FIN310 Class Web Page, Fall ' 24

Instructor: Maggie Foley

Jacksonville University

The

Syllabus Risk

Tolerance Assessment

·

Term

Project 1 (option 1)

·

Term

Project 2 (option 2)

·

Term Project 3 (option 3): Create a Stock Data Fetcher Using Google Sheets

(Details can be found at the bottom of the website)

Weekly SCHEDULE, LINKS, FILES and Questions

|

Chapter |

Coverage,

HW, Supplements -

Required |

References

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Intro |

Discussion: How to pick stocks (finviz.com) How To Win The MarketWatch Stock Market Game

Daily earning announcement: http://www.zacks.com/earnings/earnings-calendar IPO schedule: http://www.marketwatch.com/tools/ipo-calendar |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Review of the Financial Market

U.S. Regional Banks

Crisis in 2023

Video on youtube (fyi)

1.

Background:

2.

The Trigger:

3.

Contagion Effect:

4.

Government and

Regulatory Response:

5.

Lessons Learned:

Key

Takeaways

The U.S. economy in

August 2024

· Economic Growth:

· Inflation and Monetary Policy:

· Financial Markets:

· Fiscal Policy:

· Election Uncertainty:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part I –

The Feds: Steering Monetary Policy Quiz2 Fed Introduction Video by Invideo.ai (FYI) 1.

The Federal Reserve System: Structure and Roles

·

The Federal Reserve

System:

·

Board of Governors:

·

12 Regional Federal

Reserve Banks:

·

Regional Bank Presidents:

2.

The Federal Open Market Committee (FOMC): Decision-Making Body

·

Composition of the FOMC:

·

Functions and

Responsibilities:

3.

The Interest Rate Decision-Making Process

·

Data Analysis:

·

Discussion and Debate:

·

Voting:

·

Public Communication:

4.

Key Concepts and Tools in Monetary Policy

(Continued)

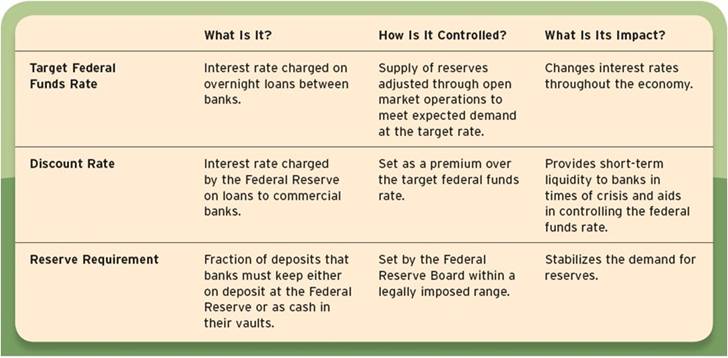

·

Federal Funds Rate

(Continued):

·

Open Market Operations:

·

Discount Rate:

·

Reserve Requirements:

·

Quantitative Easing (QE):

·

Dual Mandate:

5.

Critical Thinking Points

·

Who Makes the Decisions?: ·

FOMC Members:

Understand the distinct roles of the Board of Governors and the regional

Federal Reserve Bank Presidents in the decision-making process. Recognize the

influence of each member, especially the Fed Chair, and how their

backgrounds, economic philosophies, and regional concerns shape their

decisions. ·

Rotation System:

Consider how the rotation of voting rights among regional bank presidents

ensures a broad range of perspectives are considered in monetary policy. ·

How Is Policy Decided?: ·

Data-Driven Decisions:

Reflect on the importance of data in shaping monetary policy. Explore how

different economic indicators, like unemployment, inflation, and GDP growth,

influence the FOMC’s decisions. ·

Diverse Opinions:

Examine how the diversity of opinions within the FOMC can lead to complex

policy debates. Consider the impact of dissenting votes and what they reveal

about the challenges of setting a single monetary policy in a diverse and

dynamic economy. ·

Communication Strategy:

Analyze the importance of clear communication from the Fed, especially in

managing market expectations and maintaining public confidence in the

economy. ·

What Tools Does the Fed

Use?: ·

Impact of Interest Rates:

Delve into how changes in the federal funds rate ripple through the economy,

affecting everything from mortgage rates to business investment decisions.

Explore the effectiveness and limitations of this tool in different economic

conditions. ·

Role of Open Market

Operations: Study how the Fed uses OMOs to manage

the money supply and control short-term interest rates. Understand the

strategic use of buying and selling securities and how these actions

influence the broader economy. ·

Use of Non-Traditional

Tools: Investigate the circumstances under

which the Fed might use tools like QE. Consider the potential risks and

benefits of such interventions and how they differ from traditional monetary

policy actions. ·

Why Does the Fed Matter?:

6. 12 Regional Federal

Reserve Bank Presidents

Nomination Process:

1. Selection by the Regional Board of Directors: The president of each of the 12 regional Federal Reserve Banks is selected by the bank's board of directors. The board of directors consists of nine members, divided into three classes: · Class A: Three members representing member banks. · Class B: Three members representing the public, elected by member banks. · Class C: Three members representing the public, appointed by the Board of Governors. The Class B and Class C directors play a primary role in the selection process, with the final candidate needing to be approved by the Board of Governors in Washington, D.C. 2. Approval by the Board of Governors: Once the regional board of directors selects a candidate, the appointment must be approved by the Board of Governors of the Federal Reserve System. Term Duration:

7. Federal Reserve Chair

and Vice Chair

Nomination Process:

· Nomination by the President: The Chair and Vice Chair of the Federal Reserve Board are nominated by the President of the United States from among the sitting members of the Board of Governors. · Confirmation by the Senate: The nominations must be confirmed by the U.S. Senate through a majority vote. Term Duration:

8.

Board of Governor

Nomination

Process:

Term

Duration:

Summary

9. Chair The Fed Simulation Game Game

1: https://lewis500.github.io/macro/ Game

2: https://www.fedchairsim.com/ Homework 1-1: Understanding

the Role of the Fed Chair (due with the first midterm exam) Objective: Play the FOMC Simulation Game and analyze the challenges faced by the Federal Reserve Chair. Provide thoughtful advice based on your experience with the simulation and understanding of monetary policy. Instructions: 1.

Play the Simulation: 2.

Reflection Questions: o Challenges

as Fed Chair:

o Advice

to Fed Chair Jerome Powell:

|

In Plain Enlgish Fed St. Louise

(Cool video about Fed)

***** FRB – Federal Reserve Banks ******* Federal Reserve Bank

of Atlanta Federal Reserve Bank of Atlanta's Boardroom Video

(youtube)

https://www.atlantafed.org/about/atlantafed/directors

The

Fed Explains Monetary Policy (video) The

Tools of Monetary Policy (video) Segment

406: Open Market Operations(video of Philadelphia Fed) ********** Fed Funds Rate *********

Release

date: July 1, 2024 https://fred.stlouisfed.org/series/FEDFUNDS What

is the Fed Fund rate (youtube) Segment 406: Open Market Operations (youtube, by the Fed)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part II – The Mechanics of

Monetary Policy: Tools and Outcomes Quiz1 Quiz3 Introduction to Monetary Policy

Monetary

policy involves the actions undertaken by a central bank, such as the Federal

Reserve in the United States, to influence the availability and cost of money

and credit to help promote national economic goals. It revolves around

managing the economy's money supply and interest rates to control inflation,

stabilize currency, and achieve a sustainable level of economic growth and

employment. Key Tools of Monetary Policy

1.

Open Market Operations

(OMOs):

2.

The Discount Rate:

3.

