class assignment: Set up marketwatch.com account and have

fun |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Week1,2 |

Chapter 5 Time value of money – Part

1 Chapter 5 In Class Exercise (Solution Word File)

The time value of money -

German Nande (youtube)

Concept of FV, PV,

Rate, Nper Calculation of FV, PV,

Rate, Nper Concept of interest

rate, compounding rate, discount rate

Present value – Future value – Demonstration

Game In class exercise (conceptual) Chapter 6 Time Value of Money – Part

2 Chapter 6 In Class Exercise (Chapter 6 In Class Exercise

Solution Word File) Concept of PMT, NPV Calculation of FV, PV,

Rate, Nper, PMT, NPV, NFV Concept of EAR, APR Calculation of EAR,

APR First Discussion Board Assignment (post your writing on blackboard under

discussion folder):

Market Watch Game

Let's start trading in the stock market!

Please join a game and report back on your experience. Directions 1.

URL for your game: 2.

Password for this private game: havefun. 3.

Click on the Join Now button to get started. 4.

Register for a new account with your email address or sign in if

you already have an account.

1.

Why did you choose the stock? How much money did you think you would

make? Please explain. 2.

Did you make money or lose money off of your chosen stock? Which

factors contributed to that? 3.

What did you learn from this experience and how will it affect your

choices in real life when choosing stocks? Instructions ·

Responses should be 100 to 250 words in length and should answer

all three prompts ·

Optional: reply to one of your peers with meaningful,

thought-provoking responses ·

Due by 7/11/2024 at 11:59

p.m. ET HOMEWORK of Chapters 5

and 6 (due by 11/3 ) 1. The Thailand

Co. is considering the purchase of some new equipment. The quote consists of

a quarterly payment of $4,740 for 10 years at 6.5 percent interest. What is

the purchase price of the equipment? ($138,617.88) 2. The condominium

at the beach that you want to buy costs $249,500. You plan to make a cash

down payment of 20 percent and finance the balance over 10 years at 6.75

percent. What will be the amount of your monthly mortgage payment? ($2,291.89) 4. Shannon wants

to have $10,000 in an investment account three years from now. The account

will pay 0.4 percent interest per month. If Shannon saves money every month,

starting one month from now, how much will she have to save each month?

($258.81)

(Hint: Bridget’s is an annuity due, so abs(fv(8%/12, 10*12, 150, 0,

1)) --- type =1; Jordan’s is an ordinary annuity, so abs(fv(8%/12, 10*12, 175, 0) --- type =0, or omitted. There is a

mistake in the help video for this question. Sorry for the mistake.) 14. What is the

future value of weekly payments of $25 for six years at 10 percent? ($10,673.90) 15. At the end of

this month, Bryan will start saving $80 a month for retirement through his

company's retirement plan. His employer will contribute an additional $.25

for every $1.00 that Bryan saves. If he is employed by this firm for 25 more

years and earns an average of 11 percent on his retirement savings, how much

will Bryan have in his retirement account 25 years from

now? ($157,613.33) 16. Sky

Investments offers an annuity due with semi-annual payments for 10 years at 7

percent interest. The annuity costs $90,000 today. What is the amount of each

annuity payment? ($6,118.35) 17. Mr. Jones

just won a lottery prize that will pay him $5,000 a year for thirty years. He

will receive the first payment today. If Mr. Jones can earn 5.5 percent on

his money, what are his winnings worth to him today? ($76,665.51) 18. You want to

save $75 a month for the next 15 years and hope to earn an average rate of

return of 14 percent. How much more will you have at the end of the 15 years

if you invest your money at the beginning of each month rather than the end

of each month? ($530.06) 19. What is the

effective annual rate of 10.5 percent compounded

semi-annually? (10.78%) 22. What is the

effective annual rate of 12.75 percent compounded daily? (13.60 percent) 23. Your

grandparents loaned you money at 0.5 percent interest per month. The APR on

this loan is _____ percent and the EAR is _____ percent. (6.00; 6.17) FYI only: help for homework Part 1(Qs

1-2) Part 2(Qs

4-8) Part 3(Qs 9-12) Part 4(Qs

13-16) Part 5(Qs

17-20) Part 6(Qs 21-24) (Q13: Bridget’s is an annuity

due, so abs(fv(8%/12, 10*12, 150, 0, 1)) --- type =1; Jordan’s is an ordinary

annuity, so abs(fv(8%/12, 10*12, 175, 0) --- type =0, or omitted. There is a mistake in the help

video for this question. Sorry for the mistake.) Quiz 1- Help Videos - Practice

Quiz |

Calculators Time

Value of Money Calculator © 2002 - 2019 by Mark A. Lane,

Ph.D. Math Formula FV = PV *(1+r)^n PV = FV /

((1+r)^n) N = ln(FV/PV)

/ ln(1+r) Rate = (FV/PV)1/n -1 Annuity: N

= ln(FV/C*r+1)/(ln(1+r)) Or N

= ln(1/(1-(PV/C)*r)))/ (ln(1+r))

EAR = (1+APR/m)^m-1 APR = (1+EAR)^(1/m)*m Excel Formulas To get FV, use FV

function. =abs(fv(rate, nper,

pmt, pv)) To get PV, use PV

function =

abs(pv(rate, nper, pmt, fv)) To get r, use

rate

function =

rate(nper, pmt, pv, -fv) To get number of

years,

use nper function = nper(rate, pmt, pv,

-fv) To get annuity

payment, use PMT

function = abs(pmt(rate, nper, pv,

-fv)) To get Effective

rate (EAR), use Effect

function =

effect(nominal_rate, npery) To get annual

percentage rate (APR), use nominal

function APR = nominal(effective rate, npery) To get NPV, use NPV function NPV = npv(rate, cf1, cf2,…) + cf0 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Week3 |

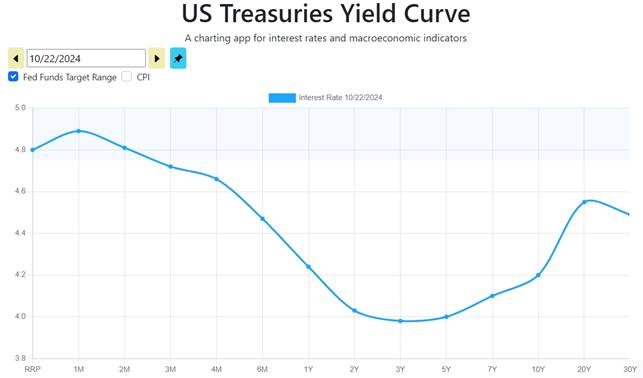

Chapter 7 Bond

Pricing Part I - Yield Curve Quiz Self-Produced

Video

https://www.ustreasuryyieldcurve.com/ US Treasuries Yield Curve - October 22, 2024 ·

Inverted Yield Curve: The curve starts high at

the short end, with a peak around 1-month maturity, and then declines,

hitting a low point at around 3 years. This is indicative of an inverted

yield curve, which often signals an impending

economic recession. ·

Steepening Beyond 10 Years: After the 10-year mark,

the curve starts to rise again, indicating investors expect higher returns

for longer maturities, possibly due to anticipated future inflation or uncertainty.