Reserve Requirements:

Goals of Monetary Policy

Outcomes of Monetary Policy

Challenges in Monetary Policy

Homework 1-2: Monetary Policy (due

with the first midterm exam) 1. Explore the interactive simulation at https://www.jufinance.com/fin310_24f/money_interest.html

to understand the relationship between money supply and interest rates. Question: Based on current economic indicators, do you support the

Federal Reserve's decision to lower interest rates in September 2024? Provide

reasons for your stance. 2. Velocity of Money

Simulation Engage with

the simulation game at https://www.jufinance.com/fin310_24f/chair_fed.html

to learn about the dynamics between money supply, interest rates, and the

velocity of money. Question: What is the concept of the velocity of money? How can

changes in interest rates influence this monetary indicator? What is the

current velocity of money according to the latest data? In your opinion, is

this velocity too high, too low, or optimal for the current economic

environment? |

Nominal Interest Rates and the Market for Money Beggs, Jodi. "How Money Supply and Demand Determine Nominal Interest Rates." ThoughtCo, Apr. 5, 2023, thoughtco.com/nominal-interest-rates-and-money-supply-and-demand-1147766.

There is more than one

interest rate in an economy and even more than one interest rate on

government-issued securities. These interest rates tend to move in tandem, so

it is possible to analyze what happens to interest rates overall by looking

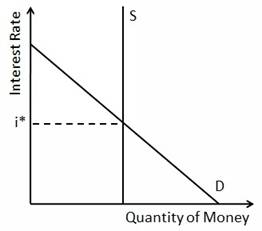

at one representative interest rate. What Is the Price of Money? Like other supply and demand

diagrams, the supply and demand for money is plotted with the price

of money on the vertical axis and the quantity of money in the economy on the

horizontal axis. But what is the "price" of money? As it turns out, the price

of money is the opportunity cost of holding money. Since cash doesn't earn

interest, people give up the interest that they would have earned on non-cash

savings when they choose to keep their wealth in cash instead. Therefore,

the opportunity cost of money, and, as a

result, the price of money, is the nominal interest rate. Graphing the

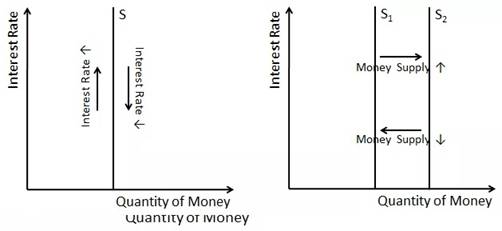

Supply of Money

Therefore, the supply of

money is represented by a vertical line at the quantity of money that the Fed

decides to put out into the public realm. When the Fed increases the money

supply this line shifts to the right. Similarly, when the Fed decreases the

money supply, this line shifts to the left. As a reminder, the Fed

generally controls the supply of money by open-market operations where it

buys and sells government bonds. When it buys bonds, the economy gets the

cash that the Fed used for the purchase, and the money supply increases. When

it sells bonds, it takes in money as payment, and the money supply decreases.

Even quantitative easing is just a variant

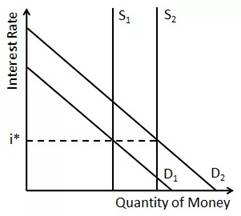

on this process. Graphing the Demand for Money

Most importantly,

households, businesses and so on use the money to purchase goods and

services. Therefore, the higher the dollar value of aggregate output, meaning

the nominal GDP, the more money the players in the

economy want to hold to spend it on this output. However, there's an

opportunity cost of holding money since money doesn't earn interest. As the

interest rate increases, this opportunity cost increases, and the quantity of

money demanded decreases as a result. To visualize this process, imagine a

world with a 1,000 percent interest rate where people make transfers to their

checking accounts or go to the ATM every day rather than hold any more cash

than they need to. Since the demand for money

is graphed as the relationship between the interest rate and quantity of

money demanded, the negative relationship between the opportunity cost of

money and the quantity of money that people and businesses want to hold

explains why the demand for money slopes downward. Just like with other demand curves, the demand for money shows

the relationship between the nominal interest rate and the quantity of money

with all other factors held constant, or ceteris paribus. Therefore, changes

to other factors that affect the demand for money shift the entire demand

curve. Since the demand for money changes when nominal GDP changes, the

demand curve for money shifts when prices (P) or real GDP (Y) changes. When

nominal GDP decreases, the demand for money shifts to the left, and, when

nominal GDP increases, the demand for money shifts to the right. Equilibrium in the Money Market

Equilibrium in a market is

found where the quantity supplied equals the quantity demanded because

surpluses (situations where supply exceeds demand) pushes prices down and

shortages (situations where demand exceeds supply) drive prices up. So, the

stable price is the one where there is neither a shortage nor a surplus. Regarding the money market,

the interest rate must adjust such that people are willing to hold all of the

money that the Federal Reserve is trying to put out into the economy and

people aren't clamoring to hold more money than is available. Changes in the Supply of Money

When the Fed decreases the

money supply, there is a shortage of money at the prevailing interest rate. Therefore,

the interest rate must increase to dissuade some people from holding money.

This is shown on the right-hand side of the diagram above. This is what happens when

the media says that the Federal Reserve raises or lowers interest rates—the

Fed isn't directly mandating what interest rates are going to be but is

instead adjusting the money supply to move the resulting equilibrium interest

rate. Changes in the Demand for Money

The right-hand panel of the

diagram shows the effect of a decrease in demand for money. When not as much

money is needed to purchase goods and services, a surplus of money

results and interest rates must decrease to make players in the economy

willing to hold the money. Using Changes in the Money Supply to Stabilize

the Economy

On the other hand, if the

supply of money increases in tandem with the demand for money, the Fed can

help to stabilize nominal interest rates and related quantities (including

inflation). That said, increasing the

money supply in response to a demand increase that is caused by an increase

in prices rather than an increase in output is not advisable, since that

would likely exacerbate the problem of inflation rather than have a

stabilizing effect. Key Takeaways:

1.

Concept of Nominal Interest Rates:

2.

The Price of Money:

3.

Supply and Demand Representation:

4.

Market Equilibrium:

5.

Impact of Federal Reserve Actions:

6.

Influence of Demand Changes:

7.

Stabilizing the Economy Through Monetary Policy:

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

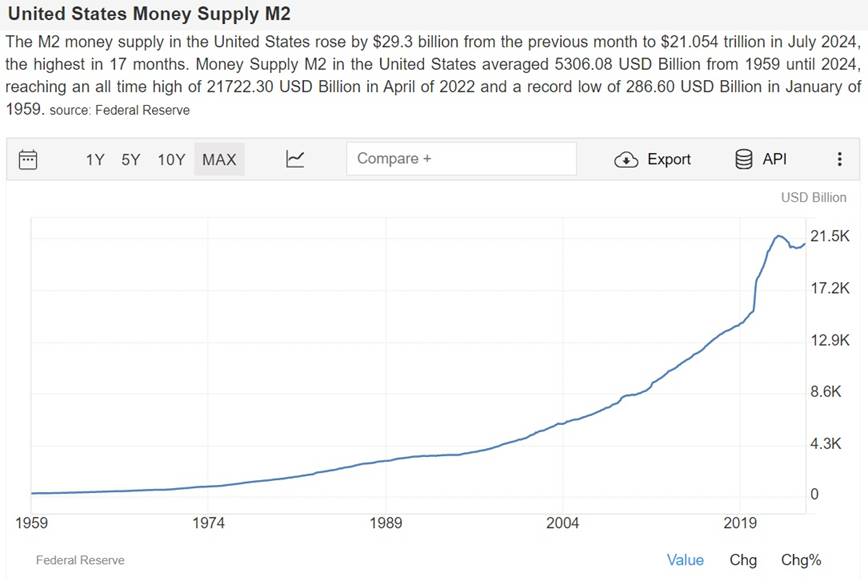

Chapter 2 What is Money Part I What is Money?

Let’s start by Playing a game https://www.jufinance.com/game/money_supply.html · There is no single "correct" measure of

the money supply: instead, there are several measures, classified along a

spectrum or continuum between narrow and broad monetary

aggregates. • Narrow measures include only the most liquid

assets, the ones most easily used to spend (currency, checkable deposits).