Or at https://www.gurufocus.com/yield_curve.php Current Treasury Yield Curve vs. prior years’

Summary: · Inflation:

·

Stock Market:

·

Economic Growth:

Part II – Bond Definition How

Bonds Work (video) For

discussion: https://jufinance.com/risk_tolerance.html

· Among the aforementioned bonds, do you

have a preference? If so, what factors influence your choice? Outlook for Investing in Bonds in

2024 After starting the year recommending that investors focus on

the middle of the yield curve, we began to advise investors to lengthen their

duration in our midyear bond

market update. According to our forecasts, we continue to

think investors will be best served in longer-duration bonds

and locking in the currently high interest rates. https://www.morningstar.com/markets/where-invest-bonds-2024 Where can you find bond information? · All types of bonds: https://www.finra.org/finra-data/fixed-income · Treasury Bond Auction and Market information http://www.treasurydirect.gov/ Are bonds Risky? Self-produced video Quiz Bond risk – credit risk (video)

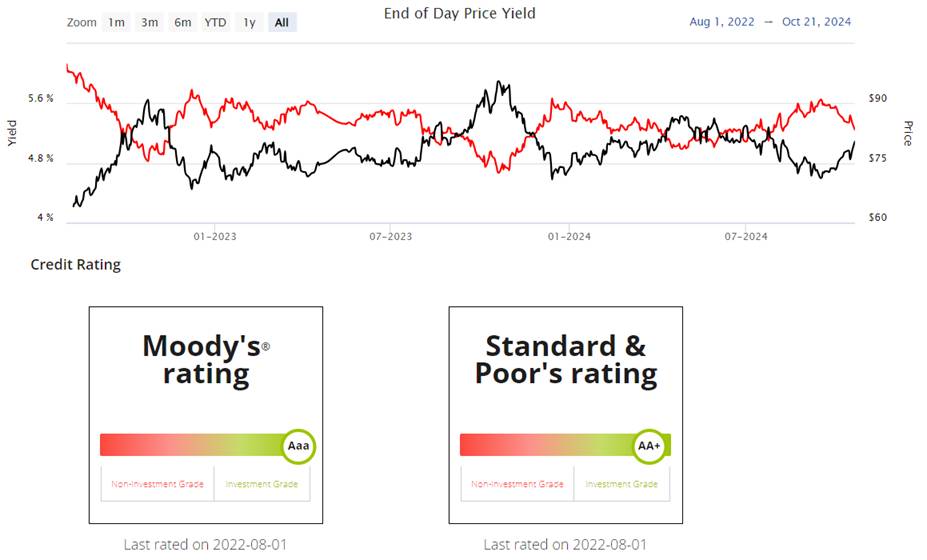

The above graph shows the cash flow of a five year 5% coupon bond.

The bond has a duration of 4.49 years.

|

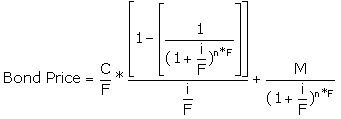

Bond Pricing Formula (FYI)

Bond Pricing Excel Formula Summary of

bond pricing excel functions To calculate bond price (annual coupon bond): Price=abs(pv(yield

to maturity, years left to maturity, coupon rate*1000, 1000) To calculate yield to maturity (annual coupon bond):: Yield

to maturity = rate(years left to maturity, coupon rate *1000, -price, 1000) To calculate bond price (semi-annual coupon bond): Price=abs(pv(yield

to maturity/2, years left to maturity*2, coupon rate*1000/2,

1000) To calculate yield to maturity (semi-annual coupon

bond): Yield

to maturity = rate(years left to maturity*2, coupon rate *1000/2,

-price, 1000)*2 To calculate number of years left(annual coupon bond) Number

of years =nper(yield to maturity, coupon rate*1000, -price, 1000) To calculate number of years left(semi-annual coupon bond) Number

of years =nper(yield to maturity/2, coupon rate*1000/2, -price,

1000)/2 To calculate coupon (annual coupon bond) Coupon

= pmt(yield to maturity, number of years left, -price, 1000) Coupon

rate = coupon / 1000 To calculate coupon (semi-annual coupon bond) Coupon

= pmt(yield to maturity/2, number of years left*2, -price, 1000)*2 Coupon

rate = coupon / 1000 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Week 4 |

Chapter 8 Stock

Valuation Part

I Dividend payout and Stock Valuation For class

discussion: · Why can we

use dividend to estimate a firm’s intrinsic value? · Are

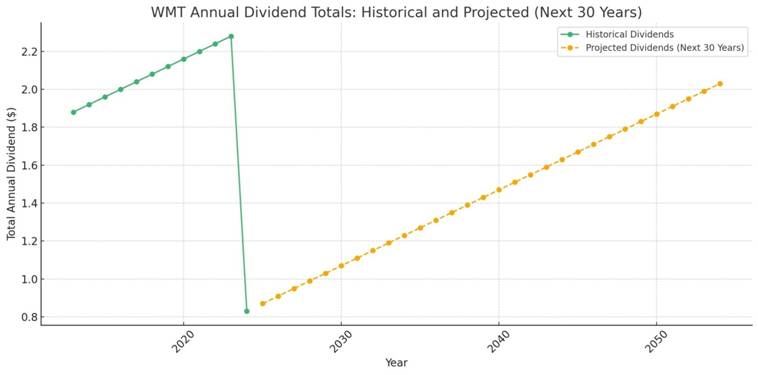

future dividends predictable? Refer to the following table for WMT’s dividend history Wal-Mart Dividend History https://www.macrotrends.net/stocks/charts/WMT/walmart/dividend-yield-history

WMT Dividend History

https://www.nasdaq.com/market-activity/stocks/wmt/dividend-history Walmart Inc. Common Stock (WMT) Dividend

History

·

Ex-Dividend Date08/16/2024 ·

Dividend Yield1.01% ·

Annual Dividend$0.83 ·

P/E Ratio13.72

An Analysis based on Walmart's (WMT) Dividend Payout

Record from 2020 to 2024: ·

Annual Payouts and Trends:

· Recent Dividend

Leveling:

· Prospects and Stability:

https://www.nasdaq.com/market-activity/stocks/wmt/dividend-history

P₀ = Σ [Dₜ / (1 + r)ᵗ]

from t=1 to ∞ where:

Calculating

the present value of dividends, especially when assuming they extend to

infinity, can be challenging. To simplify, we can assume that dividends grow at a constant rate. Additionally,

we can use the discount rate 'r,' which is based on the Beta and Capital

Asset Pricing Model (CAPM) discussed in Chapter 13. By incorporating these

assumptions, we can streamline the calculation process for determining the

present value of dividends. For dividends that grow at a constant

rate, the Net Present Value (NPV) of dividends can be calculated as: P₀ = D₁ / (r -

g) where:

https://www.nasdaq.com/market-activity/stocks/wmt

What information does each item in the table convey or

represent? From

finviz.com https://finviz.com/quote.ashx?t=WMT

Part II: Constant Dividend

Growth-Dividend growth model Calculate

stock prices 1) Given next dividends and price Po= Po= Po= Po= …… where:

Refer to http://www.calculatinginvestor.com/2011/05/18/gordon-growth-model/ · Now let’s apply this Dividend

growth model in problem solving. Constant dividend

growth model calculator (www.jufinance.com/stock) Equations 1. Present

Value (P₀)

Formulas:

P₀ = D₁

/ (r - g) or P₀ = D₀

* (1 + g) / (r - g)

2. Required Rate of Return (r):

r = D₁ / P₀

+ g = D₀ * (1 + g) / P₀

+ g

3. Growth Rate (g):

g = r - D₁ / P₀

= r - D₀ * (1 + g) / P₀

4. Dividend Formulas (D₁ and D₀):

D₁ = P₀

* (r - g) and D₀ = P₀

* (r - g) / (1 + g) 5. Capital Gain Yield:

Capital Gain Yield = g = (P₁ - P₀) / P₀

P₁ = D₂

/ (r - g) 6. Dividend Yield:

Dividend Yield = r - g = D₁ / P₀ = D₀ * (1 + g) / P₀ 7. Future Dividends (D₁, D₂, D₃, …):

D₁ = D₀

* (1 + g), D₂ = D₁

* (1 + g), D₃ = D₂

* (1 + g), … Exercise: 1.

Consider the valuation of a common stock that

paid $1.00 dividend at the end of the last year and is expected to pay a cash

dividend in the future. Dividends are expected to grow at 10% and the

investors required rate of return is 17%. How much is the price? How much is

the dividend yield? Capital gain yield? 2. The

current market price of stock is $90 and the stock pays dividend of $3 (D1)

with a growth rate of 5%. What is the return of this stock? How much is the

dividend yield? Capital gain yield? Part III: Non-Constant Dividend

Growth Calculate

stock prices 1) Given next dividends and price Po= Po= Po= Po= …… Non-constant

dividend growth model Equations 1.

Market Price in Year (Pₙ):

When dividends start to grow at a constant rate from year : Pₙ = Dₙ₊₁ / (r - g) = Dₙ * (1 + g) / (r - g) where:

2.

Present Value in Year 0 (P₀):

The present value P0 of all future dividends

up to year is: P₀ = NPV(r, D₁, D₂, …, Dₙ + Pₙ) Or, equivalently: P₀ = D₁ / (1 + r) + D₂ / (1 +

r)² + … + (Dₙ

+ Pₙ) / (1 + r)ⁿ Calculator: Non-Constant Dividend Growth Calculator https://www.jufinance.com/dcf/ In class exercise for

non-constant dividend growth model 1.

You expect

AAA Corporation to generate the following free cash flows over the next five

years:

Since year 6, you estimate that AAA's free cash flows will

grow at 6% per year. WACC of AAA = 15% · Calculate the enterprise value for DM Corporation. · Assume that AAA has $500 million debt and 14 million shares

outstanding, calculate its stock price. Answer:

2. AAA pays no dividend

currently. However, you expect it pay an annual dividend of $0.56/share 2

years from now with a growth rate of 4% per year thereafter. Its equity cost

= 12%, then its stock price=? Answer:

Do=0 D1=0 D2=0.56 g=4%

after year 2 è

P2 = D3/(r-g), D3=D2*(1+4%) è

P2 = 0.56*(1+4%)/(12%-4%) = 7.28 r=12% Po=? Po =

NPV(12%, D1, D2+P2), D2 = 0.56, P2=7.28. SO Po = NPV(12%, 0,0.56+7.28) =

6.25 (Note: for non-constant growth

model, calculate price when dividends start to grow at the constant rate.

Then use NPV function using dividends in previous years, last dividend plus

price. Or use calculator at https://www.jufinance.com/dcf/

) 3. Required return =12%.

Do = $1.00, and the dividend will grow by 30% per year for the next 4

years. After t = 4, the dividend is

expected to grow at a constant rate of 6.34% per year forever. What is the stock price ($40)? Answer:

Do=1 D1 =

1*(1+30%) = 1.3 D2=

1.3*(1+30%) = 1.69 D3 =

1.69*(1+30%) = 2.197 D4 =

2.197*(1+30%) = 2.8561 D5 =

2.8561*(1+6.34%), g=6.34% P4 =

D5/(r-g) = 2.8561*(1+6.34%) /(12% - 6.34%) Po = NPV(12%, 1.3, 1.69, 2.197,

2.8561+2.8561*(1+6.34%)) /(12% - 6.34%)) = 40 Or use calculator at https://www.jufinance.com/dcf Part IV: How to pick stocks?

(FYI) ·

FINVIZ.com http://finviz.com/screener.ashx use screener

on finviz.com to narrow down your choices of stocks, such as PE<15,

PEG<1, ROE>30% ·

Mutual

Fund Selection Game https://www.jufinance.com/game/mutual_fund_selection.html ·

FYI ~ Step-by-Step Guide for

Screening Mutual Funds:

1. Open the Mutual Fund

Screener:

2. Choose Basic Search

Criteria:

Key

Criteria to Focus On:

3. Set Up a Simple Screen:

Step-by-Step Filters for the screener:

4. Run the Search:

5. Analyze the Results:

After you run the screen, a

list of funds will appear. Here's how to interpret the most important columns:

6. Key Points:

Example:

Let’s say you want to find a low-cost,

well-rated balanced fund:

Now, click Search,

and the results will show a list of funds that match this criteria. 7. Choosing a Fund:

After the search, click on a

fund’s name for more detailed information. You’ll see details like:

Additional Tips:

· Start

Simple: Focus on categories and ratings to avoid getting

overwhelmed by too many options. · Expense

Ratio: Always look at the fees! They can significantly impact

long-term returns. · Performance:

A fund’s historical performance isn’t

a guarantee of future returns, but it’s a useful

indicator. Part V: Behavior Finance (FYI) Understanding

behavioral finance is essential because it explains how psychological biases

and emotions influence investors' decisions, often leading to irrational market

behavior. By recognizing these tendencies, investors and analysts can make

more informed choices, avoid common pitfalls, and better anticipate market

trends driven by human behavior. Anchoring Game Self-produced Video • Test

yourself first: A

stock price jumps to $40 from $20 but it suddenly dropped back to $20. Shall

you buy the stock or not? • The

concept of anchoring draws on the tendency to attach or "anchor"

our thoughts to a reference point - even though it may have no logical

relevance to the decision at hand. • Avoiding Anchoring – Be

especially careful about which figures you use to evaluate a stock's

potential. – Don't

base decisions on benchmarks – Evaluate

each company from a variety of perspectives to derive the truest picture of

the investment landscape. Mental

Accounting Self-produced Video • Test

yourself – Shall

you payoff your credit card debt or start saving for a vocation? – How

do you spend your tax refund? • Mental

Accounting refers to the tendency for people to separate their money into

separate accounts based on a variety of subjective criteria, like the source

of the money and intent for each account. Example: People

have a special "money jar" set aside for a vacation while still

carrying credit card debt. Confirmation Bias Self-produced video • Confirmation

bias: First impression can be hard to shake – people

selectively filter information that supports their opinion – People

ignore the rest opinions. – In

investing, people look for information that supports original idea • Generate

faulty decision making because of the bias Example: investor finds all

sorts of green flags about the investment (such as growing cash flow or a low

debt/equity ratio), while glossing over financially disastrous red flags,

such as loss of critical customers or dwindling markets. Herding Game Self-produced video – Example:

Dotcom herd – The

tendency for individuals to mimic the actions of a larger group. • Social

pressure of conformity is one of the causes. – This

is because most people are very sociable and have a natural desire to be

accepted by a group • The

second reason is the common rationale that a large group could not be

wrong. – This

is especially prevalent when an individual has very little experience. Overconfidence: • Confidence

implies realistically trusting in one's abilities • Overconfidence

implies an overly optimistic assessment of one's knowledge or control over a

situation. Disposition

effect Game Self-produced Video – which

is the tendency for investors to hold on to losing stocks for too long and

sell winning stocks too soon. » The

most logical course of action would be to hold on to winning stocks to

further gains and to sell losing stocks to prevent escalating losses. » investors

are willing to assume a higher level of risk in order to avoid the negative

utility of a prospective loss. » Unfortunately,

many of the losing stocks never recover, and the losses incurred continued to

mount . Avoiding the Disposition Effect • When you have a

choice of thinking of one large gain or a number of smaller gains (such as

finding $100 versus finding a $50 bill from two places), thinking of the

latter can maximize the amount of positive utility. • When you have a

choice of thinking of one large loss or a number of smaller losses (losing

$100 versus losing $50 twice), think of one large loss would create less

negative utility. • When you can

think of one large gain with a smaller loss or a situation where you net the

two to create a smaller gain ($100 and -$55, versus +$45), you would receive

more positive utility from the smaller gain. • When you can

think of one large loss with a smaller gain or a smaller loss (-$100 and

+$55, versus -$45), try to separate losses from gains. Gambler’s

fallacy Game Self-produced Video – An

individual erroneously believes that the onset of a certain random event is less

likely to happen following an event or a series of events. Example: • Example: – You

liquidate a position after it has gone up in several days. – You

hold on to a stock that has fallen in several days because you view further

declines as "improbable". • Avoiding

Gambler's Fallacy – Investors

should base decisions on fundamental or technical analysis before

determining what will happen. It is irrational to buy a

stock because you believe it is likely to reverse. 12 Cognitive Biases Explained - How to Think Better and More Logically

Removing Bias (video, FYI)

0:18 Anchoring Bias 1:22 Availability

Bias 2:22 Bandwagon Effect

3:09 Choice

Supportive Bias 3:50 Confirmation

Bias 4:30 Ostrich Bias 5:20 Outcome Bias 6:12 Overconfidence 6:52 Placebo Effect 7:44 Survivorship

Bias 8:32 Selective

Perception 9:08 Blindspot Bias Part VI: Practice (FYI) Play the stock market investment game. Make

investment decision and balance risk with rewards in the stock market at https://www.jufinance.com/game/investment/index.html

HOMEWORK (Due with final) 1. Northern

Gas recently paid a $2.80 annual dividend on its common stock. This dividend

increases at an average rate of 3.8 percent per year. The stock is currently

selling for $26.91 a share. What is the market rate of return? (14.60

percent) 5.

Investors of

Creamy Custard common stock earns 15% of return. It just paid a

dividend of $6.00 and dividends are expected to grow at a rate of 6%

indefinitely. What is expected price of Creamy Custard's stock? ($70.67) Homework Video of this

week Homework help video

(FYI) Quiz 3- Help Video Quiz 3

Practice Part I Part II Part III Part IV

|

P/E Ratio Summary by

industry (FYI) --- Thanks to Dr Damodaran Data Used: Multiple data services Date of Analysis: Data used is as of January 2021 Download as an excel file instead: http://www.stern.nyu.edu/~adamodar/pc/datasets/pedata.xls For global datasets: http://www.stern.nyu.edu/~adamodar/New_Home_Page/data.html

Details

about how to derive the model mathematically (FYI) The Gordon growth model is a simple discounted cash flow (DCF)

model which can be used to value a stock, mutual fund, or even the entire

stock market. The model is named after Myron Gordon who first published

the model in 1959. The Gordon model assumes that a financial security

pays a periodic dividend (D) which grows at a constant rate

(g). These growing dividend payments are assumed to continue forever.

The future dividend payments are discounted at the required rate of return

(r) to find the price (P) for the stock or fund. Under these simple assumptions, the price of the

security is given by this equation:

In this equation, I’ve used the “0” subscript

on the price (P) and the “1” subscript on the dividend (D) to

indicate that the price is calculated at time zero and the dividend is the

expected dividend at the end of period one. However, the equation is

commonly written with these subscripts omitted. Obviously, the assumptions built into this

model are overly simplistic for many real-world valuation problems. Many

companies pay no dividends, and, for those that do, we may expect

changing payout ratios or growth rates as the business matures. Despite

these limitations, I believe spending some time experimenting with the

Gordon model can help develop intuition about the relationship between

valuation and return. Deriving the Gordon Growth Model Equation

The Gordon growth model calculates the present value of

the security by summing an infinite series of discounted dividend payments

which follows the pattern shown here:

Multiplying both sides of the previous equation by

(1+g)/(1+r) gives:

We can then subtract the second equation from the first

equation to get:

Rearranging and simplifying:

Finally,

we can simplify further to get the Gordon growth model equation |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 9 Capital Budgeting Self-produced video explaining

approaches for capital budgeting

1. NPV Excel syntax Syntax NPV(rate,value1,value2, ...) Rate is the rate of discount over

the length of one period. Value1, value2,

... are 1 to

29 arguments representing the payments and income. · Value1, value2, ... must be equally spaced in

time and occur at the end of each period. NPV uses the

order of value1, value2, ... to interpret the order of cash flows.

Be sure to enter your payment and income values in the correct sequence. 2. IRR Excel syntax Syntax IRR(values, guess) Values is an array or a reference to cells

that contain numbers for which you want to calculate the internal rate of

return. Guess is a number that you guess is

close to the result of IRR.

Or, PI =

NPV / CFo +1 Profitable

index (PI) =1 + NPV / absolute value of CFo 3. MIRR( values, finance_rate, reinvest_rate ) Where

the function arguments are as follows:

Modified Rate of Return:

Definition & Example (video)

https://study.com/academy/lesson/modified-rate-of-return-definition-example.html NPV, IRR, Payback Period calculator I NPV, IRR, Payback Period calculator II

Excel Template - NPV, IRR, MIRR, PI, Payback,

Discounted payback NPV

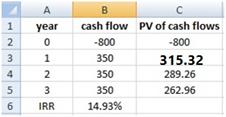

Profile in Excel Demonstration (Video, FYI) In class exercise Part I: Single project 1.

How much is MIRR? IRR? Payback period?

Discounted payback period? NPV? WACC: 11.00% Year 0 1 2 3 Cash

flows -$800 $350 $350 $350 Answer: 1)

NPV: NPV = -800 + 350/(1+11%) +

350/(1+11%)2 + 350/(1+11%)3 = 55.30 Or in excel: = npv(11%, 350, 350, 350)-800 = 55.30 2)

IRR:

So NPV = 0 = -800 +

350/(1+IRR) + 350/(1+IRR)2 + 350/(1+IRR)3 , use Solver,

can get IRR = 14.93% Or in excel:

3)

PI: profitable index

SO, PI= (350/(1+11%) + 350/(1+11%)2 + 350/(1+11%)3

) / 800 = 1.069 Or PI = NPV/800 + 1 = 55.30/800 + 1 = 1.069 4)

Payback period:

A portion of the third year = (800-350-350)/350 = 100/350 =

0.2857 So it takes 2 + 0.2857 = 2.2857 years to pay off the debt of

$800. 5)

Discounted payback period:

Note: All the cash flows in the above equation should be the

present values. A portion of the third year = (800-318.18-289.26)/262.96 =

0.72 So it takes 2 + 0.72 = 2.72 years to pay off the debt of $800.

A portion of the third year = (800-315.32-289.26)/262.96 = 0.72 So it takes 2 + 0.72 = 2.72 years to pay off the debt of $800. Or use the calculator at https://www.jufinance.com/capital/ Part

II: Multi-Projects 1.