Broader measures add less liquid types of assets (certificates of deposit, etc.)

· M0: In

some countries, such as the United Kingdom, M0 includes bank reserves, so M0

is referred to as the monetary base, or narrow money. · MB: is

referred to as the monetary base or total currency. This

is the base from which other forms of money (like checking deposits, listed

below) are created and is traditionally the most liquid measure of the money

supply. · M1: Bank

reserves are not included in M1. (M1 and

Components @ Fed St. Louise website)

· M2:

Represents M1 and "close substitutes" for M1. M2 is a broader

classification of money than M1. M2 is a key economic indicator used to

forecast inflation. (M2 and components @

Fed St. Louise website) · M3: M2

plus large and long-term deposits. Since 2006, M3 is no longer published by

the US central bank. However, there are still estimates produced by

various private institutions. (M3 and components at

Fed St. Louise website) Let’s watch this money

supply video:

https://tradingeconomics.com/united-states/money-supply-m0

https://tradingeconomics.com/united-states/money-supply-m1

https://tradingeconomics.com/united-states/money-supply-m2 Key Takeaway: VIDO (FYI) by

invideo.ai

·

Definition: M0 represents the most

basic form of money, including physical currency (coins and paper money) in circulation

and reserves held by banks at the central bank. It is the foundation of the

money supply and the most liquid form of money. ·

Role: M0 is crucial because it

forms the base upon which the broader money supply (M1 and M2) is built. It

reflects the amount of cash and bank reserves that can be quickly used by

banks to meet withdrawal demands or create more money through lending.

·

Stimulating

Economic Activity:

The growth in M1 and M2 during the pandemic helped stimulate economic activity

by making more funds available for spending and investment, which was crucial

for economic recovery. ·

Inflationary

Pressure:

The significant increase in the money supply has also raised concerns about

inflation, as more money in circulation can lead to rising prices if it

outpaces economic growth. ·

Central

Bank Policy:

The Federal Reserve closely monitors these trends and adjusts policies, such

as interest rates, to balance economic growth with inflation control,

ensuring that the expansion of M1 and M2 does not lead to excessive

inflation. Homework (due with the first midterm

exam)

Imagine you're the Chair of the Federal Reserve during the

COVID-19 pandemic. You have to make decisions that will affect M0, M1, and

M2.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

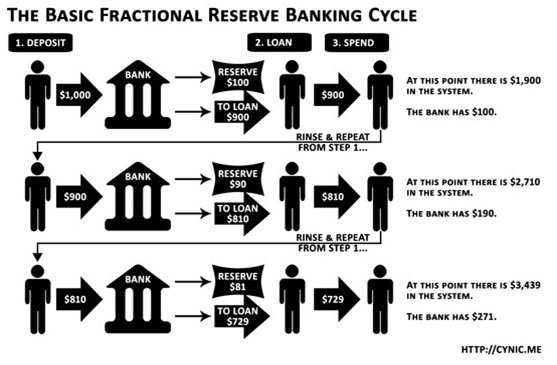

Part II What is Fractional

Reserve Banking System? The Money

Multiplier (video)

Money creation in a fractional reserve system | Financial

sector | AP Macroeconomics | Khan Academy

Fractional Reserve Banking By JULIA KAGAN Updated August 10, 2022, Reviewed by SOMER

ANDERSON What Is Fractional Reserve Banking? Fractional reserve

banking is a system in which only a

fraction of bank deposits are backed by actual cash on hand and available for

withdrawal. This is done to theoretically expand the economy by freeing

capital for lending. Today, most economies' financial systems use

fractional reserve banking. KEY TAKEAWAYS ·

Fractional reserve

banking describes a system whereby banks can loan out a certain amount of the

deposits that they have on their balance sheets. ·

Banks are required

to keep on hand a certain amount of the cash that depositors give them, but

banks are not required to keep the entire amount on hand. ·

Often, banks are

required to keep some portion of deposits on hand, which is known as the

bank's reserves. ·

Some banks are exempt

from holding reserves, but all banks are paid a rate of interest on reserves. Understanding

Fractional Reserve Banking Banks are required to

keep on hand and available for withdrawal a certain amount of the cash that

depositors give them. If someone deposits $100, the bank can't lend out the

entire amount. Nor are banks required to keep the entire amount on hand. Many central banks have historically

required banks under their purview to keep 10% of the deposit, referred to as

reserves. This requirement is set in the U.S. by the Federal Reserve and is

one of the central bank's tools to implement monetary policy. Increasing the

reserve requirement takes money out of the economy while decreasing the

reserve requirement puts money into the economy. Historically, the

required reserve ratio on non-transaction accounts (such as CDs) is zero,

while the requirement on transaction deposits (e.g., checking accounts) is 10

percent. Following recent efforts to stimulate economic growth, however, the

Fed has reduced the reserve requirements to zero for transaction accounts as

well. Fractional Reserve

Requirements Depository

institutions must report their transaction accounts, time and savings

deposits, vault cash, and other reservable obligations to the Fed either

weekly or quarterly. Some banks are exempt from holding reserves, but all banks are paid a rate of interest on

reserves called the "interest rate on reserves" (IOR) or the

"interest rate on excess reserves" (IOER). This rate acts as an

incentive for banks to keep excess reserves. Reserve requirements

for banks under the Federal Reserve Act were set at 13%, 10%, and 7%

(depending on what kind of bank) in 1917. In the 1950s and '60s, the Fed had

set the reserve ratio as high as 17.5% for certain banks, and it remained

between 8% to 10% throughout much of the 1970s through the 2010s. During this period,

banks with less than $16.3 million in assets were not required to hold

reserves. Banks with assets of less than $124.2 million but more than $16.3

million had to have 3% reserves, and those banks with more than $124.2

million in assets had a 10% reserve requirement. Beginning March 26, 2020, the 10% and 3% required reserve ratios

against net transaction deposits was reduced to 0 percent for all banks, essentially

removing the reserve requirements altogether. Prior to the

introduction of the Fed in the early 20th century, the National Bank Act of

1863 imposed 25% reserve requirements for U.S. banks under its charge. Fractional Reserve Multiplier Effect "Fractional reserve" refers to the

fraction of deposits held in reserves. For example, if a bank has $500

million in assets, it must hold $50 million, or 10%, in reserve. Analysts reference an

equation referred to as the multiplier equation when estimating the impact of

the reserve requirement on the economy as a whole. The equation provides an estimate for the amount of money created

with the fractional reserve system and is calculated by multiplying the

initial deposit by one divided by the reserve requirement. Using the

example above, the calculation is $500 million multiplied by one divided by

10%, or $5 billion. This is not how money is actually created but only a way to

represent the possible impact of the fractional reserve system on the money

supply. As such, while is useful for economics professors, it is generally

regarded as an oversimplification by policymakers. What Are the Pros of Fractional Reserve Banking? Fractional reserve banking permits banks to use funds (i.e., the

bulk of deposits) that would be otherwise unused and idle to generate returns

in the form of interest rates on new loans—and to make more money available

to grow the economy. It is thus able to better allocate capital to where it

is most needed. What Are the Cons of Fractional Reserve Banking? Fractional reserve banking could catch a bank short of funds

on hand in the self-perpetuating panic of a bank run. This occurs when

too many depositors demand their cash at the same time, but the bank only

has, say 10% of deposits in liquid cash available. Many U.S. banks were

forced to shut down during the Great Depression because too many customers

attempted to withdraw assets at the same time. Nevertheless, fractional

reserve banking is an accepted business practice that is in use at banks

worldwide. Where Did Fractional

Reserve Banking Originate? Nobody knows for sure

when fractional reserve banking originated, but it is certainly not a modern

innovation. Goldsmiths during the Middle Ages were thought to issue demand

receipts for gold on hand that exceeded the amount of physical gold they had

under custody, knowing that on any given day only a small fraction of that

gold would be demanded. In 1668, Sweden's

Riksbank introduced the first instance of modern fractional reserve banking. Example:

You deposited $1,000 in a local bank

Homework of chapter 2 (due with the first mid term) 1.

Imagine that you

deposited $5,000 in Bank A. Reserve ratio is 0.1. Imagine that the fractional banking system

is fully functioning. After Eight cycles, what is the

amount that has been deposited and what is the total amount that has been

lent out? |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 11 - 14:

Commercial Banking and Investment Banking PPT2 Commercial banking II (Balance

sheet) Part I – Commercial

Bank’s Financial Statement Analysis Quiz Let’s Play a

game on Banks’ Balance Sheet

Wells Fargo’s Balance Sheet https://www.nasdaq.com/market-activity/stocks/wfc/financials

Wells Fargo’s Income Statement https://www.nasdaq.com/market-activity/stocks/wfc/financials

Understanding

How Banks Operate: A Case Study on Wells Fargo (based on a prior study) Quiz

1. Introduction to Banking Operations

Banks

are essential financial institutions that play a vital role in the economy.

They manage money, facilitate transactions, provide credit, and offer various

financial services to individuals, businesses, and governments. We'll use

Wells Fargo's financial data as a case study to illustrate these concepts. 2. Core Functions of a Bank

Deposits

and Loans:

Interest

Income and Net Interest Margin (NIM):

Investments:

Fee-Based

Services:

3. Understanding Key Financial Statements

Balance

Sheet:

Income

Statement:

4. Wells Fargo Case Study: Key Financial

Metrics (2020-2023)

Using

Wells Fargo's financial data, let's explore key metrics that indicate the

bank's financial health: Total

Revenue:

Cost

of Revenue:

Net

Income:

Operating

Income (EBIT):

Total

Assets and Liabilities:

5. Identifying Bank Vulnerabilities

Declining

Net Interest Margin (NIM):

High

Loan Defaults:

Increasing

Cost of Revenue:

High

Leverage:

Declining

Liquidity:

6. Safety Tips for Managing and Analyzing

Banks

Diversify

Assets:

Maintain

Adequate Reserves:

Monitor

Loan Quality:

Ensure

Liquidity:

Stress

Testing and Scenario Analysis:

Regulatory

Compliance:

7. Practical Application: Analyzing Wells

Fargo

Here’s how we can apply these concepts using Wells Fargo’s data:

8. Conclusion on Wells Fargo

Wells

Fargo’s financial performance from 2020 to 2023 demonstrates

a bank that has effectively managed its operations despite various economic

challenges. The consistent growth in revenue and net income, coupled with

stable asset management, reflects the bank’s strong

financial position. However, the significant rise in the cost of revenue in

2023 could be a potential risk factor that needs to be monitored closely. |

Part III: Governmental Regulations on

Banking Industry (FYI) A Brief History of U.S. Banking

Regulation (FYI) By MATTHEW

JOHNSTON Reviewed by

MICHAEL J BOYLE on July 30, 2021 https://www.investopedia.com/articles/investing/011916/brief-history-us-banking-regulation.asp As early as

1781, Alexander Hamilton recognized that “Most commercial nations have found

it necessary to institute banks, and they have proved to be the happiest

engines that ever were invented for advancing trade.” Since then, America has

developed into the largest economy in the world, with some of the biggest

financial markets in the world. But the path from then to now has been

influenced by a variety of different factors and an ever-changing regulatory

framework. The changing nature of that framework is best characterized by the

swinging of a pendulum, oscillating between the two opposing poles of greater

and lesser regulation. Forces, such as the desire for greater financial

stability, more economic freedom, or fear of the concentration of too much

power in too few hands, are what keep the pendulum swinging back and forth. Early Attempts

at Regulation in Antebellum America From the

establishment of the First Bank of the United States in 1791 to the National

Banking Act of 1863, banking regulation in America was an experimental mix of

federal and state legislation.1 2 The regulation was motivated, on the

one hand, by the need for increased centralized control to maintain stability

in finance and, by extension, the overall economy. While on the other hand,

it was motivated by the fear of too much control being concentrated in too

few hands. Despite

bringing a relative degree of financial and economic stability, the First

Bank of the United States was opposed to being unconstitutional, with many

fearing that it relegated undue powers to the federal government.

Consequently, its charter was not renewed in 1811. With the government

turning to state banks to finance the War of 1812 and the significant

over-expansion of credit that followed, it became increasingly apparent that

financial order needed to be reinstated. In 1816, the Second Bank of the

United States would receive a charter, but it too would later succumb to

political fears over the amount of control it gave the federal government and

was dissolved in 1836. Not only at

the federal level, but also at the level of state banking, obtaining an

official legislative charter was highly political. Far from being granted on

the basis of proven competence in financial matters, successful acquisition

of a charter depended more on political affiliations, and bribing the

legislature was commonplace. By the time of the dissolution of the Second

Bank, there was a growing sense of a need to escape the politically corrupt

nature of legislative chartering. A new era of “free banking” emerged with a

number of states passing laws in 1837 that abolished the requirement to

obtain an officially legislated charter to operate a bank. By 1860, a majority

of states had issued such laws. In this

environment of free banking, anyone could operate a bank on the condition,

among others, that all notes issued were back by proper security. While this

condition served to reinforce the credibility of note issuance, it did not

guarantee immediate redemption in specie (gold or silver), which would serve

to be a crucial point. The era of free banking suffered from financial

instability with several banking crises occurring, and it made for a

disorderly currency characterized by thousands of different banknotes

circulating at varying discount rates. It is this instability and disorder

that would renew the call for more regulation and central oversight in the

1860s. Increasing

Regulation from the Civil War to the New Deal The free

banking era, characterized as it was by a complete lack of federal control

and regulation, would come to an end with the National Banking Act of 1863

(and its later revisions in 1864 and 1865), which aimed to replace the old

state banks with nationally chartered ones. The Office of the Comptroller of

the Currency (OCC) was created to issue these new bank charters as well as

oversee that national banks maintained the requirement to back all note

issuance with holdings of U.S. government securities. While the new

national banking system helped return the country to a more uniform and

secure currency that it had not experienced since the years of the First and

Second Banks, it was ultimately at the expense of an elastic currency that

could expand and contract according to commercial and industrial needs. The

growing complexity of the U.S. economy highlighted the inadequacy of an

inelastic currency, which led to frequent financial panics occurring

throughout the rest of the nineteenth century. With the

occurrence of the bank panic of 1907, it had become apparent that America’s

banking system was out of date. Further, a committee gathered in 1912 to

examine the control of the nation’s banking and financial system. It found

that the money and credit of the nation were becoming increasingly

concentrated in the hands of relatively few men. Consequently, under the

presidency of Woodrow Wilson, the Federal Reserve Act of 1913 was approved to

wrest control of the nation’s finances from banks while at the same time

creating a mechanism that would enable a more elastic currency and greater

supervision over the nation’s banking infrastructure. Although the

newly established Federal Reserve helped to improve the nation’s payments

system and created a more flexible currency, it's a misunderstanding of the

financial crisis following the 1929 stock market crash served to roil the

nation in a severe economic crisis that would come to be known as the Great

Depression. The Depression would lead to even more banking regulation

instituted by President Franklin D. Roosevelt as part of the provisions under

the New Deal. The Glass-Steagall Act of 1933 created the Federal Deposit

Insurance Corporation (FDIC), which implemented regulation of deposit

interest rates, and separated commercial from investment banking. The Banking

Act of 1935 served to strengthen and give the Federal Reserve more

centralized power. 1980s

Deregulation and Post-Crisis Re-Regulation The period

following the New Deal banking reforms up until around 1980 experienced a

relative degree of banking stability and economic expansion. Still, it has

been recognized that the regulation has also served to make American banks

far less innovative and competitive than they had previously been. The

heavily regulated commercial banks had been losing increasing market share to

less-regulated and innovative financial institutions. For this reason, a wave

of deregulation occurred throughout the last two decades of the twentieth

century. In 1980,

Congress passed the Depository Institutions Deregulation and Monetary Control

Act, which served to deregulate financial institutions that accept deposits

while strengthening the Federal Reserve’s control over monetary policy.6 Restrictions on the opening of bank