Projects S and L, whose cash flows are

shown below. These projects are

mutually exclusive, equally risky, and not repeatable. The CEO believes the IRR is the best

selection criterion, while the CFO advocates the NPV. If the decision is made by choosing the

project with the higher IRR rather than the one with the higher NPV, how

much, if any, value will be forgone, i.e., what's the chosen NPV versus the

maximum possible NPV? Note that (1) “true value” is measured by NPV,

and (2) under some conditions the choice of IRR vs. NPV will have no effect

on the value gained or lost. WACC: 7.50% Year 0 1 2 3 4 CFS -$1,100 $550 $600 $100 $100 CFL -$2,700 $650 $725 $800 $1,400 Answer:

If the required rate of return is 10%. Which

project shall you choose? 1) How

much is the cross over rate? (answer: 11.8%) 2) How

is your decision if the required rate of return is 13%? (answer: NPV of

B>NPV of A) · Rule for mutually exclusive projects: (answer:

Choose B) · What about the two projects are

independent? (answer: Choose both) Solution:

Part III More on IRR – (non-conventional cash flow) Suppose an investment will

cost $90,000 initially and will generate the following cash flows: – Year 1: 132,000 – Year 2: 100,000 – Year 3: -150,000 The required return is 15%.

Should we accept or reject the project? 1) How does the

NPV profile look like? (Answer: Inverted NPV profile) 2) IRR1= 10.11% --

answer 3) IRR2= 42.66% --

answer Solution:

Summary

HOMEWORK(Due with final)

Year Cash

flows 1 $8,000 2 4,000 3 3,000 4 5,000 5 10,000 1) How much is the payback

period (approach one)? ---- 4 years 2) If the firm has a 10%

required rate of return. How much is NPV (approach 2)?-- $2456.74 3) If the firm has a 10%

required rate of return. How much is IRR (approach 3)? ---- 14.55% 4) If the firm has a 10%

required rate of return. How much is PI (approach 4)? ---- 1.12 Question 2: Project with an initial cash

outlay of $60,000 with following free cash flows for 5 years. Year FCF Initial

outlay –60,000 1 25,000 2 24,000 3 13,000 4 12,000 5 11,000 The firm has a 15% required

rate of return. Calculate payback period, NPV,

IRR and PI. Analyze your results. Question 3: Mutually Exclusive Projects 1) Consider the following

cash flows for one-year Project A and B, with required rates of return of

10%. You have limited capital and can invest in one but one project. Which

one? § Initial Outlay: A = -$200; B = -$1,500 § Inflow: A

= $300; B = $1,900 2) Example: Consider two projects,

A and B, with initial outlay of $1,000, cost of capital of 10%, and following

cash flows in years 1, 2, and 3: A:

$100 $200 $2,000 B:

$650 $650 $650 Which project should you choose if they are mutually

exclusive? Independent? Crossover rate? (mutually exclusive: A’s NPV=758.83 >

B’s NPV = 616.45, so choose A; Independent, choose

all positive NPV, so choose both; Crossover rate = 21.01%. The calculator does not work. Use IRR

in Excel) Quiz 4- chapter 9 – (no

video prepared; Could use the calculator) Homework help videos (chapter 9) |

Simple

Rules’ for Running a Business

From the 20-page cellphone contract to the five-pound employee

handbook, even the simple things seem to be getting more complicated. Companies have been complicating things for themselves, too—analyzing hundreds of factors when making decisions, or

consulting reams of data to resolve every budget dilemma. But those

requirements might be wasting time and muddling priorities. So argues Donald Sull,

a lecturer at the Sloan School of Management at the Massachusetts Institute

of Technology who has also worked for McKinsey & Co. and Clayton, Dubilier & Rice LLC. In the book Simple

Rules: How to Thrive in a Complex World, out this week from Houghton

Mifflin Harcourt HMHC -1.36%,

he and Kathleen Eisenhardt of Stanford University claim that straightforward

guidelines lead to better results than complex formulas. Mr. Sull recently spoke with At Work about

what companies can do to simplify, and why five basic rules can beat a

50-item checklist. Edited excerpts: WSJ: Where, in the business context,

might “simple

rules” help

more than a complicated approach? Donald Sull: Well, a common decision that people face in organizations is

capital allocation. In many organizations, there will be thick procedure

books or algorithms–one company I worked with had an

algorithm that had almost 100 variables for every project. These are very

cumbersome approaches to making decisions and can waste time. Basically, any

decision about how to focus resources—either people

or money or attention—can benefit from simple rules. WSJ: Can you give an example of

how that simplification works in a company? Sull: There’s

a German company called Weima GmBH that makes shredders. At one point,

they were getting about 10,000 requests and could only fill about a thousand

because of technical capabilities, so they had this massive problem of

sorting out which of these proposals to pursue. They had a very detailed checklist with 40 or 50 items. People

had to gather data and if there were gray areas the proposal would go to

management. But because the data was hard to obtain and there were so many

different pieces, people didn’t always fill out the checklists completely. Then

management had to discuss a lot of these proposals personally because there

was incomplete data. So top management is spending a disproportionate amount

of time discussing this low-level stuff. Then Weima came up with guidelines that the

frontline sales force and engineers could use to quickly decide whether a

request fell in the “yes,” “no” or “maybe” category. They did it with five

rules only, stuff like “Weima had to

collect at least 70% of the price before the unit leaves the factory.” After that, only the “maybes” were sent to management. This dramatically

decreased the amount of time management spend evaluating these projects–that time was decreased by almost a factor of 10. Or, take Frontier Dental Laboratories in Canada. They were

working with a sales force of two covering the entire North American market.

Limiting their sales guidelines to a few factors that made someone likely to

be receptive to Frontier—stuff like “dentists

who have their own practice” and “dentists

with a website”—helped focus their efforts and

increase sales 42% in a declining market. WSJ: Weima used five factors—is

that the optimal number? And how do you choose which rules to follow? Sull: You should have four to six

rules. Any more than that, you’ll spend too much time trying to follow

everything perfectly. The entire reason simple rules help is because they

force you to prioritize the goals that matter. They’re

easy to remember, they don’t confuse or stress you,

they save time. They should be tailored to your specific goals, so you choose

the rules based on what exactly you’re trying to

achieve. And you should of course talk to others. Get information from

different sources, and ask them for the top things that worked for them. But

focus on whether what will work for you and your circumstances. WSJ: Is there a business leader

you can point to who has embraced the “simple rules” guideline? Donald Sull: Let’s look at when Alex Behring took

over America

Latina Logistica SARUMO3.BR +1.59%,

the Brazilian railway and logistics company. With a budget of $15 million,

how do you choose among $200 million of investment requests, all of which are

valid? The textbook business-school answer to this is that you run the

NPV (net present value) test on each project and rank-order them by NPV. Alex

Behring knows this. He was at the top of the class at Harvard Business School. But instead Similarly, the global-health arm of the Gates Foundation gets

many, many funding requests. But since they know that their goal is to have

the most impact worldwide, they focus on projects in developing countries

because that’s where the money will stretch farther. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