branches in different states that had been in place since the McFadden Act of

1927 were removed under the Riegle-Neal Interstate Banking and Branching

Efficiency Act of 1994. Finally, the Gramm-Leach-Bliley Act of 1999 repealed

significant aspects of the Glass-Steagall Act as well as the Bank Holding Act

of 1956, both of which had served to sever investment banking and insurance

services from commercial banking.7 From 1999

onwards, a bank could now offer commercial banking, securities, and insurance

services under one roof. All of this

deregulation helped to accelerate a trend towards increasing the complexity

of banking organizations as they moved to greater consolidation and

conglomeration. Financial institution mergers increased with the total number

of banking organizations consolidating to under 8000 in 2008 from a previous

peak of nearly 15,000 in the early 1980s.8 While banks

have gotten bigger, the conglomeration of different financial services under

one organization has also served to increase the complexity of those

services. Banks began offering new financial products like derivatives and

began packaging traditional financial assets like mortgages together through

a process of securitization. At the same

time that these new financial innovations were being praised for their

ability to diversify risk, the sub-prime mortgage crisis of 2007 that

transformed into a global financial crisis and the need for the bailout of

U.S. banks that had become “too big to fail” has caused the government to

rethink the financial regulatory framework. In response to the crisis, the

Obama administration passed the Dodd-Frank Wall Street Reform and Consumer

Protection Act in 2010, aimed at many of the apparent weaknesses within the

U.S. financial system.9 It may take

some time to see how these new regulations affect the nature of banking

within the U.S. The Bottom

Line In antebellum

America, numerous attempts at increased centralized control and regulation of

the banking system were tried, but fears of concentrated power and political

corruption served to undermine such attempts. Nevertheless, as the banking

system grew, the need for ever-increasing regulation and centralized control,

led to the creation of a nationalized banking system during the Civil War,

the creation of the Federal Reserve in 1913, and the New Deal reforms under

Roosevelt.4 While the

increased regulation led to a period of financial stability, commercial banks

began losing business to more innovative financial institutions,

necessitating a call for deregulation. Once again, the deregulated banking

system evolved to exhibit even greater complexities and precipitated the most

severe economic crisis since the Great Depression. Dodd-Frank was the

response, but if history is any guide, the story is far from over, or

perhaps, the pendulum will continue to swing. Why Are

Banks Regulated? (FYI) January

30, 2017 By Julie L Stackhouse This

post is the first in a series titled “Supervising Our

Nation’s Financial Institutions.”

Supervising Our Nation’s Financial Institutions The

series, written by Julie Stackhouse, executive vice president and

officer-in-charge of supervision at the St. Louis Federal Reserve, is

expected to appear at least once each month throughout 2017. The

topic of financial deregulation is once again generating news stories. It

raises a foundational question: “Why is the U.S.

banking system so heavily regulated?” Banking

regulation has existed in some form since the chartering of banks and its

goals have evolved over time. Today, banking regulation serves four main

purposes. Financial

Stability Instability

in the financial system can have material ripple effects into other parts of

the domestic and international financial sectors. Supervision that is focused

on financial stability (often called macro-prudential supervision) looks at

trends and analyzes the likelihood for financial contagion and the possible

impacts across firms that pose systemic risks. Protection

of the Federal Deposit Insurance Fund Since

Jan. 1, 1934, the Federal Deposit Insurance Corp. has insured the deposits

held in U.S. banks up to a defined amount (currently $250,000 per depositor

per bank). The federal government serves as a backstop to the insurance fund. In

exchange for this insurance guarantee, banks pay an insurance premium and are

also subject to safety and soundness examinations by state and/or federal

regulators. Oversight of individual financial institutions by banking

regulators is called micro-prudential supervision. While

the insurance fund protects depositors, it does not protect shareholders of

banks. When inappropriate risks are taken and prove unsuccessful, banks will

fail and be liquidated. Consumer

Protection Since

the creation of the Federal Trade Commission in 1914, the federal government

has had a formal obligation to protect consumers across industries. Since

that time, numerous laws and regulations have been crafted by various

agencies to protect bank customers and promote fair and equal access to

credit. Banks

conduct financial transactions with consumers either directly (lending to

consumers and taking consumer deposits) or indirectly (through financial technology

on the front end, for example). Banking regulators enforce consumer

protection regulations by conducting comprehensive reviews of bank lending

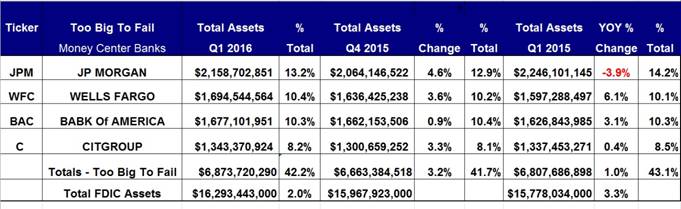

and deposit operations and investigating consumer complaints. Competition A

competitive banking system is a healthy banking system. Banking regulators

actively monitor U.S. banking markets for competitiveness and can deny bank

mergers that would negatively affect the availability and pricing of banking

services. Although

fewer than 40 banks account for more than 70 percent of all U.S. banking

assets, as shown in the table below, there are nearly 6,000 institutions of

all sizes operating in communities across the country. US

BankSystem While

all banks are regulated, not all regulations apply to every bank. We’ll discuss some of these differences in future posts. In

my next post, I’ll discuss how the banking system has

changed over time—especially over the past 25 years—adding to the complexity and scope of banking regulation

in the U.S. For discussion: As

compared with small banks, do big banks are relatively more burdened by

regulations? Or vice versa? |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part II –Bank Run and Bank Failure

1.

What is bank run? It is rare. Why?

2. How can you

tell that banks are getting bigger and bigger? Who need big banks? What is too big to fail (Bloomberg

university) video

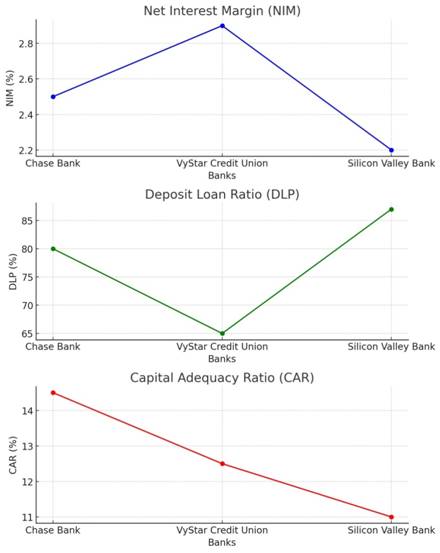

Table of Key Financial Metrics: (The data are collected for

late 2022 and early 2023 based on available public data)

Definitions

and Explanations:

1.

Net Interest Margin

(NIM):

2.

Deposit Loan Ratio (DLP): ·

Definition:

DLP shows the proportion of a bank's deposits that have been lent out. A

higher ratio suggests more aggressive lending. ·

Explanation: First

Republic Bank had a very high DLP of 90%,

meaning it had lent out a large portion of its deposits, leaving it

vulnerable to liquidity issues. Similarly, SVB had

a DLP of 87%, making it susceptible

to liquidity risks during a sudden bank run, as they lacked sufficient liquid

reserves to meet withdrawal demands. 3.

Capital Adequacy Ratio

(CAR):

Why These Banks Failed:

1.

High DLPs:

Banks like First Republic and SVB

had high DLPs, which meant they aggressively loaned out deposits, leaving

them with limited liquidity. When depositors began to withdraw funds en

masse, these banks struggled to meet the demand, leading to bank

runs. 2.

Low CARs:

With relatively low CARs, these banks had insufficient capital to absorb

losses. First Republic was particularly

vulnerable, with a CAR of 8.0%. This low capital

buffer made it difficult for the bank to weather shocks, particularly as

interest rates increased and asset values dropped. 3.

Interest Rate Risk:

Rising interest rates played a crucial role in the collapse of these banks. First

Republic and SVB had significant

exposure to long-term assets like mortgages and bonds, which lost value as

interest rates rose. Their failure to manage this interest rate risk caused

substantial losses. 4.

Loss of Depositor Confidence:

In each case, a loss of depositor confidence led to rapid withdrawals. Signature

Bank and SVB were particularly

affected, as large portions of their deposits were uninsured, making

depositors more likely to withdraw when uncertainty arose. Key Takeaway:

·

Lessons from SVB and

First Republic: These banks failed largely due to their high

DLPs and low CARs, which left them

vulnerable to liquidity crises and market fluctuations. Understanding these

metrics helps us see how poor risk management, especially under rising

interest rates, can lead to financial collapse. · Choosing Banks: By comparing banks with higher CARs and more conservative DLPs, we can better assess the safety of their banking options, focusing on banks that maintain strong capital reserves and prudent lending practices. Bank Failure · Definition of Bank Failure: A bank

failure occurs when a bank is closed by federal or state regulators because

it cannot meet its financial obligations to depositors and creditors. · Causes of Bank Failure:

· FDIC’s Role:

· Bank Runs: A bank run may occur if

depositors fear they won't be able to withdraw their money, further depleting

the bank's liquid assets. · Uninsured Deposits: It can take

months or even years for depositors to reclaim uninsured deposits from

a failed bank. · Historical Examples:

· FDIC Creation: The FDIC was

established in 1933 following the mass bank failures during the Great

Depression to protect depositors and prevent future bank panics.

https://www.fdic.gov/bank/historical/bank/ Why SVB

Failed? Key Factors Behind the Collapse

Quiz

Play a

game here

How Silicon

Valley Bank Collapsed in 36 Hours | WSJ What Went Wrong (youtube)

1. Liquidity and Deposit Loan Ratio (DLP)

2. Net Interest Margin (NIM) &

Profitability

3. Capital Adequacy Ratio (CAR)

4. Bank Run & Depositor Behavior

5. Uninsured Deposits

6. Interest Rate Risk

7. Risk Management Failures

8. Depositor Base

9. Bond Sales at a Loss

|

What Is a Bank Failure? Definition,

Causes, Results, and Examples

By JULIA KAGAN Updated November

17, 2021, Reviewed by SOMER ANDERSON, Fact checked by SUZANNE KVILHAUG https://www.investopedia.com/terms/b/bank-failure.asp What Is Bank Failure? A bank failure is the closing of an

insolvent bank by a federal or state regulator. The comptroller of the

currency has the power to close national banks; banking commissioners in the

respective states close state-chartered banks. Banks close when they are

unable to meet their obligations to depositors and others. When a bank fails,

the Federal Deposit Insurance Corporation (FDIC) covers the insured portion

of a depositor's balance, including money market accounts. Understanding Bank

Failures A bank fails when it can’t meet

its financial obligations to creditors and depositors. This could occur

because the bank in question has become insolvent, or because it no longer

has enough liquid assets to fulfill its payment obligations. KEY TAKEAWAYS · When a bank

fails, assuming the FDIC insures its deposits and finds a bank to take it

over, its customers will likely be able to continue using their accounts,

debit cards, and online banking tools.

· Bank failures

are often difficult to predict and the FDIC does not announce when a bank is

set to be sold or is going under. · It may take

months or years to reclaim uninsured deposits from a failed bank. · The most

common cause of bank failure occurs when the value of the bank’s assets falls

to below the market value of the bank’s liabilities, which are the bank's

obligations to creditors and depositors. This might happen because the bank

loses too much on its investments. It’s not always possible to predict when a

bank will fail. What Happens When a

Bank Fails? When a bank fails, it may try to

borrow money from other solvent banks in order to pay its depositors. If the

failing bank cannot pay its depositors, a bank panic might ensue in which

depositors run on the bank in an attempt to get their money back. This can

make the situation worse for the failing bank, by shrinking its liquid assets

as depositors withdraw cash from the bank. Since the creation of the FDIC,

the federal government has insured bank deposits up to $250,000 in the U.S. When a bank fails, the FDIC takes

the reins and will either sell the failed bank to a more solvent bank or take

over the operation of the bank itself. Ideally, depositors who have money in

the failed bank will experience no change in their experience of using the

bank; they’ll still have access to their money and should be able to use

their debit cards and checks as normal. In the event that a failed bank is

sold to another bank, account holders automatically become customers of that

bank and may receive new checks and debit cards. When necessary, the FDIC has

taken over failing banks in the U.S. in order to ensure that depositors

maintain access to their funds, and prevent a bank panic. Examples of Bank Failures During the 2007-2008 financial

crisis, the biggest bank failure in U.S. history occurred when Washington Mutual,

with $307 billion in assets, closed its doors. Another large bank failure had

occurred just a few months earlier when IndyMac was seized. Special Considerations The FDIC was created in 1933 by

the Banking Act (often referred to as the Glass-Steagall Act). In the years

immediately prior, which marked the beginning of the Great Depression,

one-third of American banks had failed. During the 1920s, before the Black

Tuesday crash of 1929, an average of about 70 banks had failed each year

nationwide. During the first 10 months of the Great Depression, 744 banks

failed, and during 1933 alone, about 4,000 American banks failed. By the time

the FDIC was created, American depositors had lost $140 billion due to bank

failures, and without federal deposit insurance protecting these deposits,

bank customers had no way of getting their money back. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part III: The Impact

of Lower Interest Rates on Bank Stability How to prepare personal

finances for Fed interest rate cuts (youtube)

When

Interest Rates Rise: refer to https://www.investopedia.com/ask/answers/041015/how-do-interest-rate-changes-affect-profitability-banking-sector.asp

1.

Increased Profitability:

2.

Strong Loan Demand:

3.

Example of Profit:

4.

Risk of Overly High

Rates:

5.

Bank Stocks:

When

Interest Rates Drop:

1.

Reduced Profit Margins:

2.

Increased Loan Demand:

3.

Example of Profit:

4.

Pressure on Savings:

In

summary:

|

How Interest Rate Changes Affect the Profitability of Banking By Mary Hall Updated March 08, 2024 Reviewed by

Thomas Brock Banks make money by accepting cash deposits

from their customers in return for interest payments and then investing that

money elsewhere. The bank's profit is the difference between the interest

they pay their depositors and the yield they make through investing. Higher interest rates increase the yield on

their investments. Interest rates can go too high. If they reach a level that

makes businesses and consumers hesitate to borrow, the lending side of

banking starts to suffer. Key

Takeaways ·

Interest rates

and bank profitability are connected, with banks benefiting from higher

interest rates. ·

When interest

rates are higher, banks make more money by taking advantage of the greater

spread between the interest they pay to their customers and the profits they earn

by investing. ·

A bank can

earn a full percentage point more than it pays in interest simply by lending

out the money at short-term interest rates. ·

Moreover,

higher interest rates tend to reflect a healthy economy. Demand for loans to

businesses and consumers should be high, with the bank making better returns

on those loans. ·

There's the

risk that interest rates will go too high, discouraging borrowers. The Federal Reserve reduces interest rates in

order to encourage businesses and consumers to borrow more money, adding fuel

to the economy. The banks will benefit by the rising demand for loans. But

the profit from each loan will be lower, as will the amount the bank makes by

investing in short-term debt securities. How

the Banking Sector Makes a Profit The banking industry encompasses not only

corner banks but investment banks, insurance companies, and brokerages. All

have massive cash holdings. They hold onto a small portion of that cash to

ensure liquidity. The rest is invested. Some

of it is invested in loans to businesses and consumers. Much of it is

invested in short-term Treasury securities. This is the wave of cash that

originates with the U.S. Treasury and flows constantly through the banking

system. Even the very low interest

rates that short-term Treasury notes yield are greater than the interest the

banks pay to their customers. It's similar to the way that an increase in oil

prices benefits oil drillers. They make more money for the same expenditure

of resources. Example of Interest Rate Impact on Bank

Earnings Consider a bank that has $1 billion on deposit.