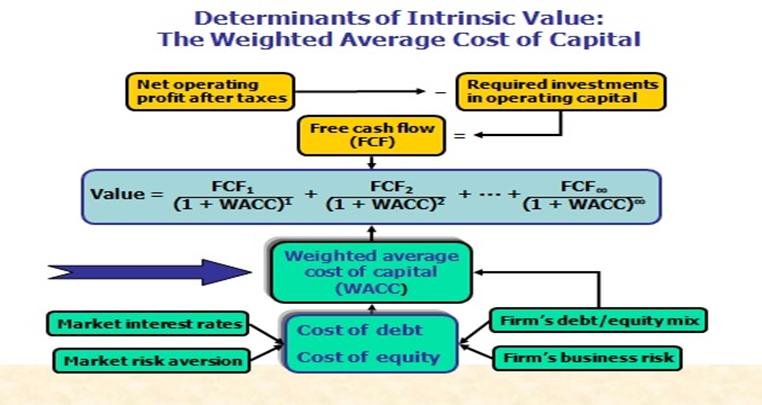

Week 4 - Chapter 14 Cost of Capital Self-Produced

Video Explaining WACC and WACC Strategies for Different Industries

One option (if beta is given, refer to chapter 13)

Another option (if dividend is given):

WACC Formula

WACC calculator (annual

coupon bond) (www.jufinance.com/wacc)

WACC calculator (semi-annual coupon bond) (www.jufinance.com/wacc_1)

WACC Calculator help

videos FYI

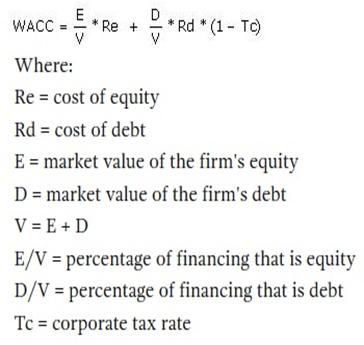

Weighted Average Cost of Capital (WACC) WACC

is the discount rate used to evaluate project values. Formula:

WACC = (Wd * Cost of Debt) + (We * Cost of Equity) Where:

Cost of Debt Formula: Definitions:

Cost of Equity Two

methods are available depending on the information provided:

Definitions:

Definitions:

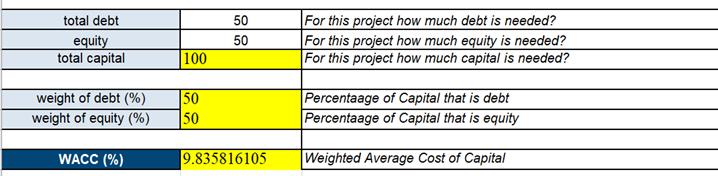

In Class Exercise: A firm borrows money from bond market. The price they paid is $950 for the bond with 5% coupon rate and 10 years to mature. Flotation cost is $40. For the new stocks, the expected dividend is $2 with a growth rate of 10% and price of $40. The flotation cost is $4. The company raises capital in equal proportions i.e. 50% debt and 50% equity (such as total $1m raised and half million is from debt market and the other half million is from stock market). Tax rate 34%. What is WACC (weighted average cost of capital, cost of capital)? (Answer: 9.84%) 1) Why does the firm raise capital from the financial market? Is there of any costs of doing so? What do you think? 2) What is cost of debt? (Kd = rate(nper, coupon, -(price – flotation costs $)), 1000)*(1-tax rate)) 3) Cost of equity? (Ke = (D1/(Price – flotation costs $)) +g, or Ke = Rrf + Beta*MRP)) Why no tax adjustment like cost of debt? 4) WACC=Cost of capital = Percentage of Debt * cost of debt + percentage of stock * cost of stock = Wd*Kd + We* Ke Meaning: For a dollar raised in the capital market from debt holders and stockholders, the cost is WACC. Solution: Cost

of debt = rate(10, 50, -(950-40), 1000)*(1-34%) Cost

of/equity = 2/(40-4)+10% WACC

= 0.5*cost of debt + 0.5*cost of equity

https://www.jufinance.com/wacc/ No

homework for chapter 14 |

(both annual and

semi-annual) WACC calculator (annual coupon bond) WACC calculator (semi-annual coupon

bond) (www.jufinance.com/wacc_1) Wal-Mart

Inc (NYSE:WMT) WACC %: 7.62%

As of 11/4/2024 As of today (2024-11-4), Walmart's

weighted average cost of capital is 7.62%. Walmart's ROIC % is 11.51% (calculated using TTM income

statement data). Walmart generates higher returns on investment than it costs

the company to raise the capital needed for that investment. It is earning

excess returns. A firm that expects to continue generating positive excess

returns on new investments in the future will see its value increase as

growth increases.https://www.gurufocus.com/term/wacc/WMT/WACC/Walmart%2BInc

Amazon.com

Inc (NAS:AMZN) WACC %:11.77% As of 11/4/2024 As of today (2024-11/4) Amazon.com's weighted average cost of capital is 11.77%. Amazon.com's ROIC % is 13.05% (calculated using TTM income statement data). Amazon.com generates higher returns on investment than it costs the company to raise the capital needed for that investment. It is earning excess returns. A firm that expects to continue generating positive excess returns on new investments in the future will see its value increase as growth increases. https://www.gurufocus.com/term/wacc/AMZN/WACC-Percentage/Amazon.com%20Inc Apple

Inc (NAS:AAPL) WACC %:11.17%

As of 11/4/2024 As of today (2024-11/4), Apple's

weighted average cost of capital is 11.17%. Apple's ROIC % is 31.92% (calculated

using TTM income statement data). Apple generates higher returns on

investment than it costs the company to raise the capital needed for that

investment. It is earning excess returns. A firm that expects to continue

generating positive excess returns on new investments in the future will see

its value increase as growth increases..https://www.gurufocus.com/term/wacc/AAPL/WACC/Apple%2Binc

Tesla WACC %: 15.32% As of 11/4/2024

As of today (2024-11-4), Tesla's weighted average cost of capital is 15.32%. Tesla's ROIC % is 18.67% (calculated using TTM income statement data). Tesla earns returns that do not match up to its cost of capital. It will destroy value as it grows. https://www.gurufocus.com/term/wacc/NAS:TSLA/WACC-/Tesla

NVIDIA (NAS:NVDA) WACC %: 18.89% As of 11/4/2024

As of today (2024-11/4), NVDIA's weighted average cost of capital is 18.89%. NVDIA's ROIC % is 162.59%. (calculated using TTM income statement data). Tesla earns returns that do not match up to its cost of capital. It will destroy value as it grows. https://www.gurufocus.com/term/wacc/NVDA/WACC-Percentage/NVDA

Cost of Capital by

Sector (US) Date of Analysis: Data used is as of January 2024 Download as an excel file instead: https://www.stern.nyu.edu/~adamodar/pc/datasets/wacc.xls For global datasets: https://www.stern.nyu.edu/~adamodar/New_Home_Page/data.html

http://people.stern.nyu.edu/adamodar/New_Home_Page/datafile/wacc.htm |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Week

6 - Chapter 13 Risk

and Return Equations (FYI): 1. Expected return and

standard deviation Given a probability distribution of

returns, the expected return can be calculated using the following equation:

where

https://www.zenwealth.com/businessfinanceonline/RR/ExpectedReturn.html Given an asset's expected return,

its variance can be calculated using the following equation:

where

The standard deviation is calculated

as the positive square root of the variance.