The bank pays its customers an annual percentage rate of 1% interest, but the

bank earns 2% on that cash by investing it in short-term notes. The bank is

earning $20 million on its customers' accounts but returning only $10 million

to its customers. If the central bank then raises rates by 1%, the federal

funds rate will rise from 2% to 3%. The bank will then be yielding $30

million on customer accounts. The payout to customers will still be $10

million. The bank may be forced to raise the interest

rates it pays on deposits if higher interest rates persist. But the vast

majority of its customers won't go in search of a better return for their

savings. This is a powerful effect. Whenever

economic data or comments from central bank officials hint at rate hikes,

bank stocks rally first. When interest rates rise, so does the spread

between long-term and short-term rates. This is a boon to the banks since

they borrow on a short-term basis and lend on a long-term basis. Another

Way Interest-Rate Hikes Help Interest rate increases tend to occur when

economic growth is strong. Businesses are expanding, and consumers are

spending. That means a greater demand for loans. As interest rates rise, profitability on loans

increases, as there is a greater spread between the federal funds rate that

the bank earns on its short-term loans and the interest rate that it pays to

its customers. In fact, long-term rates tend to rise faster

than short-term rates. This has been true for every rate hike since the

Federal Reserve was established early in the 20th century. It is a reflection of the strong underlying

conditions and inflationary pressures that tend to prompt the Federal Reserve

to increase the interest rates it charges. It's also an optimal confluence of events for

banks, as they borrow on a short-term basis and lend on a long-term basis. Note

that if interest rates rise too high, it can start to hurt bank profits as

demand from borrowers for new loans suffers and refinancings decline. Are

Higher Interest Rates Good for Stocks? Generally,

higher interest rates are bad for most stocks. A big exception is bank stocks, which thrive

when rates rise. For everybody else, it's a delicate balancing act. Interest

rates rise because the economy is booming. But increasing interest rates make

businesses and consumers more cautious about borrowing money. This is why the Federal Reserve acts as it

does. It's raising or lowering the interest rates it charges to the banks in

order to cool the economy or rev it up. Are

Higher Interest Rates Good for Bonds? When interest rates increase, new bonds that

are issued now have to carry a higher rate of return in order to be

attractive to buyers. However, the owners of older bonds are stuck

with their lower rates of return. On the secondary market where bonds are

resold, their value will decrease to compensate for the lower return. The

investor who holds bonds in an investment portfolio doesn't lose money but

does lose the opportunity to invest in higher-yield bonds. Are

Higher Interest Rates Good for the U.S. Dollar? Higher interest rates are good for the U.S.

dollar. When the Federal Reserve tweaks its short-term interest rates, the

change ripples through all other types of loans, including the loans that are

represented by U.S. Treasury bonds and, indeed, all other dollar-denominated

investments. When U.S. rates are high in comparison with

those of other nations, money pours out of foreign investments and into U.S.

investments. That tends to make the U.S. dollar rise in value against other

currencies. The Bottom Line A rise in interest rates automatically boosts a

bank's earnings. It increases the amount of money that the bank earns by lending

out its cash on hand at short-term interest rates. At the same time, the

bank's costs of doing business are unaffected. Their customers are unlikely

to pull their cash out of their savings accounts in order to chase a slightly

higher-yielding savings account. Thus, the spread widens between the interest

the bank pays its customers and the interest it earns by lending it out. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Part IV: The Role of

Regulation in Bank Stability Quiz Game A

Brief History of

Banking and Regulations (Lessons from Hoover Boot Camp) (youtube video)

Video summary Summary:

The speaker provides an overview of the history and rationale behind

banking regulation in the U.S., highlighting how financial crises have

shaped regulatory responses. The talk is structured in three parts:

4.

The

5% Trigger: How Small Asset Declines Lead to Bank Failures ·

One

key point discussed is how banks' balance sheets are highly leveraged,

meaning even a small shock—such as a 5% decline in asset value—can

wipe out their equity, leading to insolvency and potential failure. ·

This

fragility in the banking system was a significant factor during the 2008

financial crisis when many banks went under due to deteriorating asset

values. ·

The

speaker emphasizes that this 5% trigger is a threshold at which the

balance sheet collapses, causing the bank to be unable to pay back its debt

holders, leading to bankruptcy. Key Takeaways:

Key

Takeaways from https://www.investopedia.com/articles/investing/011916/brief-history-us-banking-regulation.asp

Major

Laws and Acts:

Conclusion:

Homework (Due with the first midterm Exam)

Is Your Bank Safe?

Research the following key metrics for your bank:

1. Compare these metrics with the figures listed in the table provided (Chase, VyStar, SVB, etc.). 2. Discuss: Based on these comparisons, do you think your bank is safe? Why or why not? 3.

As a banker: Do you believe

that lower interest rates would help your bank survive or even thrive? Why or

why not? |

A Brief History of U.S.

Banking Regulation By

Matthew Johnston Updated August 12, 2024 Reviewed by Michael J Boyle Fact

checked by Suzanne Kvilhaug https://www.investopedia.com/articles/investing/011916/brief-history-us-banking-regulation.asp Alexander

Hamilton once observed, "Most commercial nations have found it necessary

to institute banks, and they have proved to be the happiest engines that ever

were invented for advancing trade." Since Hamilton's day, the United

States has grown into the largest economy in the world. That growth has been

accompanied by ever-evolving banking regulation, which has swung like a

pendulum over the past three centuries between greater and lesser control.

Competing forces like the desire for financial stability versus more economic

freedom, or the fear that too much power is concentrated in too few hands,

have kept the pendulum swinging back and forth. Here

is a brief history of banking regulation in the U.S. Key Takeaways ·

As the U.S. evolved into the world's

largest economy, its regulatory framework has evolved as well. ·

Early regulations aimed to foster economic

financial stability through centralized control of the banking system.

Opponents, however, maintained that such regulatory authority gave the

federal government too much power in comparison to the states. ·

In the years following the Civil War, an

assortment of financial crises and bank panics led to new regulations. The

Great Depression of the 1930s also gave rise to significant reforms. ·

The 1980s saw a move toward deregulation,

soon followed by re-regulation in the wake of the subprime mortgage crisis

and the Great Recession of the early 2000s. The First and Second Banks

of the United States The

First Bank of the United States was established in 1791. Although it helped

bring a degree of economic stability to the young nation, many feared that it

gave undue powers to the federal government and considered it

unconstitutional. As a result, its charter was not renewed in 1811. The U.S.

government turned to state banks to finance the War of 1812, but with the

significant over-expansion of credit that followed, it became apparent that

financial order needed to be restored.