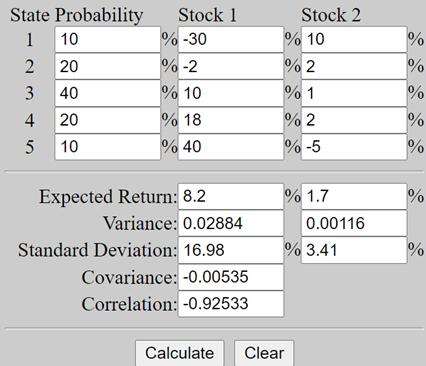

https://www.zenwealth.com/businessfinanceonline/RR/MeasuresOfRisk.html Exercise: Stock A has the following returns for various states of the

economy:

Stock A's expected return is?

Standard deviation? Solution:

· Expected return = 10%*(-30%)) + 20%*(-2%) + 40% *10% + 20%*18%

+ 10%*40% = 8.2% · Standard deviation = sqrt(10%*(-30%-8.2%)2 +

20%*(-2%-8.2%)2 +40%*(10%-8.2%)2 + 20%*(18%-8.2%)2

+10%*(40%-8.2%)2) = 16.98% Or, https://www.jufinance.com/return/

W1 and W2 are the percentage of each stock in the

portfolio.

Exercise: Stocks A and B have the following returns for various states of

the economy:

Solution: (or use calculator

at https://www.jufinance.com/return/) Stock 1: · Expected return = 10%*(-30%)) + 20%*(-2%) + 40%

*10% + 20%*18% + 10%*40% = 8.2% · Standard deviation = sqrt(10%*(-30%-8.2%)2

+ 20%*(-2%-8.2%)2 +40%*(10%-8.2%)2 + 20%*(18%-8.2%)2

+10%*(40%-8.2%)2) = 16.98% Stock 2: · Expected return = 10%*(10%)) + 20%*(2%) + 40% *1%

+ 20%*2% + 10%*(-5)% = 1.7% · Standard deviation = sqrt(10%*(10%-1.7%)2

+ 20%*(2%-1.7%)2 +40%*(1%-1.7%)2 + 20%*(2%-1.7%)2

+10%*((-5)%-1.7%)2) = 3.41% Covariance: · Covariance =

10%*(-30%-8.2%)*(10%-1.7%)+20%*(-2%-8.2%)*(2%-1.7%)+40%*(10%-8.2%)*(1%-1.7%)+20%*(18%-8.2%)*(2%-1.7%)+10%*(40%-8.2%)*((-5%)-1.7%)

= -0.54% Correlation: · Correlation = -0.54%/(16.98%* 3.41%) = -0.93

]3..

Historical returns Holding period return (HPR) =

(Selling price – Purchasing price + dividend)/ Purchasing price 4. CAPM (Capital Asset

Pricing Model) model · What is Beta? Where to find Beta?

Beta

is a measurement of a stock's price fluctuations, which is often called

volatility, and is used by investors to gauge how quickly a stock's price

will rise or fall. Because beta is calculated from past returns, it's not

considered as reliable a tool to forecast rises in stock prices, and it is

more commonly used by options traders. Beta compares the changes in a

company's stock returns against the returns of the market as a whole. Online

brokerages give investors extensive data on a stock's beta value, and some

free financial news websites also show current beta measurements. · What

Is the Capital Asset Pricing Model?

The Capital Asset Pricing Model (CAPM)

describes the relationship between systematic risk and expected

return for assets, particularly stocks. CAPM is widely used throughout

finance for pricing risky securities and generating expected returns

for assets given the risk of those assets and cost of capital. Ri = Rf + βi *( Rm -

Rf) ------ CAPM model · Ri =

Expected return of investment ·

Rf = Risk-free rate ·

βi = Beta of the investment ·

Rm = Expected return of market ·

(Rm - Rf)

= Market risk premium Investors expect to be compensated for risk and the time

value of money. The risk-free rate in the CAPM formula accounts for

the time value of money. The other components of the CAPM formula account for

the investor taking on additional risk. The beta of a potential investment is a

measure of how much risk the investment will add to a portfolio that looks

like the market. If a stock is riskier than the market, it will have a beta

greater than one. If a stock has a beta of less than one, the formula assumes

it will reduce the risk of a portfolio. A stock’s beta is then multiplied by

the market risk premium, which is the return expected from the market

above the risk-free rate. The risk-free rate is then added to the product of

the stock’s beta and the market risk premium.

The result should give an investor the required

return or discount rate they can use to find the value of an

asset. The goal of the CAPM formula is to evaluate whether a stock is

fairly valued when its risk and the time value of money are compared to its

expected return. For example, imagine an investor is

contemplating a stock worth $100 per share today that pays a 3% annual

dividend. The stock has a beta compared to the market of 1.3, which means it

is riskier than a market portfolio. Also, assume that the risk-free rate is

3% and this investor expects the market to rise in value by 8% per year. The expected return of the stock based on the CAPM formula is

9.5%. The expected return of the CAPM formula is used to discount

the expected dividends and capital appreciation of the stock over the

expected holding period. If the discounted value of those future cash flows

is equal to $100 then the CAPM formula indicates the stock is fairly valued

relative to risk. (https://www.investopedia.com/terms/c/capm.asp) · SML – Security Market Line

In Class Exercise (NVIDIA, WalMart, JP Morgan -

Monthly Stock

prices – prior 5 years) Here's how to pull monthly

stock data in Google Sheets for free

using the Step 1: Use

|

How

much does Amazon worth?” --- FYI only: Amazon.com Inc. (AMZN) https://www.stock-analysis-on.net/NASDAQ/Company/Amazoncom-Inc/DCF/Present-Value-of-FCFF

Present Value of Free Cash Flow to the Firm

(FCFF)

In discounted cash flow (DCF) valuation techniques the

value of the stock is estimated based upon present value of some measure of

cash flow. Free cash flow to the firm (FCFF) is generally described as cash

flows after direct costs and before any payments to capital suppliers.

Intrinsic Stock

Value (Valuation Summary)

Amazon.com Inc., free cash flow to the

firm (FCFF) forecast

1 Weighted Average

Cost of Capital (WACC)

Amazon.com Inc., cost of capital

1 USD $ in millions Equity (fair value) = No. shares of

common stock outstanding × Current share price Debt (fair value). See Details » 2 Required rate of return on equity is estimated by

using CAPM. See Details » Required rate of return on

debt. See Details » Required rate of return on debt

is after tax. Estimated (average) effective

income tax rate WACC = 16.17% FCFF Growth Rate

(g)

FCFF growth rate

(g) implied by PRAT model

Amazon.com Inc., PRAT model

2017 Calculations 2 Interest expense, after tax = Interest expense ×

(1 – EITR) 3 EBIT(1 – EITR) = Net income (loss) + Interest

expense, after tax 4 RR = [EBIT(1 – EITR) – Interest expense (after

tax) and dividends] ÷ EBIT(1 – EITR) 5 ROIC = 100 × EBIT(1 – EITR) ÷ Total capital 6 g = RR × ROIC FCFF growth rate

(g) forecast

Amazon.com Inc., H-model

where: Calculations g2 = g1 + (g5 – g1) × (2 – 1) ÷ (5 – 1) g3 = g1 + (g5 – g1) × (3 – 1) ÷ (5 – 1) g4 = g1 + (g5 – g1) × (4 – 1) ÷ (5 – 1) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Week7 part I |

Final Exam (will be posted on blackboard) Final prep video (on youtube) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Week 7 Part II |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