In response, the Second Bank of the United States was chartered in

1816. It, too, would succumb to political fears over the amount of control it

gave the federal government and it was dissolved in 1836. The End of Charters, the

Rise of Free Banking Obtaining

an official legislative charter was highly political at both the federal and

state levels, depending more on political connections than proven competence

in financial matters. The bribing of legislators was fairly common. By

the time the Second Bank dissolved, a new era of free banking was emerging,

with a number of states passing laws in 1837 that abolished the requirement

that banks obtain an officially legislated charter to operate. By 1860, a

majority of states had passed such laws. During

this time of free banking, anyone could operate a bank on the condition that

all the notes it issued were backed by proper security. While that helped

reinforce the credibility of banknotes, it did not guarantee immediate

redemption in specie (gold or silver), which would serve to be a crucial

point. The

era of free banking suffered from financial instability, including several

banking crises. It also made for a chaotic currency market, characterized by

thousands of different banknotes circulating at varying discount rates. This

instability and disorder led to a renewed call for more regulation and

central oversight in the 1860s. From the Civil War to the

New Deal The

free banking era, characterized as it was by a complete lack of federal

control and regulation, ended with the National Banking Act of 1863 (and its

later revisions in 1864 and 1865), which aimed to replace the old state banks

with nationally chartered ones. The Office of the Comptroller of the Currency

(OCC) was created to issue these new bank charters as well as see to it that

national banks maintained the requirement to back all their notes with

holdings of U.S. government securities. The

new national banking system helped return the country to a more uniform and

secure currency but ultimately at the expense of an elastic currency that

could expand and contract according to commercial and industrial needs. The

growing complexity of the U.S. economy highlighted the inadequacy of an

inelastic currency, which helped fuel frequent financial panics throughout

the rest of the nineteenth century. It

became apparent during the bank panic of 1907 that America's banking system

was out of date. A committee gathered in 1912 to examine the situation and

found that the nation's money and credit were becoming increasingly concentrated

in the hands of relatively few men. The Federal Reserve Act of 1913 was

approved during the presidency of Woodrow Wilson to wrest control of the

nation's finances from banks while creating a mechanism to enable a more

elastic currency and greater supervision over the banking infrastructure. Although

the newly established Federal Reserve improved the nation's payments system

and created a more flexible currency, the country soon faced another

financial crisis, exacerbated by the 1929 stock market crash and banking

panics in 1930 and 1931. The

Great Depression, which began in 1929 and continued, by some measures, until

1941, led to new regulations instituted by President Franklin D. Roosevelt as

part of his administration's New Deal. The Glass-Steagall Act of 1933 created

the Federal Deposit Insurance Corporation (FDIC), which implemented the

regulation of deposit interest rates while separating commercial banking and

investment banking. The Banking Act of 1935 served to give the Federal Reserve,

also called the Fed, more centralized power. 1980s Banking Deregulation The

period following the banking reforms of the New Deal up until about 1980 was

marked by a relative degree of banking stability and economic expansion.

Still, critics argued that regulation also made American banks less

innovative and competitive than they were previously. The heavily regulated

commercial banks were losing increasing market share to less-regulated and

more innovative institutions. This led to a wave of deregulation throughout

the last two decades of the 20th century. Those changes included: Congress

passed the Depository Institutions Deregulation and Monetary Control Act in

1980, which served to deregulate financial institutions that accept deposits

while strengthening the Fed's control over monetary policy. estrictions

on the opening of bank branches in different states that had been in place

since the McFadden Act of 1927 were removed under the Riegle-Neal Interstate

Banking and Branching Efficiency Act of 1994. The

Gramm-Leach-Bliley Act of 1999 repealed significant aspects of the

Glass-Steagall Act as well as the Bank Holding Act of 1956, both of which had

served to sever investment banking and insurance services from commercial

banking. From 1999 onward, banks could now offer

commercial banking, securities, and insurance services under one roof. These

moves helped to accelerate a trend toward greater consolidation and

conglomeration in the banking sector, with more than 4,300 bank mergers in

the 1980s and more than 6,000 in the 1990s. As

banks became bigger, their financial services and products became more

complex. Banks started to offer new products like derivatives. They also

started packaging traditional financial assets like mortgages and selling

them to investors through the process of securitization. Banking

Regulation Following the Global Financial Crisis of 2008 The

subprime mortgage meltdown beginning in 2007, the ensuing global financial

crisis, and the need to bail out banks deemed "too big to fail"

caused the government to rethink the financial regulatory framework. In

response to the crisis, Congress passed the Dodd-Frank Wall Street Reform and

Consumer Protection Act in 2010. Some

of Dodd-Frank's protections were rolled back under the Trump administration

in 2018. In particular, the new rules loosened restrictions on institutions

with under $250 billion in assets and eliminated the need for them to pass

stress tests. Then,

in 2021, the newly arrived Biden administration signaled its intention to

tighten the government's oversight of banks. A July 2021 executive order on

promoting competition in the American economy called for greater scrutiny of

bank mergers by the Department of Justice and federal banking regulators.

"Excessive consolidation," the order explained, "raises costs

for consumers, restricts credit for small businesses, and harms low-income

communities." What Is a Central Bank? A

central bank is a public financial institution responsible for overseeing a

nation's monetary system. The central bank of the United States is the

Federal Reserve System, which describes its mission as carrying out "the

nation's monetary policy guided by the goals set forth in the Federal Reserve

Act, namely 'to promote effectively the goals of maximum employment, stable

prices, and moderate long-term interest rates.'" What Is a National Bank? National

banks in the United States are financial institutions that are chartered by

the U.S. Treasury and members of the Federal Reserve System. Examples include

Bank of America, Chase Bank, Citibank, PNC Bank, U.S. Bank, and Wells Fargo. What Is the Dodd-Frank Act? The

Dodd-Frank Act of 2010, more formally known as the Dodd-Frank Wall Street

Reform and Consumer Protection Act, is a major set of financial reforms

enacted in the wake of the Great Recession of 2007 to 2009. Among other

provisions, it clamped down on speculative trading by banks, increased

government oversight of the banking sector, and gave the government the power

to liquidate ailing banks. It also created the Consumer Financial Protection

Bureau. The Bottom Line Since

the founding of the United States, there have been numerous attempts to

centralize the control and regulation of the country's banking system. Prior

to the Civil War of the 1860s, fears of concentrated power and political

corruption served to undermine such attempts. But as the banking system grew,

the need for greater regulation and federal control became more widely accepted.

That led to the creation of a nationalized banking system during the Civil

War, the creation of the Federal Reserve in 1913, and the New Deal reforms of

the 1930s and 1940s. While

more regulation led to a long period of financial stability, banks began

losing business to more innovative financial institutions, resulting in a

move toward deregulation in the 1980s and 1990s. But it wasn't long before

the mortgage meltdown of 2007 and the most severe economic crisis since the

Great Depression led to a call for re-regulation and to the passage of the

Dodd-Frank financial reforms of 2010. The Trump administration rolled back

some of those rules, but much of Dodd-Frank remains in place and the Biden

administration has indicated its desire to restore and tighten bank

regulations, particularly with regard to mergers. If

history is any guide, the story is far from over and the regulation pendulum

will continue to swing. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

How AI and FinTech Are

Shaping the Future of Banking Quiz Based on the article by Mr.

Kreger posted at https://www.forbes.com/councils/forbesbusinesscouncil/2023/03/20/the-future-of-ai-in-banking/ · AI’s Role in Personalization: AI can

analyze customer data to provide personalized services like financial

advice, targeted product recommendations, fraud detection, and faster

customer support. It helps improve customer engagement and retention by creating

tailored experiences. · Automation and Efficiency: AI can

automate routine tasks such as account balance inquiries, password

resets, and loan applications, allowing human representatives to

handle more complex issues. This increases efficiency, reduces costs, and

offers 24/7 support. · Conversational Banking: AI-powered chatbots

can offer a seamless user experience by handling money transfers, financial

advice, and credit score monitoring through chat or voice

interfaces, making banking operations simpler for customers, including

nonnative speakers. · Use Cases: AI can enhance the

banking experience by handling tasks like fraud prevention, financial

planning, and customer service while improving account

management and insurance claims processes. · Challenges: Banks face challenges in