FYI – Develop a Stock

Data Fetcher in Google Sheets Step 1: Create a New

Google Sheet

Step 2: Set Up the

Google Apps Script

// Function to serve

the HTML file function doGet() { return HtmlService.createHtmlOutputFromFile('index'); } function fetchStockData(ticker, startDateStr) { var sheet = SpreadsheetApp.getActiveSpreadsheet().getActiveSheet(); // Clear previous data sheet.getRange("A1:F1000").clearContent(); // Set the header row for daily data sheet.getRange("A1").setValue("Date"); sheet.getRange("B1").setValue("Closing

Price"); sheet.getRange("C1").setValue("Stock Name"); // Fetch and display the stock name using GOOGLEFINANCE var stockNameFormula = `=GOOGLEFINANCE("${ticker}", "name")`; sheet.getRange("C2").setFormula(stockNameFormula); // Set up the formula to fetch daily data using

GOOGLEFINANCE var formula = `=GOOGLEFINANCE("${ticker}", "close", "${startDateStr}", TODAY(), "daily")`; sheet.getRange("A2").setFormula(formula); // Wait for the data to populate SpreadsheetApp.flush(); // Copy the daily data into an array var dataRange = sheet.getRange("A2:B1000").getValues(); var validData = dataRange.filter(row => row[0] && row[1]); // Remove empty rows and invalid data if (validData.length === 0) { return "No data

available. Please check the stock ticker and date range."; } // Set the header row for monthly data in columns

D, E, and F sheet.getRange("D1").setValue("Month"); sheet.getRange("E1").setValue("Closing

Price"); sheet.getRange("F1").setValue("Monthly

Return"); // Process data to calculate the last trading

day of each month var monthlyData = {}; validData.forEach(row => { var date = new Date(row[0]); var price = row[1]; var monthKey = `${date.getFullYear()}-${(date.getMonth() + 1).toString().padStart(2, '0')}`; // Keep updating to get the last price of the

month monthlyData[monthKey] = price; }); // Write the monthly data and calculate returns var previousPrice = null; var rowIndex = 2; for (var month in monthlyData) { var price = monthlyData[month]; sheet.getRange(rowIndex, 4).setValue(month); // Write month in column D sheet.getRange(rowIndex, 5).setValue(price); // Write price in column E if (previousPrice !== null) { var monthlyReturn = ((price - previousPrice) / previousPrice) * 100; sheet.getRange(rowIndex, 6).setValue(monthlyReturn.toFixed(2) + "%"); // Write return in column F } previousPrice = price; rowIndex++; } return "Data fetched and

returns calculated successfully!"; }

Step 3: Authorize and

Run the Script

Step 4: Create the

HTML File

1.

In the Apps Script editor, click on the 2.

Name the new file 3.

Paste the following HTML code into the <!DOCTYPE html> <html> <head> <base target="_top"> <title>Stock Data Fetcher</title> <style> body { font-family: Arial, sans-serif; margin: 20px; } h2 { color: #333; } label { display: block; margin-top: 10px; } input, button { margin-top: 5px; } .footer { margin-top: 20px; font-size: 12px; color: #666; text-align: center; } </style> </head> <body> <h2>Stock Data Fetcher</h2> <label for="ticker">Stock Ticker:</label> <input type="text" id="ticker" placeholder="e.g., AAPL, WMT" /><br> <label for="startDate">Start Date:</label> <input type="date" id="startDate" /><br> <button onclick="fetchData()">Fetch Data</button> <p id="status"></p> <!-- Button to open the Google Sheet --> <button onclick="openGoogleSheet()">Open Google Sheet</button> <script> function fetchData() { var ticker = document.getElementById('ticker').value; var startDate = document.getElementById('startDate').value; // Call the Apps Script function google.script.run.withSuccessHandler(function(response) {

document.getElementById('status').innerText = response;

}).fetchStockData(ticker, startDate); } function openGoogleSheet() { // Replace with the URL of your Google Sheet var sheetUrl = "YOUR_GOOGLE_SHEET_URL";

// Replace with your actual Google Sheet URL window.open(sheetUrl, "_blank"); } </script> </body> </html> Step 5: Deploy Your

Web App

Step 6: Access and

Use the Web App

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapters 2, 3 - Financial Statements (not required)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Cash Flow Statement Answer |

calculation for changes |

||

|

Cash at the beginning of the

year |

2060 |

||

|

Cash

from operation |

|||

|

net income |

3843 |

||

|

plus depreciation |

1760 |

||

|

-/+ AR |

-807 |

807 |

|

|

-/+ Inventory |

-3132 |

3132 |

|

|

+/- AP |

1134 |

1134 |

|

|

net change

in cash from operation |

2798 |

||

|

Cash

from investment |

|||

|

-/+ (NFA+depreciation) |

-1680 |

1680 |

|

|

net

change in cash from investment |

-1680 |

||

|

Cash

from finaning |

|||

|

+/- long term debt |

1700 |

1700 |

|

|

+/- common stock |

2500 |

2500 |

|

|

- dividend |

-6375 |

6375 |

|

|

net

change in cash from financing |

-2175 |

||

|

Total

net change of cash |

-1057 |

||

|

Cash

at the end of the year |

1003 |

||

************ What is Free Cash Flow **************

What is free cash flow (video)

What is free cash flow (FCF)? Why is

it important?

•

FCF is the amount of cash available from operations for

distribution to all investors (including stockholders and debtholders) after

making the necessary investments to support operations.

•

A company’s value depends on the amount of FCF it can generate.

What are the five uses of FCF?

1. Pay interest on debt.

2. Pay back principal on debt.

3. Pay dividends.

4. Buy back stock.

5. Buy nonoperating assets (e.g., marketable securities,

investments in other companies, etc.)

What are operating

current assets?

•

Operating current assets are the CA

needed to support operations.

•

Op CA include: cash, inventory,

receivables.

•

Op CA exclude: short-term investments,

because these are not a part of operations.

What are operating

current liabilities?

•

Operating current liabilities are the

CL resulting as a normal part of operations.

•

Op CL include: accounts payable and

accruals.

•

Op CL exclude: notes payable, because

this is a source of financing, not a part of operations.

Capital

expenditure = increases in NFA + depreciation

Or,

capital expenditure = increases in GFA

Note: All companies, foreign and domestic, are required to file

registration statements, periodic reports, and other forms electronically

through EDGAR. https://www.sec.gov/edgar/searchedgar/companysearch.html

In class exercise

1. Firm AAA has EBIT (operating income) of $3 million, depreciation of $1 million. Firm AAA’s expenditures on fixed assets = $1 million. Its net operating working capital = $0.6 million. Calculate for free cash flow. Imagine that the tax rate =40%.

a. $1.2

b. $1.3

c. $1.4

d. $1.5

FCF = EBIT(1 – T) + Deprec. – (Capex + NOWC)

answer:

EBIT $3

Tax rate 40%

Depreciation $1

Capex + NOWC $1.60

So, FCF = $1.2

2. The following information should be used for the following problems:

2014 2015

Sales $ 740 $ 785

COGS 430 460

Interest 33 35

Dividends 16 17

Depreciation 250 210

Cash 70 75

Accounts receivables 563 502

Current liabilities 390 405

Inventory 662 640

Long term debt 340 410

Net fixed assets 1,680 1,413

Common stock 700 235

Tax rate 35% 35%

• What is the net income for 2015? ($52)

Ratio Analysis template

https://www.jufinance.com/ratio

Finviz.com/screener for ratio analysis (https://finviz.com/screener.ashx)

Financial ratio

analysis (VIDEO)